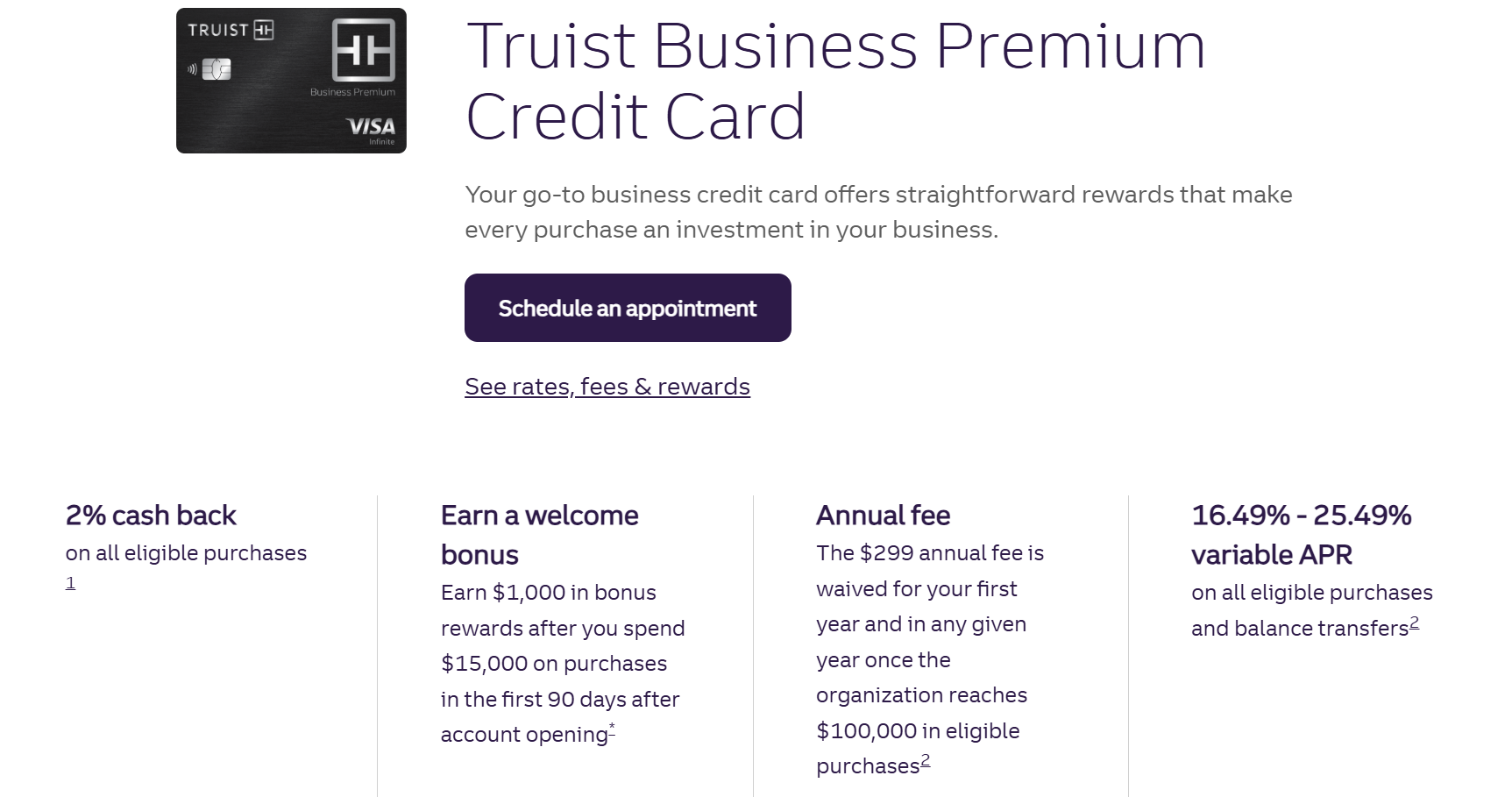

The Offer

- Truist is offering a $1,000 bonus after $15,000 in spend within 90 days

Card Details

- $299 annual fee, waived first year

- 2% cash back on all purchases

- Enjoy a 10% Loyalty Cash Bonus when rewards are redeemed into your Truist business deposit account

Our Verdict

Does require a large amount of spend, but at least the card itself earns 2%. If you spent the full $15,000 you’d earn $300 from the spend requirement and then another $1,000 from the bonus itself. Not sure what Truist’s business document requirements are but share your experiences in the comments below. This will be added to the best business credit card bonuses.

Hat tip to reader Bockrr