A classic FICO score is a three digit number between 300 and 850, industry specific scores have differing ranges. It was developed by the Fair Isaac Corporation (now under the name “FICO”) in 1989 to help creditors quickly and more effectively judge an individuals credit risk. It’s currently used by more than 90% of all lenders and a total of over 100 billion have been sold worldwide to individuals and lenders. It’s increasingly being used outside of the financial arena by insurance companies, employers, landlords and even the armed forces to help them evaluate potential risks.

Contents

How Is A FICO Score Calculated?

How A FICO Score Is Broken Down

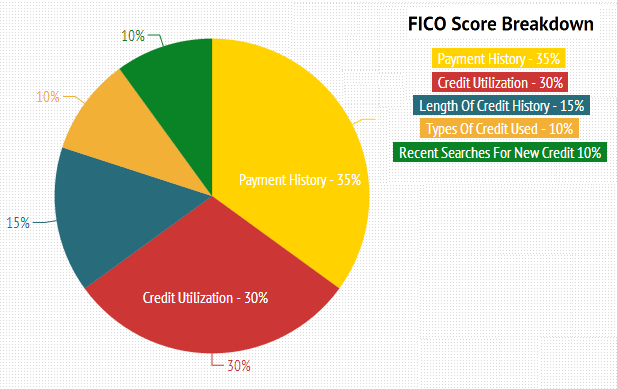

A FICO score is calculated by looking at the data found in an individuals credit report. Each individual actually has three credit reports, one from each of the credit bureaus (TransUnion, Equifax & Experian) meaning everybody actually has multiple FICO scores (in fact there are 49 variations on FICO scores read more about the variations of FICO scores). The data found in these credit reports is broken down into five categories: payment history, credit utilization, length of credit history, types of credit used and recent searches for credit.

For example somebody with a shorter credit history may have less emphasis placed on credit history length and more on their searches for new credit. The below percentages are based on the averages of the general population and are provided by FICO.

Payment History 35%

Payment history is the most important factor in determining FICO scores and accounts for ~35% of the total. Lenders want any money they lend to be repaid (with fees and interest of course) which is why such emphasis is put on the history of repayment.

If a payment is made late or not at all (referred to as a delinquency) the FICO algorithm will take into account the following in determining how much of a negative impact it will have:

- How late the payment was made

- How much was owed

- How recently it happened

- How many other late or missing payments there are

A track record of little to no late payments will lead to a higher FICO score whilst a history of late payments will result in a lower score.

Some lenders will even provide a discount if you set up automatic payments through your bank or credit card.

Credit Utilization 30%

Credit utilization ratio (amount of money borrowed divided by the total amount of credit available to them) accounts for 30% of a FICO score. Revolving credit (e.g credit cards) counts towards the majority of your credit utilization ratio (>95%+) whilst installment loans (mortgages or auto loans) count towards a very small minority (<5%).

Anecdotal evidence suggests (and this has been backed up many times by various people at the myFICO forums) that it’s best to have a credit utilization ratio of 0 on all of your accounts apart from one. This account should carry a balance but should be no more than 10%. It’s important to remember that credit utilization doesn’t have a history, so you only need to worry about it when you’re planning on applying for loans.

It may seem strange that it’s beneficial to have one account with a balance and this is because creditors are in the business of making money and if a consumer has zero money owing – they aren’t paying the high interest rates that credit cards command.

Around 90-95% of credit card companies will report the total amount owing that is shown on your monthly statement to the credit bureaus. If you’re unsure which number your credit card issuer will provide the credit bureaus and the credit card provider is unwilling to disclose this information then order a free copy of your credit report and check which figure they are reporting to be sure.

Length Of Credit History 15%

Credit history length makes up 15% of a total FICO score, but it’s not only the oldest account that is looked at. FICO takes into account the following factors:

- Age of oldest account

- Age of newest account

- Average age of all accounts

- How long since specific accounts have been used

The older the history of credit, the better the FICO score is likely to be. This is because it shows lenders that the borrower has displayed the same behavior over a long period of time.

Unless a credit account is costing money, keeping it open will increase the length of your credit history and thus help to improve your FICO score. After being inactive or closed for a period of 7 years these will fall off the credit report and no longer be counted so it’s important to make sure they stay somewhat active to keep them aging.

