{kind=link}

VantageScore is a three digit number that aims to aid creditors with their lending decisions. It was created on 14th of March, 2006 by the three national credit bureaus (TransUnion, Experian & Equifax). The exact same formula is used by each of these bureaus, but there can still be discrepancies between an individuals scores as the bureaus collect and maintain their own sets of credit data. There has been a total of three different revisions of VantageScore 3.0 (released in 2013), 2.0 (released in 2010) and 1.0 (released in 2006).

Contents

FICO & VantageScore

FICO (Fair Isaac Corporation) was not involved in development of VantageScore but in April of 2006 an internal FAQ about VantageScore was released by an employee of FICO. It mostly deals with how the implementation of VantageScore may impact FICO’s scoring business. Despite the credit bureaus investing in VantageScore and advertising it heavily on their websites it failed to gain much traction it’s currently used in less than 10% of lending decisions.

VantageScore Range

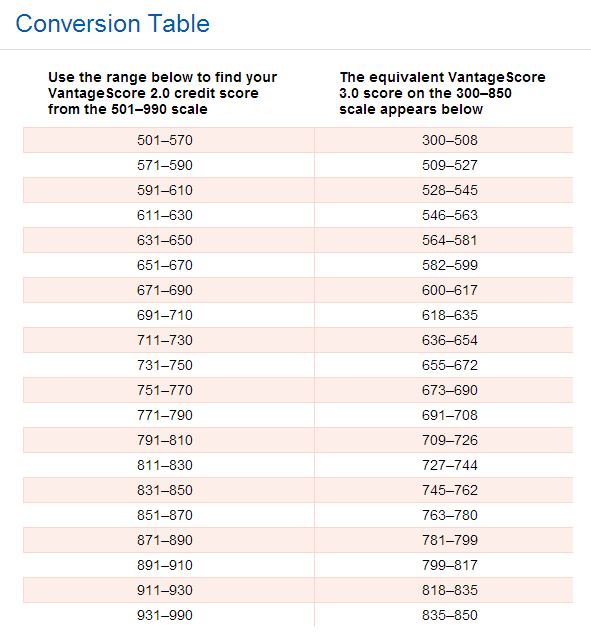

One reason for the lack of adoption was that VantageScore 1.0 & 2.0 had an unusual scoring range of 501-990. Because creditors were used to the FICO score range of 300-850 they had to update a number of their approval rules and regulations, most creditors decided it was easier to stick with FICO instead of making this transition.

In 2013 with the introduction of 3.0, the score range has moved to the more traditional 300-850 (the higher the score, the more likely a borrower is to be approved for credit – the inverse also being true).

{kind=link}

| Vantagescore range | Vantagescore versions |

|---|---|

| 501-990 | 1.0, 2.0 |

| 300-850 | 3.0 |

VantageScore Scale

VantageScores are also given an A-F scale. We’ve included this

A-F Rating VantageScore Range For Version 1.0 + 2.0 VantageScore Range For Version 3.0

| A-F Rating | Range For Version 1.0 + 2.0 | Range For Version 3.0 |

|---|---|---|

| A | 900-990 | 819-850 |

| B | 800-899 | 727-818 |

| C | 700–799 | 655-726 |

| D | 600–699 | 546-654 |

| F | 501–599 | 300-545 |

How Is A VantageScore Calculated?

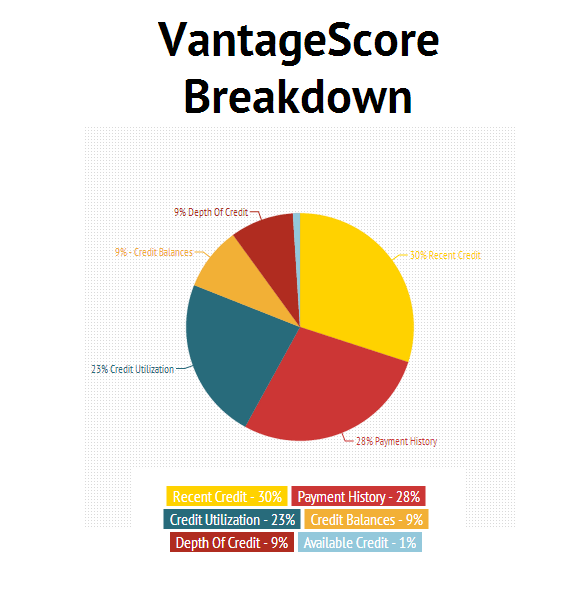

The VantageScore website used to list the exact percentage breakdowns of each scoring factor. Since the introduction of 3.0 in 2013 this has been removed and replaced by the following categories:

Extremely Influential

- Payment history

Highly Influential

- Age & Type of Credit

- % of Credit Used (also known as credit utilization ratio)

Moderately Influential

- Total Balances/Debt

Less Influential

- Recent Credit Behavior and Inquiries

- Available Credit

If one of the above categories doesn’t apply to an individual, the other categories will be readjusted automatically.

Despite the exact percentage breakdowns being removed from the VantageScore website, they are still available on the VantageScore section of Experian.

