Deal has expired, view more Chase deals by clicking here.

The Offer

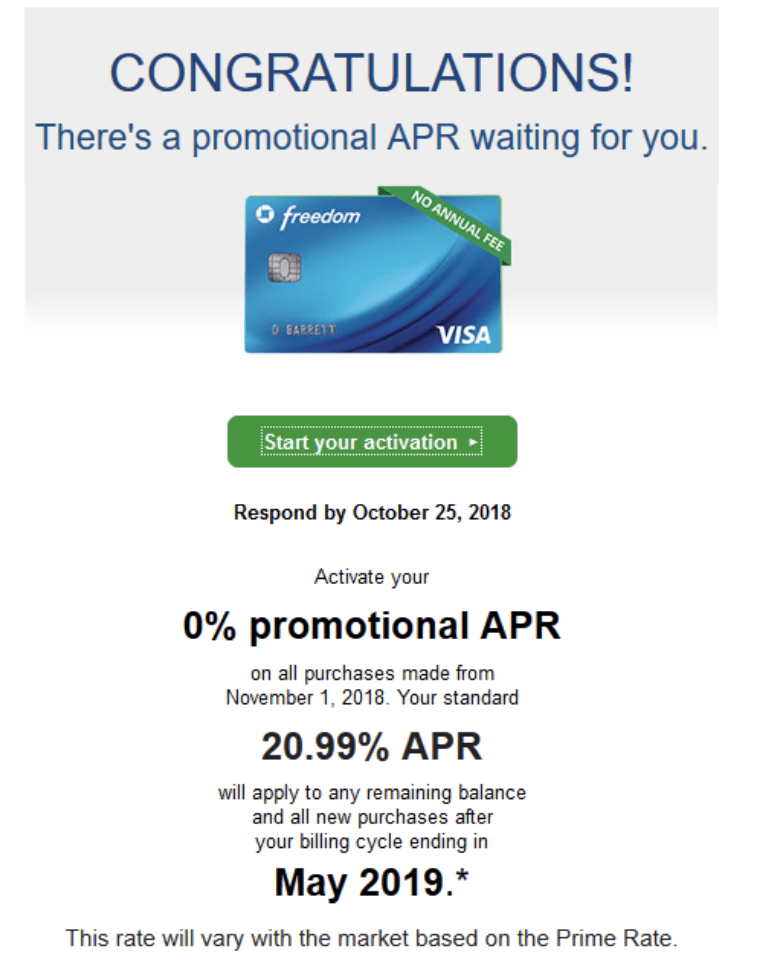

Chase sent out an email to customers with a low APR offer on various Chase cards like Freedom, Sapphire, and United.

- Get 0% APR on purchases made between November 1 and when your May statement closes.

The Fine Print

- Requires activation. To be eligible for this promotional offer, you must log on to the website referenced in this promotion and enroll by 10/25/18 by 11:59 p.m. ET.

- Promotional APR applies to all purchases that post to your account beginning November 1, 2018 through your billing cycle that ends in May 2019.

- Afterwards, your standard Purchase APR above will apply to any remaining promotional balances and new purchases.

Our Verdict

It’s basically a free 6-month loan if you pay it down before the close of the May statement. Personally, I stay away from these offers on personal credit cards since it negatively impacts the credit score.

Not everyone got the 0% offer. I got 4.99% on Freedom and others got 1.99% or 7.99%.