Recent searches for new credit 10%

Recent searches for new credit make up 10% of the FICO score algorithm. Having a lot of searches for new credit will negatively affect a FICO score because this behavior is considered risky by lenders. It’s weighted more heavily when not much other credit information is available.

An example is as follows: Cynthia is a 20 year old student who is new to having credit but struggling financially with two student loans. She her best course of action is to apply for a lot of loans to pay off her existing debt and for some extra spending money to see her through the next semester at university. The FICO algorithm would immediately see that she has very little credit history and apply more weight to the searches for new credit part of the score. Because she has applied for a lot of different loans in a short period of time she would receive a low FICO score.

Not only will opening new accounts negatively impact on the FICO score directly, they’ll also cause the average age and the newest account open to drop which will effect the score further under “credit history length”. Think before opening new accounts unnecessarily.

Soft Inquiries VS. Hard Inquiries

When applying for new loans it’s important to know what does and doesn’t count as a search for credit. There are two types of credit inquiries, soft (doesn’t affect credit scores) and hard (does affect credit scores). These are also sometimes known as soft pulls and hard pulls.

Both hard and soft inquiries allow a third party such as a creditor to view your credit report, but only hard inquiries will negatively affect your FICO score. A hard credit inquiry will stay on your credit report for a period of two years and stop affecting your FICO after a period of one year.

A hard credit inquiry is when a credit report is pulled to help aid in a lending decision. For example, when a consumer applies for a mortgage, the mortgage company will use a hard inquiry to access that consumers credit report. These hard inquiries stay on credit reports for up to two years and usually cause the consumers credit score to drop by a few points, as time progresses this penalty is slowly reduced. After two years the hard inquiry drops off an individuals credit report and no longer affects their credit score. An individual must authorize a hard inquiry is performed (simply applying for a credit card or other loan is considered authorization).

A soft credit inquiry is when a credit report is pulled but is not used in a lending decision. Ofttimes an individual won’t be aware that a soft credit inquiry has even been performed. An example of a soft inquiry is when a credit card issuer pre-approves an individual for a credit card. Individual’s accessing their credit scores also counts as a soft credit inquiry and doesn’t affect their credit score.

Types Of Credit Used 10%

Types of credit used accounts for 10% of an individuals FICO score. There are two main types of credit: revolving and installment. Lenders look for people for multiple types of credit. When industry specific scores are used (e.g bankcard or auto) the scoring model will give more weighting to the type of credit most similar to that specific scoring model (e.g bankcard models will give more weight to revolving credit whereas auto models give more to installment credit).

Revolving Credit

A revolving credit account has a predetermined credit limit that the owner can borrow up to. Interest is only paid on the amount borrowed and not the credit limit. Once money is paid back, it can be re borrowed (e.g Tony has a credit limit of $100, he borrows $50 and then pays it back with interest. He can now borrow up to a maximum of $100 again).

The most common type of revolving credit is a credit card. Other types include store cards and a line of credit for a business.

Installment Credit

Installment credit accounts have a fixed number of payments that must be made. Interest is paid on the whole amount owing, regardless of how much of the credit he borrower is actually using. Once money is paid back it cannot be re borrowed without refinancing. It’s usually used for a specific large purchase.

The most common type of installment credit is a mortgage or auto loan.

Types Of FICO Scores

In total there are 49 different FICO scoring algorithms that are made available to creditors to assist in their lending decisions, 9 of these are or were accessible to individuals. The reason there are so many different FICO scores is because there are a number of industry specific scores (34 in total) that are rarely used and don’t differentiate much from the 9 classic/generic scores. There are also 6 NextGen scores which are also rarely used by lenders and are not accessible to individuals.

Classic / Generic Scores

There has been four major revisions to the FICO score in 1995, 1998, 2004 and 2008. For every revision there is one classic or generic score for each of the three bureaus. Because the 1995 model is no longer accessible to consumers and no longer used by any creditors we no longer count these as one of the 49 FICO scores.

This leaves the revisions in 1998, 2004 and 2008, because there are a total of three credit bureaus and they all have their own credit data this gives us the 9 credit classic credit scores that are/were available to consumers.

