Update 5/6/25: Chase is back (update: not working again)

Most credit card issuers now allow you to view cards that you’ve been pre-approved for online. Here is a full list of issuers that do allow this, along with the relevant websites/contact information.

Just because you’ve been pre-approved/pre-qualified, doesn’t necessarily mean you’ll be approved, credit card issuers will do a hard pull on your credit report before they approve you and if your circumstances have changed you might be denied for a card they’ve pre-qualified you for. Click here to find out what these terms actually mean.

For those just wanting the links, here is the short list. Keep reading on for more information on all of the pre-qualifaction finders.

- American Express (personal)

- American Express (business)

- Bank of America

Barclaycard(currently not working)- Chase

- Capital One or this link (might provided more offers)

- CardMatch

- Chase Pre Qualified Offers

- Citibank

- Discover

- US Bank

- Wells Fargo

Contents

American Express

You can find out if you have “any special offers waiting for you” by going to https://www.americanexpress.com/ then clicking card offers and entering your full name, address and the last four digits of your social security number. You can view this page by:

- Click “cards” in the top bar

- Click “view all Personal and Charge cards”

- Click “Check For Pre-Qualified Offers”

If you don’t see this promotion then it’s likely than you’re signed into your account. I’d recommend either signing out or using an incognito mode window.

It’s also possible to check for small business cards. You can use this link or follow these directions:

- Click “cards” in the top bar

- Click “View All Small Business Cards”

- Scroll to bottom of the page and then enter your information where it says: “See if you qualify for a special offer”

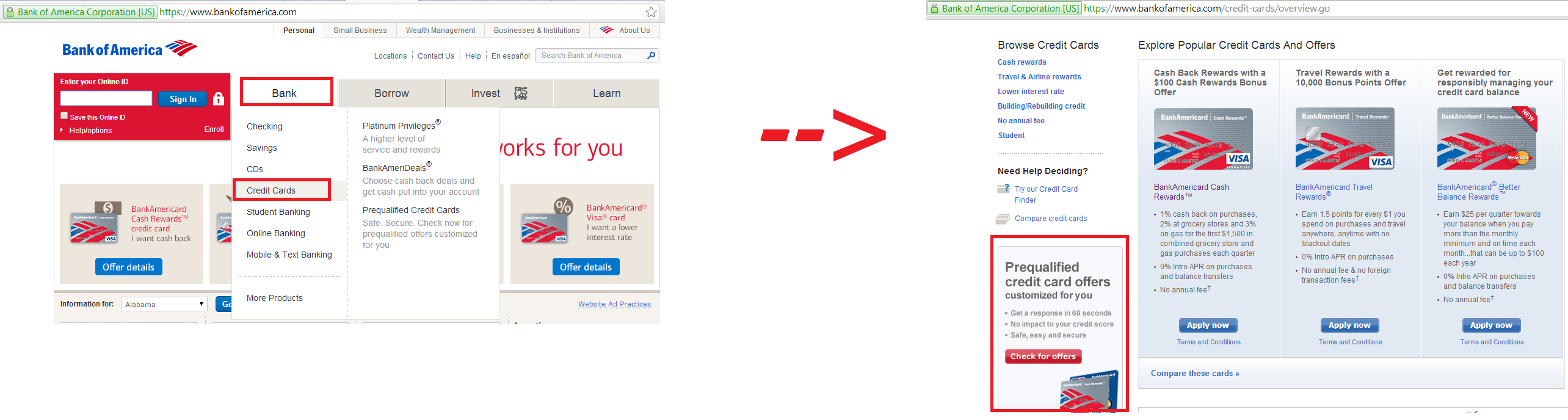

Bank of America

You can view what offers you are pre qualified for with Bank of America by clicking here. You’ll need to enter your full name, address, birth-date and the last four digits of your social security number. You’ll also need to let them know what type of credit cards you’re interested in and if you’re already one of their online banking customers.

You can view this page from the homepage of the Bank of America website by:

- Click “Bank” in the header, then click “Credit Cards”

- Click “Prequalified credit card offers” in left sidebar at the bottom

Barclaycard

Unfortunately Barclaycard have currently pulled their pre-approved checker.

To view your Barclaycard pre-qualified offers click here. You’ll have to provide your basic information (address, full name, social security number, how you rate your credit, what type of benefits you value most). If you see a screen that says “Congratulations” then you are pre-approved for those offers, if you see a screen that says “Recommended” then you have no current pre-approved offers from them.

