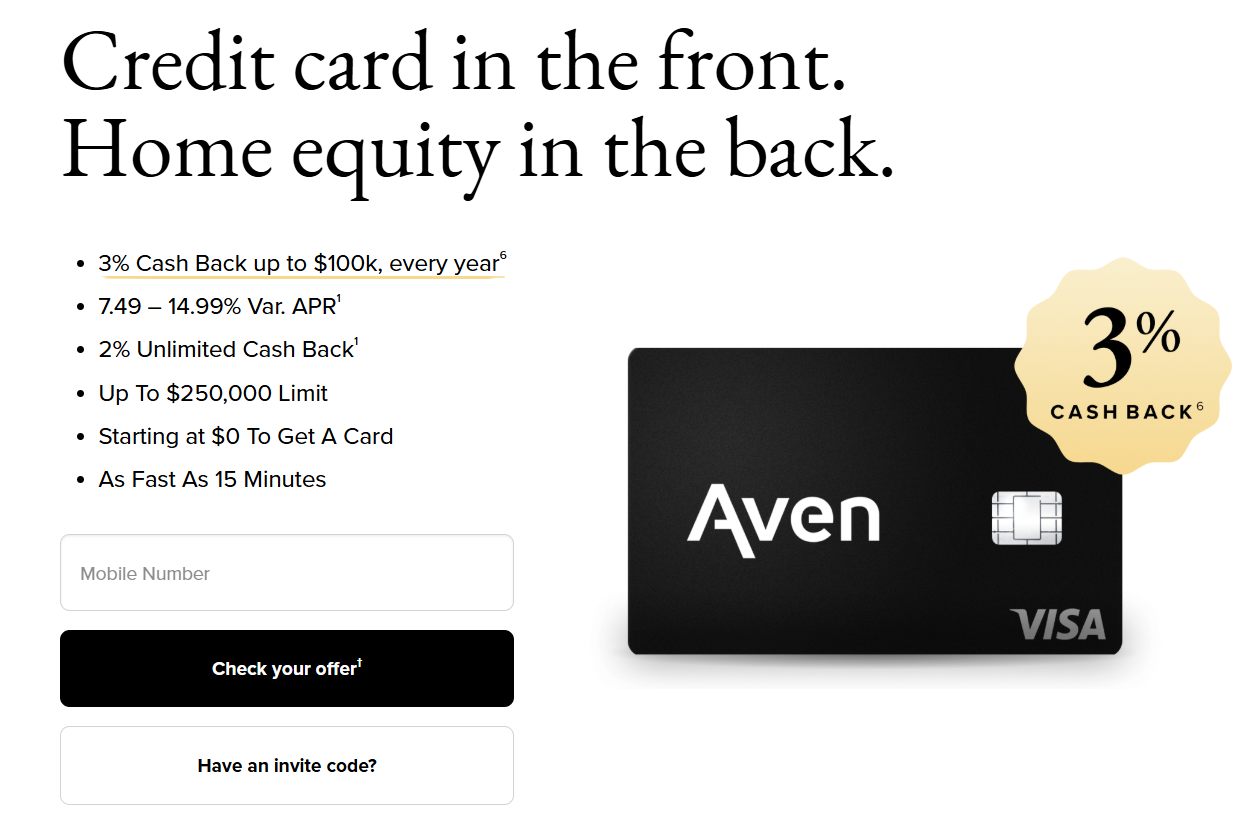

Aven has launched a credit card. Card is slightly different as it’s linked to your home equity. Card basics:

- No annual fee

- Card earns 3% back on all purchases on up to $100,000 in spend per year, then 2% unlimited cash back (must be enrolled in AutoPay)

- 7.49 – 14.99% Var. APR

- Cash Out (draw to bank account) fee and Balance Transfer fee is 2.5% of amount transferred

{kind=link}

Our Verdict

It does say you can check your offer without a credit check so they must be doing a soft pull on your credit and then a hard pull if you go ahead and apply for the product. The 3% cash back is obviously interesting, I suspect you might also be able to get large credit limits as it’s tied to your home equity. This could help boost your FICO score. Could also be useful as a HELOC alternative. Some users are already familiar with Aven due to the $5 weekly gift card offer for those with high credit scores.

