This is another post in our Manufactured Monday series. We try to offer some insights into manufactured spend each Monday. You can view all posts in this series by clicking here.

Hide MS

Some people are worried about how manufacturing spend (MS) could affect a mortgage application or other loan. Because of this they look for ways to hide the MS so that it won’t show up on their credit report.

It’s usually assumed that it’s possible to hide MS from your credit report by paying down the balances before the statement closes. It’s also mentioned that there are some credit card issuers who will report mid-statement balances, but most will only report based on the balance at the statement closing date.

Thus, if you’re careful to pay off the balances before the statement closing, you’re credit report will be “clean”. Additionally, if you constantly keep your balances low by paying off the balance multiple times each month, you’ll never have high-dollar amounts showing up on your credit report.

But is that really true? My own credit report indicates that you are able to hide MS from the Amex and Discover reporting but not from Visa and Mastercard reporting.

My Findings

On the credit report there are numerous numbers which are reported:

- credit limit

- monthly account balance

- high credit (the highest amount ever owed)

- scheduled payment amount (the monthly amount of your required minimum payment)

- actual payment amount

The one that especially interests us here is the last one: actual payment amount. The actual payment amount is the amount that you actually paid to the credit card that month. I religiously pay off my balances before statement closing and I constantly strive to keep the balances low. In the “account balance” column it shows zero or close to it, but there are still big sums being showed in the “actual payment amount” column.

However, there seems to be a disparity here between Visa and Mastercard versus American Express and Discover. In the case of the former, the “actual payment amount” usually shows. However, Amex and Discover don’t report that information to the credit agencies. This is only true in regard to regular Amex accounts, however, bank-branded Amex cards – such as Fidelity American Express – do report the actual payment amounts.

Important: This does NOT mean that there’s no benefit in paying off your balances early. A whopping 30% of your FICO score is based off credit utilization. This utilization factors the actual amount that you owe, as a percentage of your total credit available. If your account balances are being reported as close to zero, then you’ll be doing great in the credit utilization category. Our discussion here is specifically as it relates to hiding MS from a credit report/mortgage lender.

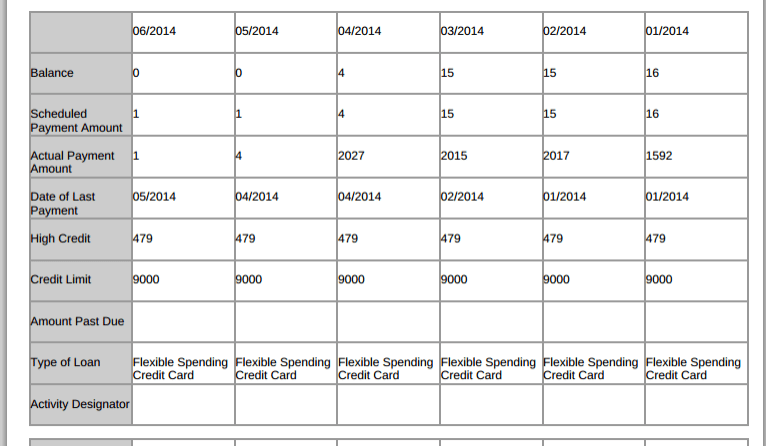

Images

Here’s a look at Citi reporting my credit card info to Equifax (the info on my Experian report is exactly the same):

This is s snapshot of my Citi Dividend card. Citi Dividend had drugstores as a category bonus in Q1 2014. I spent $6,000 in drugstores between January and March 2014. As you can see, my “balance” is being reported as close to zero, yet my credit report still shows the $6,000 in “actual payment amount” on the card.

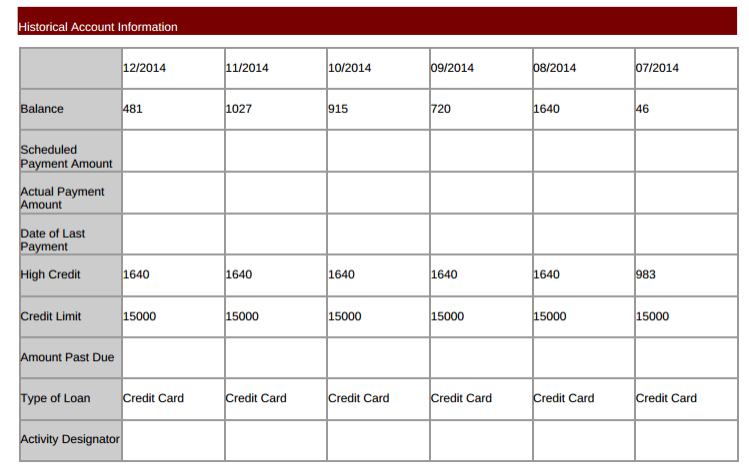

Now let’s take a look at Amex on my credit report:

Amex does not report the actual payment amount. If you keep your balances low and you pay them off before the end of the cycle, your MS will go completely unnoticed on the credit report. Discover, too, doesn’t seem to report the actual payment amount.