Capital One

To view what offers you are pre-qualified for click here. You’ll need to provide your full name, zip code and the last four digits of your social security number. You also need to tell them your favorite credit card benefit and how you rate your credit level. To view this page from the Capital One homepage do the following:

- Click “Credit Cards”

- Click “See If You’re Pre-Qualified”

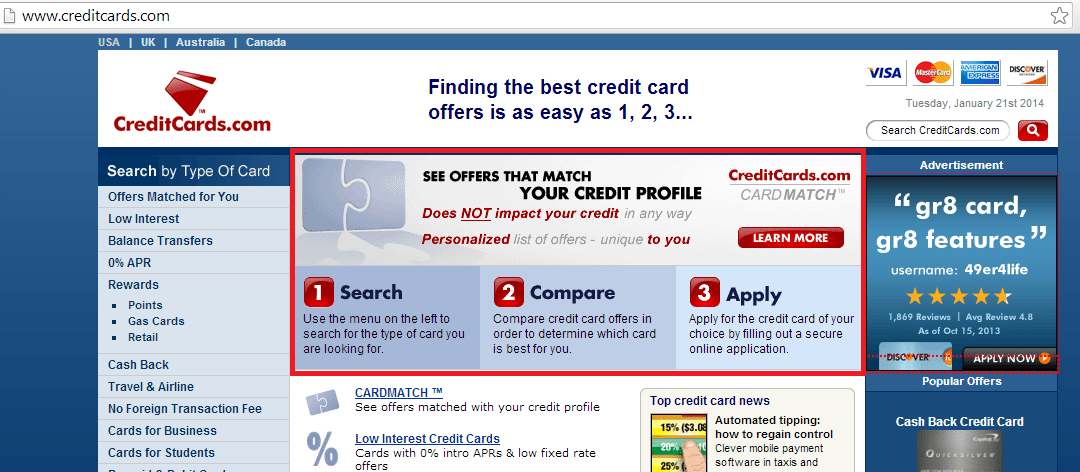

CardMatch by CreditCards.com

The CardMatch tool was developed by CreditCards.com in an effort to reduce the amount of websites you need to check for pre-qualified offers. They also sometimes run specials where the sign up bonuses are greater through their tool than elsewhere. You need to enter your full name and address, along with the last four digits of your social security number. Click here to check your offers with CardMatch. You can get to the CardMatch tool for the homepage of CreditCards.com by doing the following:

- Click the card match tool on the front page

Chase Pre-Qualified Offers

You can also check to see if you have any pre-qualified offers from chase by clicking here. You’ll need to provide your full name, address, zip code, city, state and last four digits of your social security number.

You can also access this page from the chase homepage. To do so follow these directions:

- Click “Product And Services” in the header

- Click “Credit Cards” in the drop down menu

- Click “All Credit Cards” in the side menu

- Click “Check for Pre-Qualified Offers”

the credit card section of the chase website, this is the third link in the left sidebar (screenshot below).

Citibank

Citibank

You can view all your pre-approved offers from citibank by clicking here. As always, you’ll need to enter your full name, address and last four digits of your social security number. You’ll also need to choose which credit card benefit is most important to you. To view this page from the citibank homepage follow these directions:

- Click “Credit Cards” in the header

- Click “See If You’re Pre-Qualified For An Offer”

Credit One

Credit One is a sub prime lender and as such most of their cards have high fees and interest rates. We’d suggest you look into a secured card instead of going with them, but they also have a pre-qualified card finder you can use by clicking here. You can reach this page from the homepage with the following directions:

- Click “get pre-qualified” which is found in the right sidebar, second box down.

Discover

Finding out the offers you’ve been pre-approved for with Discover is simple, just click here and fill out: first name, last name, last four digits of your SSN and answer two simple questions.

You can also get to the above page by navigating to it from the discover homepage, to do so:

- Click credit card home, which is the first link on the far left of the footer links (at the very bottom of the page)

- Scroll to the middle of the page and click “See your personalized offer”

- Fill out the information and view your personalized offers

USAA

Little bit different to the other card issuers here, as you need to be an existing member to qualify. If you are do the following:

- Log into your account

- Search for ‘offers’

- Select ‘My Offers Page’

- They’ll show pre selected offers here

You can find out more about USAA here.

US Bank

Update: This has been removed for now.

US Bank recently re-added their pre-qualification checker, which you can view by clicking here. You’ll need to enter your full name, address and last four digits of your SSN. You’ll also need to tell them what you look for most in a credit card. You can find this page from the homepage with the following directions:

Click “Credit Cards & Prepaid Cards” which is the third link to the left in the header.Click “Credit Cards” which is first link in the pop down menuClick “Check for Recommended Offers” in the main body of the website

Wells Fargo

Wells Fargo has added a tool to check for pre-select offers, you can log in using your Wells Fargo account or just use your details. Click here to see if eligible.

