The Offer

Update: Plastiq has confirmed that this promotion is targeted to those who it was sent to via email.

Plastiq is sending out an email with the following promotion.

- Get two rent or mortgage payments with no service charge when you schedule six months of payments and pay with a Mastercard

The Fine Print

- Valid through March 31 (must schedule the six payments by that date)

- Cancellation of a promotion-qualifying schedule will result in a charge of the waived fee amount

Our Verdict

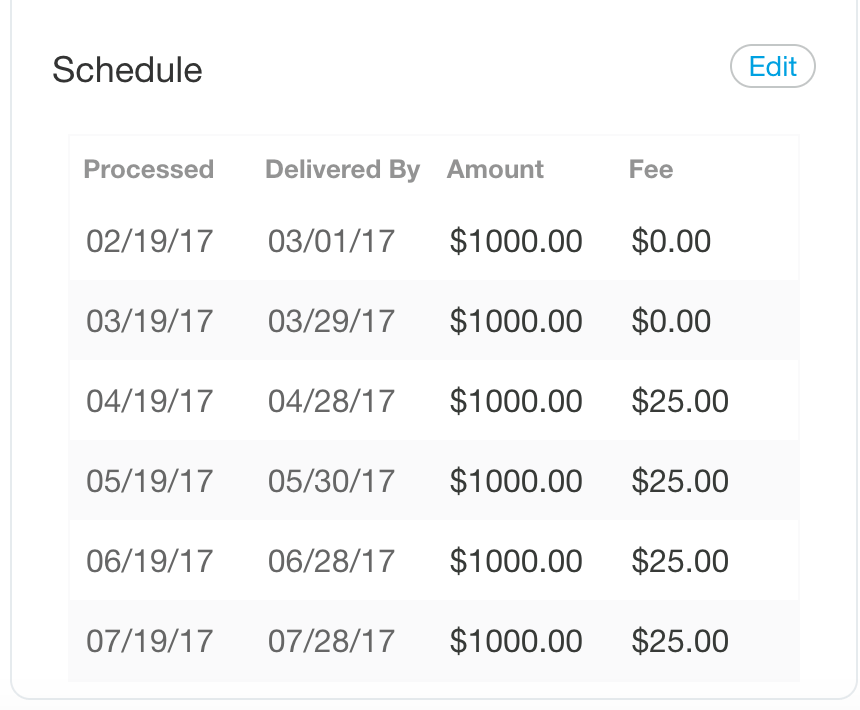

The Plastiq fee for Mastercard is usually 2.5%, but sometimes it’s 2% for some bills/people. With this promotion, you’re getting a 33% discount on the fee since two out of six are free, so you’re total average cost is either 1.66% or 1.33%.

Not bad, but limited usability since it’s Mastercard only and the charge is spread out over six months.

If you use a card that earns 2% like the Double Cash Mastercard or Barclay Arrival+ Mastercard, you’ll have a small gain overall. Assuming a 1.66% rate, you’ll net .33% on each payment. If you have a $2,000 monthly rent or mortgage you’ll net almost $7 per payment or ~$40 for the full schedule of six payments. Even better would be if Plastiq works to get 3x with AT&T for a cost of just 1.66% (.55 cents per point). It seems to vary by payee with some payments earning 3x and some not.