[12/4/17: Reposting to clarify that 5/24 does seem to apply to this card according to some data points.]

Chase and United teamed up for a new no-annual-fee credit card which earns 1.5% back in United credit on everyday purchases and 2% back on United flights. Rewards can be used to buy United flights.

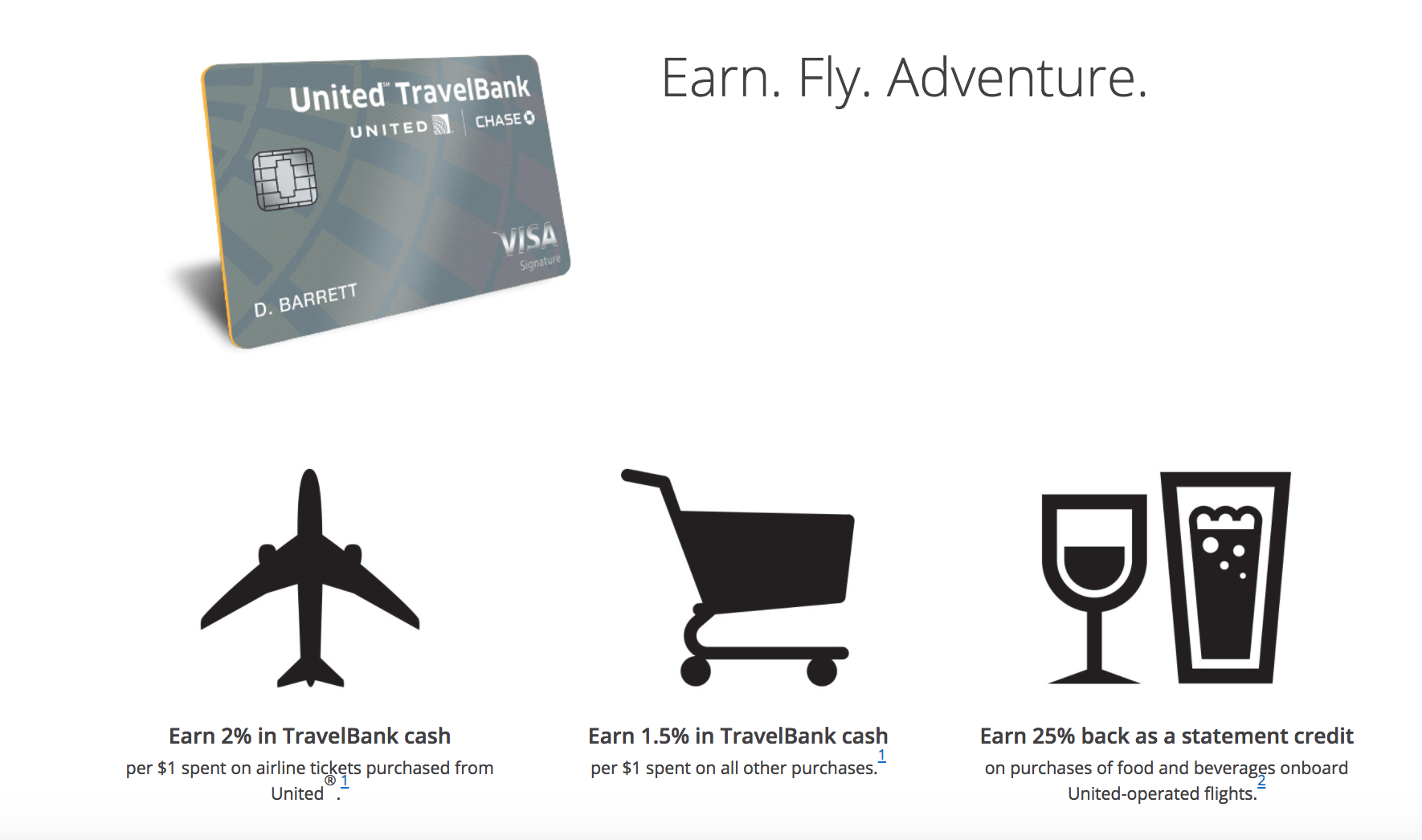

Rewards Details

- 2% back on United flight purchases

- 1.5% back on all other purchases

Rewards are not cash back, they are credits which can be redeemed for United flights.

- No limit to the amount of rewards you can earn

- TravelBank cash can be used alone or combined with select forms of payment during the purchase

Also, earn 25% back as a statement credit on purchases of food and beverages onboard United-operated flights.

Signup Bonus

- Signup bonus: Get $150 in TravelBank cash (United credit) after spending $1,000 within three months

Card Details

- No annual fee

- No foreign transaction fee

List of United Cards

United now has eight card offerings:

- United MileagePlus Explorer Card

- United MileagePlus Club Card

- United MileagePlus Explorer Business Card

- United MileagePlus Club Business Card

- MileagePlus GO Visa Prepaid Card

- United TravelBank Card

- Only available for product change: Chase United MileagePlus Rewards No Annual Fee Card

- Only available for product change: Chase United MileagePlus Awards Visa Signature

Both the Explorer cards come with a $95 annual fee, both the Club cards come with $450 annual fee, the prepaid card and TravelBank card have no annual fee.

Final Thoughts

I can’t see much reason why someone would get the TravelBank card since you can get cards which earn 2% cash back everywhere, like the Citi Double Cash card. Still, there are a few interesting thing about the card:

- $150 signup bonus

- No foreign transaction fee (most basic cards do have a 3% foreign transaction fee)

- 25% rebate on in-flight food purchases (maybe some people spend a lot on hard drinks or whatnot in-flight?)

- This card could be an interesting option for downgrading if you no longer want to pay the annual fee on the card. This might be the most interesting thing about this card – might even be possible to downgrade and subsequently upgrade when you need it, save the annual fee and don’t lose a 5/24 card.

The elephant in the room is still unknown: will this card be subject to 5/24? The other United cards are subject to 5/24, and data points indicate the card does fall under 5/24 (1, 2).

Read more on Business Insider