Industry Specific Scores

The main difference between industry specific scores and classic scores is the range that these scores fall into. An industry specific score falls between 150-950 whereas a classic score falls between 300-850.

In 1998 & 2004 all three of the bureaus also introduced four different industry specific algorithms (Installment loan, Bankcard, Auto & Personal Finance) this is a total 24 industry specific FICO scores which are only available to creditors for the ’98 and ’04 models.

The 2008 revision saw the removal of the Installment Loan & Personal Finance FICO scores by TransUnion & Experian and the additional of the Mortgage FICO score by all three bureaus, this accounts for the other 10 industry specific scores.

NextGen RISK Scores

Next generation scores (commonly known as NextGen Risk scores) also follow a range of 150-950. There has been two revisions to NextGen (first in 2001, the second is unknown) and whilst FICO claims that these scores can help the number of approved loans whilst decreasing the number of delinquencies it is rarely used by lenders and is not available to individuals. There is a total of six NextGen scoring models (two for each of the credit bureaus).

For example, a score based on TransUnion data using the 2004 model would be called TU-04. If it is an industry specific model, this would be added to the end. For example if it was using the Auto model it would be TU-04 Auto.

You can find more information on the different types of FICO scores on these sections of our website: “How Many FICO Scores Are There?” & “Types Of FICO Scores“.

Free FICO Score

There are many ways to get a free FICO score, with more being added constantly. Rather than keeping this page updated with the latest methods, I’d recommend reading our full post on the subject.

Paid FICO Scores

Through myFICO.com

myFICO.com is the official website for consumer products that FICO makes publicly available. One of their products is called “Score Watch” and allows access to a consumers Equifax Classic FICO 2004 score (also known as a Beacon 5.0 score or EQ-04) as part of the 10 day 4.95 trial.

Click here to sign up for a $4.95 10 day trial.

If it’s not cancelled you’ll be charged $14.95 per month. We suggest saving a copy of your score and then calling 188-577-5978 to cancel, it’s also possible to cancel online. The trial can also only be made use of once every 24 months so it’s not something you can continually sign up for to check your score.

Alternatively all three FICO scores can be purchased for $19.95 per score ($54.85 for all three, a saving of $5. Make sure you check for promo codes first as this can further reduce the price) through their FICO Standard and FICO Score 3-Report View. It’s generally not necessary to have a score from each of the three bureaus if there is minimal differences between each of the credit reports from the three bureaus.

If you purchase your scores through myFICO you’ll actually be receiving the following scores:

- BEACON 5.0 (Equifax)/ EQ-04

- Experian, FICO Risk Model 08 (Experian) / EX-08

- FICO Risk Score, Classic 98 (TransUnion) / TU-98

Despite the different names, these are all FICO scores and are all scores either lenders look at or extremely close to those that they do.

A lot of websites will claim to give you free credit scores in exchange for signing up to their credit monitoring program or similar. Unless otherwise stated these will not be FICO scores and thus will be unlikely to be the same scores that lenders use to approve or deny your loan application.

All of the individual credit bureaus give access to FAKO scores if a consumer signs up for their credit monitoring program, these are not the same as a FICO score and are not the same as the scores the majority of lenders look at.

FICO Score Range

A FICO score ranges between 300 and 850, with 850 being the best score a consumer can achieve and 300 being the worst. FICO score categories are further broken down grades such as “excellent” (the best grade achievable) and “poor” (the worst grade given).

| FICO Score | Grade |

|---|---|

| 720-850 | Excellent |

| 700-719 | Very Good |

| 675-699 | Good |

| 620-674 | Fair |

| 560-619 | Bad |

| 500-619 | Very Bad |

| 300-499 | Poor |

Table 1.0 FICO Scores And Their Respective Grades

It may seem unusual to group scores into these ranges, but it makes sense when it’s put into practice. One of the things lenders use these scores for is determining what interest rate will be offered, it would get extremely complex and difficult to manage/maintain if everybody was offered a different rate based on their individual score so instead lenders use these grades (or ranges) to work out an individuals interest rate.

| FICO Score | Grade | Typical Mortgage Rates* |

|---|---|---|

| 720-850 | Excellent | A |

| 700-719 | Very Good | A + 0.13% |

| 675-699 | Good | A + 0.65% |

| 620-674 | Fair | A + 1.80% |

| 560-619 | Bad | A + 4.30% |

| 500-619 | Very Bad | A + 5% |

Table 1.1 Is The Same As Table 1.0 With Typical Mortgage Rates Included

As evidenced by table 1.1 as a consumers score decreases the interest rate they are offered increases exponentially. Scores below 500 aren’t graded or given a typical mortgage rate as borrowers with these scores are almost never approved for loans, unless they are geared to people with bad credit in which case a FICO score is generally not taken into account.

