I talk about credit cards and I talk about them a lot. I love learning about the nuts and bolts of how the industry works, one thing I’ve been asking myself and researching recently is how much are co-branded credit card partners actually paid by the credit card issuers.

Contents

Types of Partners

There are really two types of credit card partners:

- Partners that just provide their brand name. You see this a lot with charities and not for profit organizations, they will offer their name to credit card issuers and receive a small kick back for doing so. In this case the brand usually does most of the promotion (on their own website and through newsletters and functions) and the credit card issuer provides them with an income stream. These are usually called “affinity card programs”.

- Partners that provide points/miles and brand benefits. These are probably the co-branded credit cards that you’re most familiar with (e.g Chase & United or American Express & Delta). In this case the branded partner will provide loyalty points/miles and in addition to that they will also provide increased benefits (e.g free baggage). These are usually called “co-branded card programs”.

Obviously there are some partners that are somewhere in between (e.g lots of chains stores will offer cards that earn at a higher rate at their stores and offer some type of benefit like early access to new products) but these are the two main groups.

Types Of Deals

There are basically four types of deals that partners can negotiate, now in most cases they will combine a number of these into a single deal.

- Approvals & activation. The credit card partner will received a fixed fee for every approved applicant (often the card also needs to be activated as well). This is often tiered as well to try and increase the number of applications (e.g 1-100 applications might receive a payment of $10 per approval, while 100+ will receive an payment of $11 per approval). In some cases the credit card issuer will only pay this out on leads the partner generates (e.g from their own website or mailing list) while in other situations they will pay it out on all approvals and activation’s. In even rarer cases the card issuer will pay out on an application, whether it is approved or not.

- Transaction volume. The credit card issuer will pay a fee based on how many transactions the cardholder makes in a specified time period (e.g month/year).

- Interchange fees revenue share. Card issuers typically make around 1.5% on all credit card transactions due to interchange fees, this will often be shared with the partner.

- Fees revenue share. Card issuers make a lot of money from various fees (e.g late, cash advance, interest charges, etc etc.) in this situation the card issuer will share a portion of these fees with the credit card partner.

It’s not just a one way street though, co-branded credit card partners will also provide the card issuer with things to attempt to increase the uptake of their card. For example, they might offer to pay half of the sign up bonus or acquisition costs, offer cardholders free benefits or elite status for meeting a spending bonus.

This makes a lot of sense when you think of this in terms of incentives that the credit card issuer has given the co-branded partner. For example, Citi might say to Hilton that they will receive 0.5% of all interchange fees and if a cardholders spends more than $40,000 they will give them a $500 bonus.

This gives Hilton a clear incentive to try and get cardholders to hit that $40,000 spend threshold, they can then decide to offer a special bonus for hitting this threshold. Hilton can then decide to give Diamond status to cardholders that hit that threshold as they are getting paid at least $700 from Citi for every card member that does this.

That’s just a fictional example, but it gives you a good idea of how and why credit card companies and their partners structure their deals like they do.

Payment Networks

In addition to partnering with a credit card issuer, these credit card partners also have to choose a payment network (e.g Visa, Mastercard, American Express or Discover). In some cases this choice will be made by the card issuer, in other cases it will be a joint decision or made solely by the credit card partner.

Different payment networks offer different benefits and protections, they are able to offer these because they earn about 0.15% of the total transaction. The most common benefits are things like zero liability protection and increased warranties.

Sample Deals

Now credit card issuers don’t normally make the deals they offer different partners public, but in some cases we can make a few educated guesses on how much these brands are actually being paid. Below are a few examples of the deals what credit card partners have.

Susan G Komen Foundation

Bank of America partners with this foundation for their Pink Ribbon Credit Card. What’s interesting is that on the fine print of this page, they actually disclose the financial arrangement that they have with Bank of America.

For each new Pink Ribbon BankAmericard Cash Rewards™ MasterCard® credit card that is activated within 90 days of opening, Komen receives $3. Komen also receives 0.20% of all retail purchases (less returns) made with the card and $1 for each annual renewal of the card.

The Pink Ribbon card is actually just a rebranded BankAmericard Cash Rewards card and Bank of America have extended this partnership to a lot of other brands (lots of universities and alumni associations). The card has no annual fee and earns 3% cash back on gas, 2% cash back on grocery stores (up to a combined limit of $1,500 in spending per quarter) and 1% cash back on all other purchases.

This is an example of an Affinity credit card partner and these are current rates that they are receiving. They might be receiving or giving something in addition to what we’ve published, but given how forthright they’ve been with the other information that is doubtful.

Other Affinity Examples

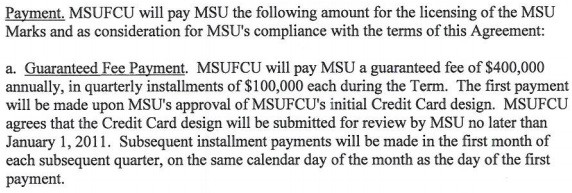

If you look at the credit card agreements for non profits/organizations they’ll usually clearly state the payment they receive in the terms. For example let’s have a look at Michigan State University Federal Credit Union & Michigan State University agreement.

Obviously this doesn’t give us much idea of how much they are making per cardholder, but $400,000 a year at minimum is a decent sum for a school that had a 2014 enrollment of ~50,000 new students.

Additional Reading

If you find this sort of stuff interesting, I’d recommend reading some of the following articles/resources:

- Frequent Flier Credit Cards Generate More Than $4 Billion for Major U.S. Airlines – A Report from IdeaWorks

- Anatomy Of a Co-Branded Credit Card by Finance Buff

- CRM Trends Article On Co-branded Credit Cards

- The Secret Sauce: How Your Airline/Hotel Credit Card Actually Works

Final Thoughts

I’d love to know about more affinity and co-branded partnerships and the terms they have, if you have any specifics (or can point me in the right direction), please let me know in the comments. Also let me know if you enjoy these sorts of articles in the comments, or if you’d prefer if I stuck to purely deals/actionable information.