HSBC

HSBC has recently readded the pre-qualified checker. Click here to see if you’re pre-qualified

Smaller Card Issuers

Here are the direct links for a number of smaller card issuers/store credit cards.

- BB&T

- Deserve.

- FNBO

- Goldman Sachs (Apple & GM Cards). They don’t have a pre-approved checker, but they will show you your credit line before doing a hard credit pull.

- Milestone gold (this is another woeful credit card, which we wouldn’t recommend)

We hope you found this post helpful, if you did why not let our readers know which credit cards you were pre-qualified for? And also let us know if you know of any other places people can check for pre-approved offers.

Bank of America not working. Goes into a forever spin (whether logged in or not).

Chase is dead again… worked earlier today for a little bit.

Doesn’t look like Chase is back. I’m seeing “We’re unable to check for offers because we’re updating our site”.

Anyone know how reliable Wells Fargo preapproval is? They say I’m pre-approved for about six different cards.

It’s been 100% accurate for me the last 3 applications.

Thanks for the info. I’m interested in their Signify CC, but it doesn’t show on my pre-approval list of cards. Do you or anyone else here have experience in applying for this card if it’s not displayed as one of their pre-approved cards for you?

I assume that since it’s a business card, it probably wouldn’t show up anyway.

I think it’s at least an actual pre approval, unlike Boa where you can make up fake info and it’ll still always show whatever cards they wanna push

Capital one sent me email about 100% guaranteed approval before credit pull. It worked! Usually it was pre-approved then declined.

Worked for USBank. Pre-approved for Cash+. After application process, several minutes later I received an email to stating unlock EQ. Received standard letter stating to call in. Approved via text. C+ card delivered within five days. This was March 3rd. Second USB CC in last 3 months.

Experian has a card match tool. https://usa.experian.com/myOffers/cards

Per the email they sent me, if they have “No Ding Declines”. However, none of them show up as “No Ding” for me.

“No Ding Decline

Apply with confidence knowing there’s no impact to your credit scores if you’re not approved.*”

Email fine print: “*Applying for cards labeled “No Ding Decline” won’t hurt your credit scores if you are not approved. Approval of your application will result in a hard inquiry, even if you’re unable to pass final verification, which may impact your credit scores.”

Seems like I would have had at least one since they emailed me about it. Bait & switch?

I once used Experian’s percentage match – had a 92% match with Wells Fargo Active Cash ==> declined. 😡

I played the “No Ding Decline” game using your link and “no-ding” results included two high-annual-fee Amex cards. The third card they showed me, one in which I am actually interested, did not have the “No Ding” label.

The US Bank tool gave me an error when I submitted my information initially, however, I received an e-mail shortly after indicating that I was pre-approved (Smartly card) and the offer is good for 15 days. Thanks DoC!

A quick and probably useful PS on the link I suggested in a comment below to check pre-qualifications for Capital One:

https://www.capitalone.com/credit-cards/compare/

(The link includes their entire CC lineup, hence is more comprehensive than the one posted in DoC’s article.) William Charles

William Charles

It turns out that even some co-branded cards with no “See if I’m Pre-Approved” link up front DO feature the link inside, if you click on “Card Details.” These include Bass Pro Shops, Cabela’s, Pottery Barn, et cetera. Needless to say, I just pre-qualified for and opened one more card this way today — my CC #45 in total (#5 with Cap One, and #11 in the last 6 months).

Wait, you mean you have a total of 45 credit cards, 11 of which were opened in the last 6 months?

Yep, whatever I do in life I try to beat EVERY possible record….otherwise it’s not fun!😂

Anyways, I only started this hobby a few years ago, and I humbly recognize I still have a looong way to go….😂

https://www.guinnessworldrecords.com/world-records/68577-largest-collection-of-valid-credit-cards

That is a LOT of credit cards.

Largest collection of valid credit cards (1,638 in April 2021)

I bet many people on here have more than 45 active credit cards. I’ve never counted mine so I may or may not be one of those people!

For PenFed, there is a “See if you pre-qualify” link on the Pathfinder Rewards CC sign-up page.

Caveat: PenFed’s prequalification tool is relatively new and still very unreliable.

By unreliable I actually meant the opposite situation, of many people reporting to have been pre-approved and then denied. When pre-approvals are not accurate, however, anything can happen either way after they take a HP and access a full report. In the end, it boils down to how much she cares about wasting a HP with Equifax (and/or Experian). If I were her, I’d probably look for another good signup bonus (there’s lots) and don’t bother with PenFed for the time being.