Industry specific scores and NextGen scores have a range of 150-950.

What Is A Good FICO Score?

Again if by looking at Table 1.0 or 1.1 it’s possible to see that a good FICO score is anything between 675 and 699, but it’s safe to say that anything above 675 can be considered a good score.

FICO Score Facts

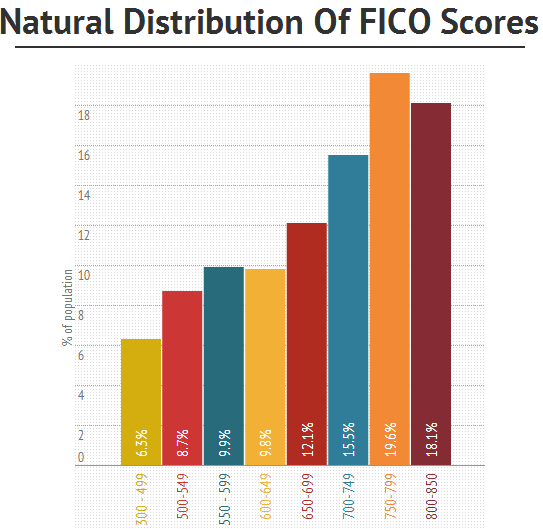

| FICO 8 Score | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 |

| 300-499 | 6.6 | 6.5 | 7.1 | 7.2 | 7.3 | 6.9 | 6.3 |

| 500-549 | 8 | 8 | 8 | 8.2 | 8.7 | 9 | 8.7 |

| 550-599 | 9 | 8.8 | 8.7 | 8.7 | 9.1 | 9.6 | 9.9 |

| 600-649 | 10.2 | 10.2 | 9.7 | 9.6 | 9.5 | 9.5 | 9.8 |

| 650-699 | 12.8 | 12.5 | 12.1 | 12 | 11.9 | 11.9 | 12.1 |

| 700-749 | 16.4 | 16.3 | 16.2 | 16 | 15.9 | 15.7 | 15.5 |

| 750-799 | 20.1 | 19.8 | 19.8 | 19.6 | 19.4 | 19.5 | 19.6 |

| 800-850 | 16.9 | 17.9 | 18.4 | 18.7 | 18.2 | 17.9 | 18.1 |

- Minimum score is 300

- Maximum score 850

- The median score is 723 (meaning half of the people have scores above 723 and half below)

- Follows a left skewed distribution (~60% of scores are between 650 & 850)

- Mean score of 693

The above information and graph was taken from the FICO analytics blog. No data has been released for 2013 yet.

Other Names For FICO Scores

| Credit Reporting Agency | FICO Score |

|---|---|

| Equifax | BEACON® Score |

| Experian | FICO® Risk Score |

| TransUnion | FICO® Risk Score (Formerly EMPIRICA®) |

F.A.Q’s About FICO Scores

Below are some of the most frequently asked questions about FICO scores, if you’ve got an unanswered question don’t worry, just contact us and let us know your question and we will answer it.

Question: I seem to have different FICO scores from different sources, what gives!?

Answer: The first thing to make sure of is that you are comparing FICO scores from the same credit bureau. There are a total of three bureaus: TransUnion (TU), Equifax (EQ) and Experian (EX).

The second thing to make sure of is that you’re comparing scores from the same time period. For example, if you pull one score three months before the other then there are three months of reasons as to why the scores could be different.

Even if you are pulling scores at the exact same time, there might still be a difference though and here’s where things get a little bit more confusing. You need to make sure you are comparing credit scores from the same credit bureau and to also ensure they are calculated using scoring models developed in the same year. There are four major revisions ’95, ’98, ’04 & ’08. So your TU-98 score is likely to be different to your TU-04 because they’ve slightly changed the formula used to calculate the score.