Ever since the Synchrony Cathay Pacific card launched one thing that has always been asked in the comments is if the sign up bonus is churnable or not. We now have at least two data points of people getting the bonus multiple times: 1, 2, 3, It’s not 100% clear if you need to wait a set time between bonuses to get the bonus a second time but I do think you need to have closed your existing card before being eligible for a second card. If anybody has any other data points I’d love to see them in the comments below.

You may also like

[Targeted] Chase Cobrand Business Cards Spend Offers

(Update) Five Chase Travel Benefits On Hotel Booking With Chase Sapphire Reserve ($250+$250+$300+$100+Boost)

Wells Fargo Choice Privileges 60,000 Points

More Bilt Leaks & Bilt Statement

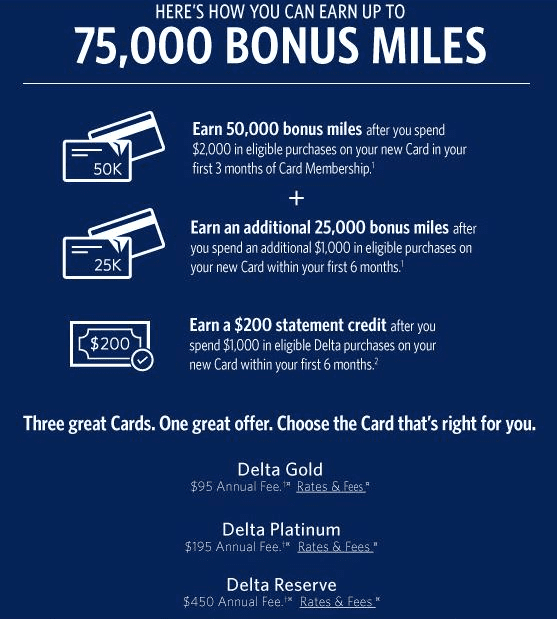

[YMMV] American Express Delta Offers – 90,000 Business Gold No Lifetime Language

Chase Marriott Bonvoy Boundless FIVE Free Night Certificates Bonus (Up To 50,000 Points Each)

Subscribe

41 Comments

newest