Hat tip to reader Tony Q

View Comments (72)

Seems to be directly competing with this https://www.rocketcard.com/

They do have a credit card offer without linking it to your home equity. I used a different link and applied for a credit card, and the terms were 3% cashback up to $10,000/year. They gave me a $12K credit line. They also tried to push me toward their home equity card (not a true credit card) with a higher limit and the same 3% cashback. They gave me the option, so I stayed with the credit card only, not the home equity option. The terms were similar to other credit cards (grace period, etc). I have a referral link that will give a $200 bonus when you apply for the credit card.

I'm interested in your referral

It requires invitation code, and I don’t have it.

Looks like it is this? (non referral) https://www.aven.com/asset

Discussion https://ficoforums.myfico.com/t5/Credit-Cards/Aven-Visa-Another-3-anything-card-up-to-10k-spend-yr/td-p/6802719

I scrolled down on the linked page, where it says it's a 2% card. Maybe it's talking about spending beyond the $100K. I think this is a must to avoid (apologies to Herman's Hermits).

Recommend caution here. My reading is that this is a home equity card, not a credit card, and that your line of credit is based on home equity.

I'm up to $75 on Starbucks and will milk this as long as I can. Wish I knew how to switch it to Dunkin.

Same, switching to DD would be great.

I've noticed subtle negative changes, a few weeks ago it was you only have 24 hours to claim the card, previously it was at any point once a week past. And just this week I had to watch a 30 second ad first to only get the link emailed to me(as opposed to taping to see it), and it was now buried further down in the app in hopes you (accidentally?) click/tap or check out some other garbage from them.

FYI multi-unit buildings aren’t covered. Funny because they keep sending me snail

Ail offers and claim to be all “automatic” in their processing… so why send targeting to an ineligible property

Their not in Texas yet

Just adding clarity. This is not a credit card. It’s an access card. As soon as you use it, purchase or not, interest assesses immediately and it’s unavoidable ie no 30 day float. I used to offer these in 2008 as a WF banker in a grocery store lol

This is not true. I pay my card off every month and am not charged interest. It’s a credit card backed by your equity - they open a lien against it. It’s not an access card.

Do they let you pay off charges as soon as they appear?

But how is that even logistically sound? What if there's a pending charge and it drops off? What if a merchant accidentally double charged you and had to remove a charge later? What happens to the interest? Sounds like a mess.

See my post below, looks like they calculate interest on the average daily balance of the prior month. So that would be slightly inflated if a charge posts but is removed a few days later. Pending charges are not a part of your balance and wouldn't incur any interest, they only decrease the amount of your available credit temporarily.

lol oh wow 🤯 aven just putting out wrong info.

They are looking for suckers to pay for my free coffee.

also unclear (from what i was able to find on the site): are you charged interest immediately on any purchases (like the upgrade cards), or do you have a grace period where they don't charge any interest as long as you pay your statement in full each month (like normal credit cards)?

This from the page about "How it works" seems to indicate you pay interest on your average daily balance from the last statement:

How to pay for charges made on a HELOC Card

Every month, you will receive a statement with your charges, much like you do with a traditional credit card. The monthly bill for a HELOC Card from Aven, for example, consists of 1% of the principal balance plus finance and interest charges on the average daily balance during your last billing cycle.

Also this:

While there are no restrictions on what products or services you can purchase with a HELOC Card, financial advisors typically advise against using your card on frivolous items or experiences, such as vacations or a new car, which are unlikely to increase your wealth. These types of purchases could even make it harder to pay off your HELOC balance in the future.

Wow that is a hard PASS on this one! I was mistaken below, this is def NOT a normal credit card.

I sign up for their app due to the $5 weekly gift card offer only to find out AFTER I signed up with their very invasive application that my state doesn't qualify and I'm on a "waitlist". Felt like a switch and bait.