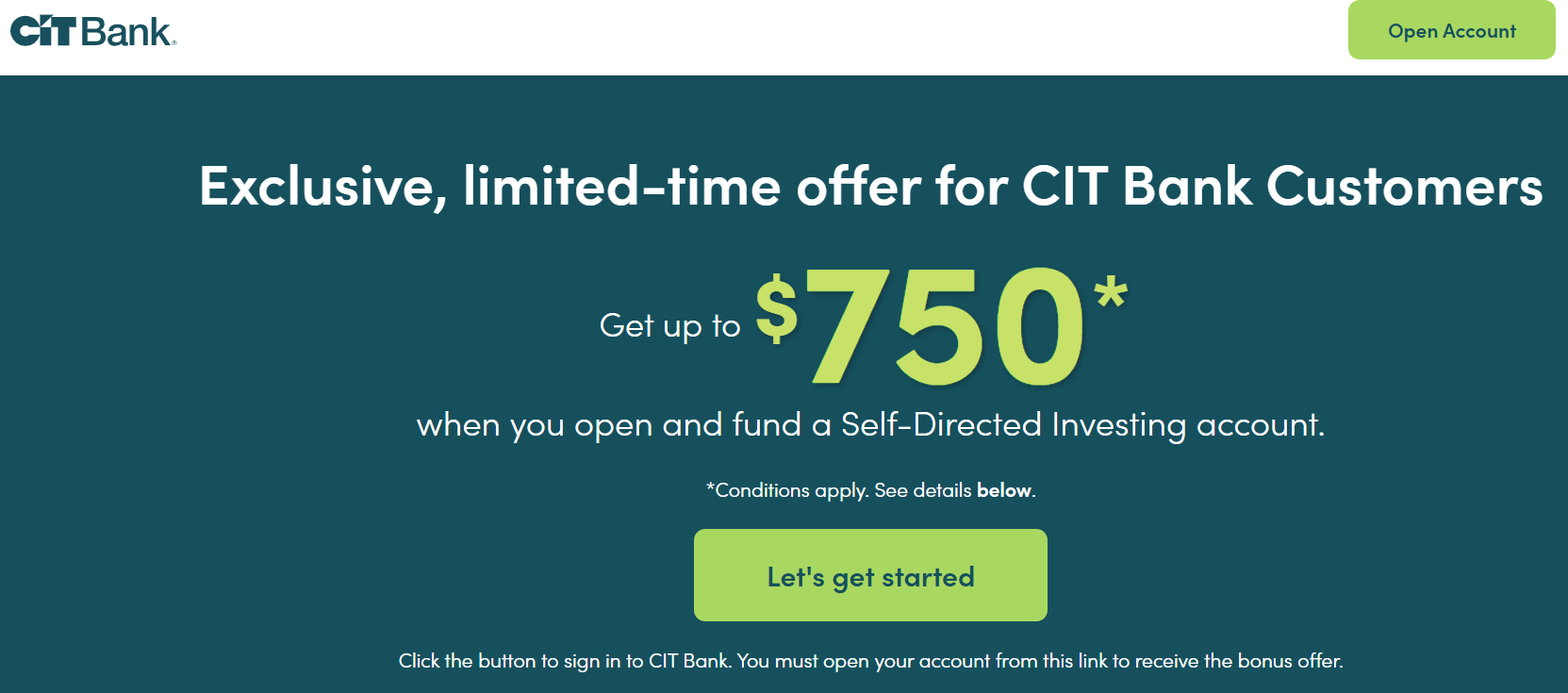

The Offer

- CIT Bank is offering a bonus of up to $750 when you open a self-directing investing account via First Citizens Wealth. The SDIA initial opening deposit must be maintained for a 60-day qualifying period from account open date in order to qualify for the bonus. Bonus tiers are as follows:

- $25 for $1,000-$4,999

- $50 for $5,000-$9,999

- $100 for $10,000-$49,999

- $200 for $50,000-$99,999

- $350 for $100,000-$249,999

- $750 for $250,000+

{kind=link}

The Fine Print

- Limited-time offer. One bonus per CIT Bank customer. If multiple Self-Directing Investing accounts are opened by a customer, only one account will be eligible for the bonus. Offer is non-transferable. The Promotion begins on December 5, 2024 and can end at any time without notice.