Note, that occasionally Visa and Mastercard credit cards also miss reporting the actual payment amount. Additionally, even when the actual payment amount is reported, it’s still less conspicuous on the credit report, since the high MS numbers are only mentioned once, under the “actual payment amount”, and not twice, under the “balance” and under the “actual payment amount”.

Conclusion

Just to recap:

- There’s good reason to be paying off your balances early in order to reduce your credit utilization. This is especially true for those who manufacture spend and would otherwise have high credit utilizations.

- Keeping balances low and paying them off early does apparently help hide the MS in the case of Amex and Discover.

- Even in the case of Visa and Mastercard, the actual payment amount is occasionally missing.

- If you pay off the balances early, the MS is less conspicuous on the credit report.

It seems many banks that used to report actual payment amounts are no longer doing so.

Things are changing in credit reporting with the introduction of Trended Data. Paying off a large balance every month now looks really good on your CR.

https://www.fanniemae.com/content/fact_sheet/desktop-underwriter-trended-data.pdf

https://www.transunion.com/blog/fannie-mae-requires-the-use-of-trended-credit-data

“revealing important information such as historical change in credit balances and actual payment amounts. These are two examples of behaviors that cannot be examined using traditional credit reports and risk models.”

But DoC’s blog post from 2 years ago was about the credit report showing those exact things (balances and actual payment amounts)… so this isn’t really anything new?

Edit: I guess the new thing is that a single credit report will show those numbers for previous dates too, not just the current date.

I’m curious what amount is reported if you put a payment before the purchase, which will cause a credit on the card.

Some issuers seem to only report the final payment for a billing cycle. This can cause abnormalities such as scheduled payment $737 actual payment $4 and still show as current. If someone were to look closely at my reports they would see escalating debt on one hand and zero balances on the other.

Hopefully, in the scheme of things, it won’t look so bad.

Unless this has changed within last 24 months, the date of reporting balances to credit bureaus is a function of “card issuer, product and and Report_To bureau (e.g Chase Freedom reports open balances to Equifax on 30th of each month (for example).,” It is possible that cardholder state also contributes to the reporting date (in certain states). I have never known the account statement closing date to be relevant in reporting open balances to any of the bureaus. Statement closing date is not even considered. If you call your cc issuer, ask the CSR which date the card issuer reports to each bureau. Be sure your open balances are sufficiently low by the earliest bureau reporting date to minimize your utilization percentage.

It’s possible that what you’re saying is correct, but I’ve always seen and heard that MOST issuers just go with the closing date and a few have a different date. I’ll have to analyze my credit report better to see if I could figure this out. Thanks

What he’s saying does not match my research tracking my own credit. I tracked this for a few months last summer, so while not definitive, pretty complete – Capital One, BoA/FIA, Discover, Amex, Wells Fargo, and Chase all report statement balance, while US Bank always reports balance on first day of month. And again, not conclusive, but I changed statement dates on several accounts to line everything up, and the reporting dates changed correspondingly. Credit Sesame is great for this, given the nature of their alerts.

Awesome! Thanks, you saved me some time there.

What site are you seeing that info on? I’ve never seen that payment info on a report, and while it doesn’t worry me terribly, it’d still be interesting to keep an eye on.

I think you mean to ask: Which site am I seeing the ‘actual payment amount’ info from my credit report.

I saw it on both my Equifax reports and on my Experian report which I received directly from them.

If you meant to ask something else, please clarify.

Yeah sorry, my wording was a bit unclear there – was definitely what I meant. I’ve long subscribed to Citi IdentityMonitor (which alas is shutting down soon) and those fields don’t appear on the reports they’ve always shown, nor do they via CreditKarma or CreditSesame. That’s why I asked – thanks!

If you pull the report directly from the issuer, I think you’d see it there.

We get one report per year free, and there are other ways of getting reports too.

Assuming you’re using Serve/Redbird and loading directly from a CC, how long do you wait between loading and bill paying?

As an aside, I’m considering switching over to buying gift cards to do loading to not have a “closed loop.” I’ve seen mixed reports on whether this is necessary or not…

I totally don’t sweat MSing on Bluebird/Serve/Redbird because I’ve never seen any problems for anyone, so long as you stick to their rules (no gc online etc.). Of course, there’s always a small risk that something could change, but I personally don’t worry a bit about either of the things you mentioned.

Nice post, Chuck. Very interesting to see what’s sent to the bureau’s

Thanks

Of course, you can always abstain from MS for a month or three before applying for a loan and look totally clean.

Well, it’s there on the report for many years. But I suppose if the past few months look good, it can definitely help.

Another recommendation that I have is: If you have the ability to open business credit cards, this will help you as the information is not reported on your credit report. For example, if I need to apply for an auto loan or mortgage, what I would do is start MS on the biz cards while keeping my personal balances low that way I don’t miss any opportunity of MS. One absolute card you should have in your wallet if you go that route is the Ink Plus hands down.

Jay

Oooh, good point. I forgot to mention that. That’s for bringing up.

From what I’ve read, Biz cards do occasionally show up on the report but not usually.