Experian may not have updated this information correctly.

{kind=link}

| Category | Description | Weight |

|---|---|---|

| Payment history | how timely and consistent your payments are | 28% |

| Credit utilization | debt-to-credit ratios and how much credit is available | 23% |

| Credit balances | what your total debt is; most likely, delinquent debt is counted more harshly than current debt | 9% |

| Depth of credit | length of credit history and types of credit previously received | 9% |

| Recent credit | how recent and many new hard inquiries and new accounts there are | 30% |

| Available credit | how much credit can be accessed, for example, could you spend $50,000 of credit tonight or within the next week | 1% |

For example, age, religion, race, gender, salary, post code, assets, occupation and a number of other factors aren’t used in calculating your VantageScore.

How To Access VantageScore?

Currently VantageScore is only available through two out of three of the consumer reporting agencies (Experian & TransUnion both offer it, whilst Equifax no longer offers it). The same formula is used by each of the agencies so as long as the data in an individuals credit report is the same across the board it’s not necessary to check it with each of the consumer reporting agencies.

Free VantageScore

Consumers can now access their TransUnion VantageScore for free through CreditKarma.com. Users will need to input their full name, address and social security number to get access to this data. The CreditKarma VantageScore is based on data provided by TransUnion. They also offer a FAKO score, so make sure you’re looking at the VantageScore tab.

Paid VantageScore

Consumers can also pay for their VantageScore through Experian. They sell this product for $7.95 or you can pay $14.95 and also get your Experian credit report. It’s important to remember that consumers are entitled to one copy of their credit report from each bureau once every twelve months.

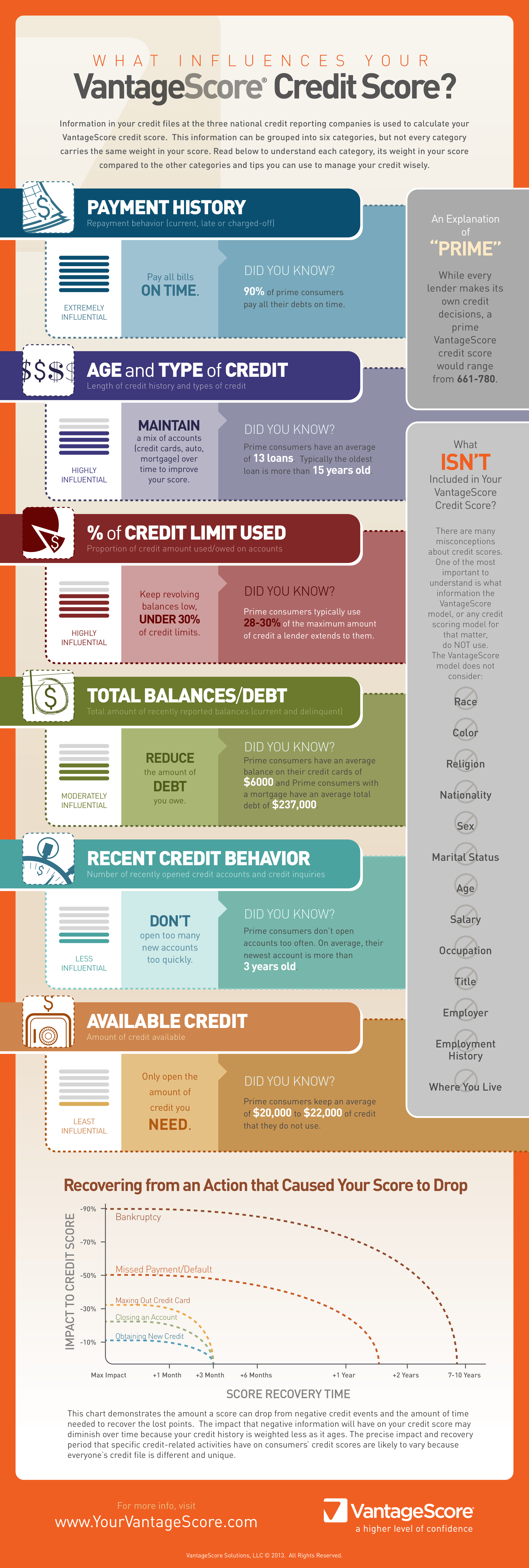

VantageScore Infographic

The following infographic is provided by VantageScore and can be viewed on their official website by clicking here.

{kind=link}

View Comments (2)

Seems to generate higher scores than FICO from the same inputs. Can be a difference between exceptional and acceptable values, your credit report accompaniment number may thus overstate creditworthiness to be encountered when actually applying for anything.

It depends. My vantage used to run about 50 points higher than my FICO. Now it runs 10 to 30 points LOWER than my FICO. I think this is mostly because Vantage counts new accounts at 30%, whereas FICO only gives them 15%. In the beginning your Vantage grows faster because you can't get many accounts and your credit age increases every single month, but then later on Vantage will hit you for 20 or more points every time you open a new account.

Good news is that it's a pretty quick recovery, and very few lenders use it.