- Offer valid when a CIT Bank customer with an existing savings or eChecking account opens a new Self-Directed Investing account offered through First Citizens Wealth after December 5, 2024 and provided that the following requirements are met:

-

- The First Citizens Self-Directed Investing account (SDIA) is opened with the initial funding deposit to earn the corresponding bonus with new funds not on deposit with CIT Bank. A customer can open an SDIA account with a minimum of $100 but will need to open the account with at least $1,000 to qualify for the bonus of $25.

-

- The SDIA initial opening deposit must be maintained for a 60-day qualifying period from account open date in order to qualify for the bonus. Any losses or gains due to trading or market fluctuation will not be taken into consideration when calculating the qualifying deposit amount.

- CIT Bank will deposit the qualifying bonus into the customer’s Savings or eChecking account within 30 days following the 60-day qualifying period.

- The bonus for which the customer qualifies will be deposited to the customer’s CIT Bank savings or eChecking account within 30 days of fulfilling the promotion requirements in the SDIA account. If a customer has more than one CIT Bank savings or eChecking account, CIT Bank will choose the account in which to deposit the bonus.

- Customer will be deemed ineligible for a bonus payment if the SDIA is not initially funded with an amount to qualify for the bonus, the qualifying deposit is withdrawn or the account is closed prior to the end of the 60-day qualifying period. The CIT Bank savings or eChecking account must also be opened at the time of the bonus payment in order to qualify.

- Bonus payments are reported as interest earned on IRS form 1099-INT for the calendar year in which it was paid. Recipient is responsible for any applicable taxes.

-

Our Verdict

The nice thing about this bonus is that it only requires a hold period of 60 days, most other brokerage bonuses are much longer. Downside is that the bonuses themselves are much smaller. If you don’t mind juggling these accounts then this is worth doing but personally I prefer my investments to just be set and forget. Can also get $100 by opening the deposit account first.

Hat tip to 14lopeza

View Comments (47)

ACAT transfers don’t seem to count?

is it only for cash transfers or securities transfers also count?

Might as well get a hundo to open the deposit account first

https://www.doctorofcredit.com/cit-bank-100-checking-bonus-direct-deposit-not-required-new-existing-users/

Added

@2 May wanna add to post so ppl can double dip bonuses

Not working?

What instructions? It just takes me to my regular login showing my checking and savings which I opened up for their bonuses back in May and June of this year.

I finally figured it out. Click on the bonus amount you want and seems like nothing is happening, then within 5 seconds it will take you to the application page.

According to the link the promo code / offerid is: Wealth-SDIA

no idea how to actually get to the page where it allows me to open a brokerage account tho. I click on the "Let's get started" button and it takes me to the login page. I do, but it just brings me to my dashboard with my newly created checking account with no instructions to open a new brokerage account or anything about the promotion. Tried with different browser and disabling the adblocker. nada.

Got it too. I clicked the link to Get Started but never saw the bonus amounts.

PSA: I used a different browser without ABP and uBlockOrigin and also deactivated my Ad blocking PiHole and received a previously unseen webpage.

Bunch of details to add in for a measly $50 but at least it's $50 for a 60 day SGOV set & forget investment.

I got the same thing few days ago when I tried.

Hey, can anyone confirm if this promo kicks off on Dec 5, 2024? And does that mean it’s running long-term without a close deadline? I’d love to grab it, just short on cash right now. Thanks!

Looks like one of the rare brokerage bonuses available for IRAs. Anybody know if the bonus is deposited into the IRA?

where do you see that this is eligible for an IRA? This page says you can't open a new one with them. I'd bet this is only for a taxable brokerage.

https://www.cit.com/cit-bank/resources/products-and-rates

> New IRAs are not available. Current IRA customers and beneficiaries may rollover or open IRA savings and IRA/Roth CDs, excluding Premier High Yield Savings, Money Market, Savings Connect, Savings Builder, Platinum Savings, No-Penalty/11-Month CD and 6-month CD.

Shows several options for IRAs at the beginning of the application when choosing which type of account to open.

