Effective September 15, 2017, Wells Fargo is adjusting some of the terms to its Online Access Agreement, which governs the use of online banking and the mobile app. The updates are unremarkable except for one interesting change: a new section governing predictive banking (section 13 at this link).

(The only other stimulating changes are to section 10(f), “Additional Terms Applicable to the ATM Access Code Service”, where Wells Fargo has decreased the time for investigating complaints or questions about ATM Access Code transactions from 90 days to 45 days, except in the case of new accounts where the 90 day timeframe still holds. They also fixed some brutal errors in the current Online Access Agreement: they’ve now bolded the introductory sub-subsection “Bank liability for failure to complete an ATM Access Code Transaction.” AND changed “If we ask you to put your complaint or question in writing and we do not receive it within 10 Business Days, we may not credityour account.” to include a space between “credit” and “your”.)

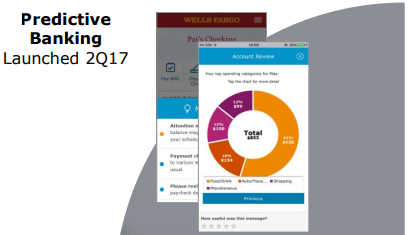

Predictive Banking

The long and short of it is that:

Wells Fargo may utilize predictive banking technology to look at credit and debit payments, as well as other banking transactions, and make suggestions based on this data. You may receive predictive banking notifications while logged in to WellsFargo.com, via email, or other means.

The publication American Banker also has an interesting article from early May about predictive banking (in general but with a focus on Wells Fargo, who’ve been working on this since 2014 or 2015). The basic goal is for Wells Fargo to provide insight to consumers based on their behavior & data – similar to any budgeting tool, but more expansive. Much like any major bank, Wells Fargo already offers a breakdown of spending by category, via their Money Map tool. Predictive banking would allow Wells Fargo to notify you that the funds in your checking account are insufficient to meet an anticipated expense (especially recurring payments, such as rent or other bills), or notify you that a paycheck you are expecting is late or of a different amount than usual.

Our Verdict

The possibilities inherent in predictive banking can be quite useful, given that many consumers do not check their banking accounts as frequently as they should be – making this a real tool for consumers who aren’t obsessively checking their accounts every other day.* You’d expect this to cut into Wells Fargo’s profit margins (less chance of overdrafts, &c.), so it will be interesting to see the full feature set once Wells Fargo fully announces it. (Of course, it’s always possible that a subset of consumers wind up relying on it too heavily, creating a potentially nasty trap when predictive banking doesn’t cover their ass.)

Your thoughts? Comment below.

* interesting tidbit: Wells Fargo’s average monthly sessions per active user (across mobile & online banking) was apparently 17 for 2016, up from 16 in 2015 and 13 in 2014. While that’s not very helpful without a median, standard deviation, and some data about time between visits, I still had no idea people checked their accounts that often!