Update 5/15/24: This is possible again.

Update: Seems to be a soft pull

Capital One now allows it’s cardholders to consolidate/reallocate credit limits between multiple cards within their online interface, in the past Capital One didn’t let it’s cardholders reallocate credit limits at all, so this is a massive improvement.

[Read: Rules For Reallocating Credit Limits With Different Credit Card Issuers]

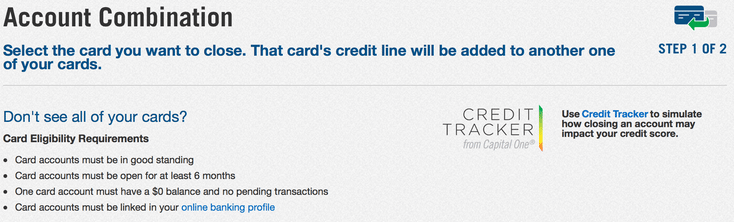

How To Use The New Feature

- Log into your account

- Go to the Services tab

- Click Request account combination

- Simplify your wallet

- Combine credit limits onto your preferred card

- Close cards you don’t use

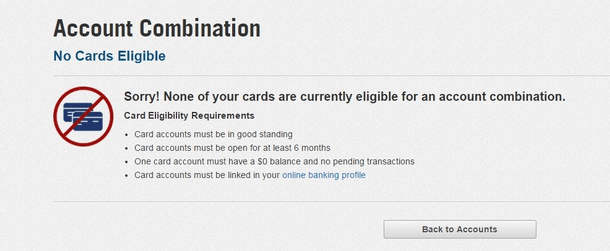

If you have no eligible cards (see requirements below) you’ll receive an error message.

Rules & Other Important Information

- Unsure if this is a hard or soft pull, please share your experiences in the comments. Data points:

- Soft pull: 1

- Hard pull:

- It’s supposed to take only five minutes for the account combination to occur

- Cards must be in good standing

- Cards must be open for at least six months

- One card must have a $0 balance and no pending transactions

- Card’s must be linked in your online banking profile

Final Thoughts

This is a significant improvement to what Capital One previously offered (nothing), Capital One did promise improvements when made two negative changes to redeeming rewards, so this is great firs step – hopefully they continue to make improvements. I actually think Capital One has the best system for credit reallocation and account closure out of all credit card issuers (American Express’ online system is also pretty good when it’s working). Hopefully this also puts pressure on other credit card issuers to improve their own reallocation and account closure systems.

I just wish Capital One wouldn’t do a hard pull on all three credit bureaus when you apply for a card, then they really would be much more competitive with Chase, Citi & American Express.

Hat tip to baller4life on myFICO forums