How did you get that screen to show up? I only see my dashboard upon login and not an account opening workflow

https://www.doctorofcredit.com/cit-bank-first-citizens-wealth-up-to-750-brokerage-bonus/#comment-2129314

"CIT Bank will deposit the qualifying bonus into the customer’s Savings or eChecking account within 30 days following the 60-day qualifying period."

The online application does not offer a way to transfer securities to fund the account...

A little weird that bonus is based only on initial deposit? Most brokerage bonuses are based on total transfers within n days of opening.

Also: If you have a P2, maybe better to divide and conquer, e.g. $20k combined deposit gets $200 combined bonus, same as single player would earn on $50k deposit.

This offer isn't worth it. Why is it posted on DoC?

Best bang-for-buck tiers(Bonus beats HYSA interest)

Not worth doing (compared to HYSA at 4.5%)

For these, the fixed bonus % return is too low. You’d make more leaving the money in a high-yield account.

"Why is it posted"? Really? You've been here long enough to know all types of offers get posted. There's plenty I don't care about but others do. Do you post the same thing on all brokerage bonuses?

It's not like the money is just sitting there. People invest it, whether that's stocks, bonds, money market funds, etc.

I don't do brokerage bonuses particularly because I have no investments. I only have cash. So this offer isn't good for me since the rates are terrible for 60 days.

Would it be wise for me to dump 100k into SGOV and earn 4.4% whole doing this bonus?

Matter of fact, can I actually do that? Would putting 100k in sgov in this cit investment account count towards the bonus? I would also earn whatever dividends it pays out right which comes out to 4.4%?

Yes. SGOV is an ETF that holds ultra-short-term U.S. Treasury bills (0-3 months maturity). It’s considered very low-risk, extremely liquid, and its current yield is around 4.4% annualized.

If you buy SGOV inside the CIT brokerage account after funding it, the market value of SGOV shares would still count toward the “assets in account” requirement for the bonus, just like cash or other eligible securities. While holding it, you’d receive monthly dividends from the T-bills it tracks — which is where the ~4.4% yield comes from — for as long as you own it.

That’s why many people use SGOV or similar T-bill ETFs for brokerage bonuses: you meet the funding requirement, keep risk minimal, and still earn some yield while you wait out the holding period.

@guest_2119924 Are you in this one my friend?

I am trying to figure out if transferring securities from another brokerage firm would work here? Or is it just for cash transfer?

@guest_2119311 from the terms it looks like cash only. They specifically say “initial funding deposit with new funds” and keep referring to deposits, not ACAT. No mention of transferring securities like other broker promos usually have. So I’d assume ACH/wire cash in to qualify, not transfer of existing holdings.

Thank you for clarifying.

Blessed are the spoonfeeders. :)

I’d rather be forked.

forking leads to too many child processes

Because this bonus can have an underlying asset not cash? I'm not sure why you're comparing to 4.5% APY when there is a 5% APY account and you're not considering that the assets will also earn during that period.

For the initial deposit, do I push from another bank or will this First Citizen Wealth pull from my bank?

Unless I am missing something, this offer isn't very good. If I did the $10,000 deposit then I would get the $100 bonus. But I would be missing out on $75 worth of interest. So it would be a net gain of $25?

You would either be transferring over existing stocks or cash (which can be invested into a fund like SGOV) to trigger the bonus.

There's a $100 outgoing transfer fee which partly offsets the bonus... so only do this as a temporary holding brokerage if you intend to transfer out to somewhere that will cover the fee!

https://www.firstcitizens.com/personal/investments/self-directed-investing

Where do you see the fee schedule?

The fine print refers to it, but they failed to link to it directly. I found it at First Citizens here:

https://www.firstcitizens.com/personal/investments/self-directed-investing

Thanks! I wonder if that's for partial AND full outgoing transfers or just full. I don't see any mention of a closure fee, so I'd probably guess they would just assess it for full account transfers?

https://www.firstcitizens.com/content/dam/firstcitizens/pdfs/hosted/wealth/self-directed-investing-fee-schedule.pdf

You need to liquidate and transfer out cash to avoid this fee.

That probably works for some folks (as long as there isn't account closure fee -- they have an inactivity fee). For me, I would be transferring assets in-kind and don't want to incur capital gains from liquidation.