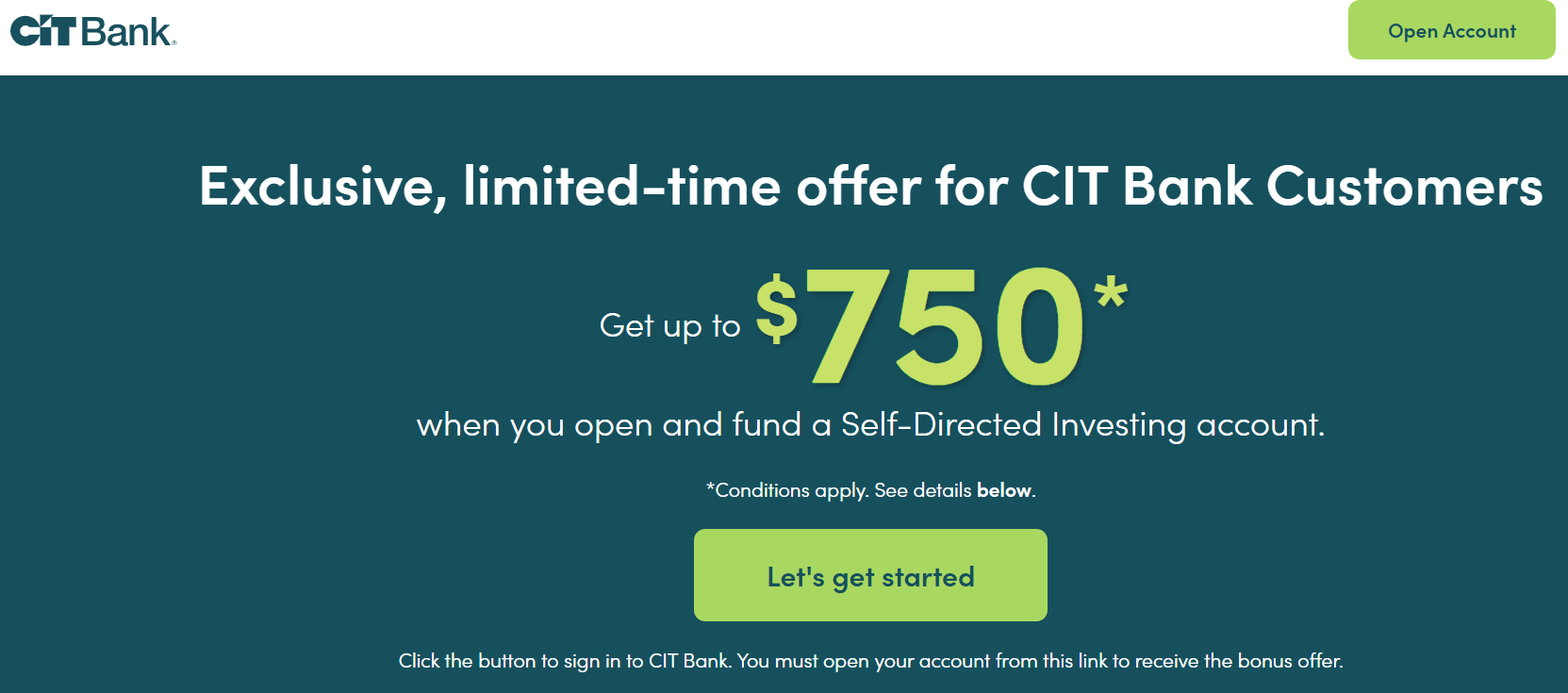

The Offer

- CIT Bank is offering a bonus of up to $750 when you open a self-directing investing account via First Citizens Wealth. The SDIA initial opening deposit must be maintained for a 60-day qualifying period from account open date in order to qualify for the bonus. Bonus tiers are as follows:

- $25 for $1,000-$4,999

- $50 for $5,000-$9,999

- $100 for $10,000-$49,999

- $200 for $50,000-$99,999

- $350 for $100,000-$249,999

- $750 for $250,000+

The Fine Print

- Limited-time offer. One bonus per CIT Bank customer. If multiple Self-Directing Investing accounts are opened by a customer, only one account will be eligible for the bonus. Offer is non-transferable. The Promotion begins on December 5, 2024 and can end at any time without notice.

- Offer valid when a CIT Bank customer with an existing savings or eChecking account opens a new Self-Directed Investing account offered through First Citizens Wealth after December 5, 2024 and provided that the following requirements are met:

-

- The First Citizens Self-Directed Investing account (SDIA) is opened with the initial funding deposit to earn the corresponding bonus with new funds not on deposit with CIT Bank. A customer can open an SDIA account with a minimum of $100 but will need to open the account with at least $1,000 to qualify for the bonus of $25.

-

- The SDIA initial opening deposit must be maintained for a 60-day qualifying period from account open date in order to qualify for the bonus. Any losses or gains due to trading or market fluctuation will not be taken into consideration when calculating the qualifying deposit amount.

- CIT Bank will deposit the qualifying bonus into the customer’s Savings or eChecking account within 30 days following the 60-day qualifying period.

- The bonus for which the customer qualifies will be deposited to the customer’s CIT Bank savings or eChecking account within 30 days of fulfilling the promotion requirements in the SDIA account. If a customer has more than one CIT Bank savings or eChecking account, CIT Bank will choose the account in which to deposit the bonus.

- Customer will be deemed ineligible for a bonus payment if the SDIA is not initially funded with an amount to qualify for the bonus, the qualifying deposit is withdrawn or the account is closed prior to the end of the 60-day qualifying period. The CIT Bank savings or eChecking account must also be opened at the time of the bonus payment in order to qualify.

- Bonus payments are reported as interest earned on IRS form 1099-INT for the calendar year in which it was paid. Recipient is responsible for any applicable taxes.

-

Our Verdict

The nice thing about this bonus is that it only requires a hold period of 60 days, most other brokerage bonuses are much longer. Downside is that the bonuses themselves are much smaller. If you don’t mind juggling these accounts then this is worth doing but personally I prefer my investments to just be set and forget. Can also get $100 by opening the deposit account first.

Hat tip to 14lopeza