Update 8/1/25: Reposting as this has now been sent out via email as well. It appears confirmed that there are two groups of nerfs, one group who can still count their investment account and one group who can not. No one knows what causes someone to be in the ‘good nerf’ or ‘bad nerf’ group.

Update 7/27/25: Some cardholders have received letters that are actually different than what is listed below and actually requires a $100,000 balance in a checking account to earn the 4% (rather than $100,000 in checking, savings and investment). Hat tip to bogleheads

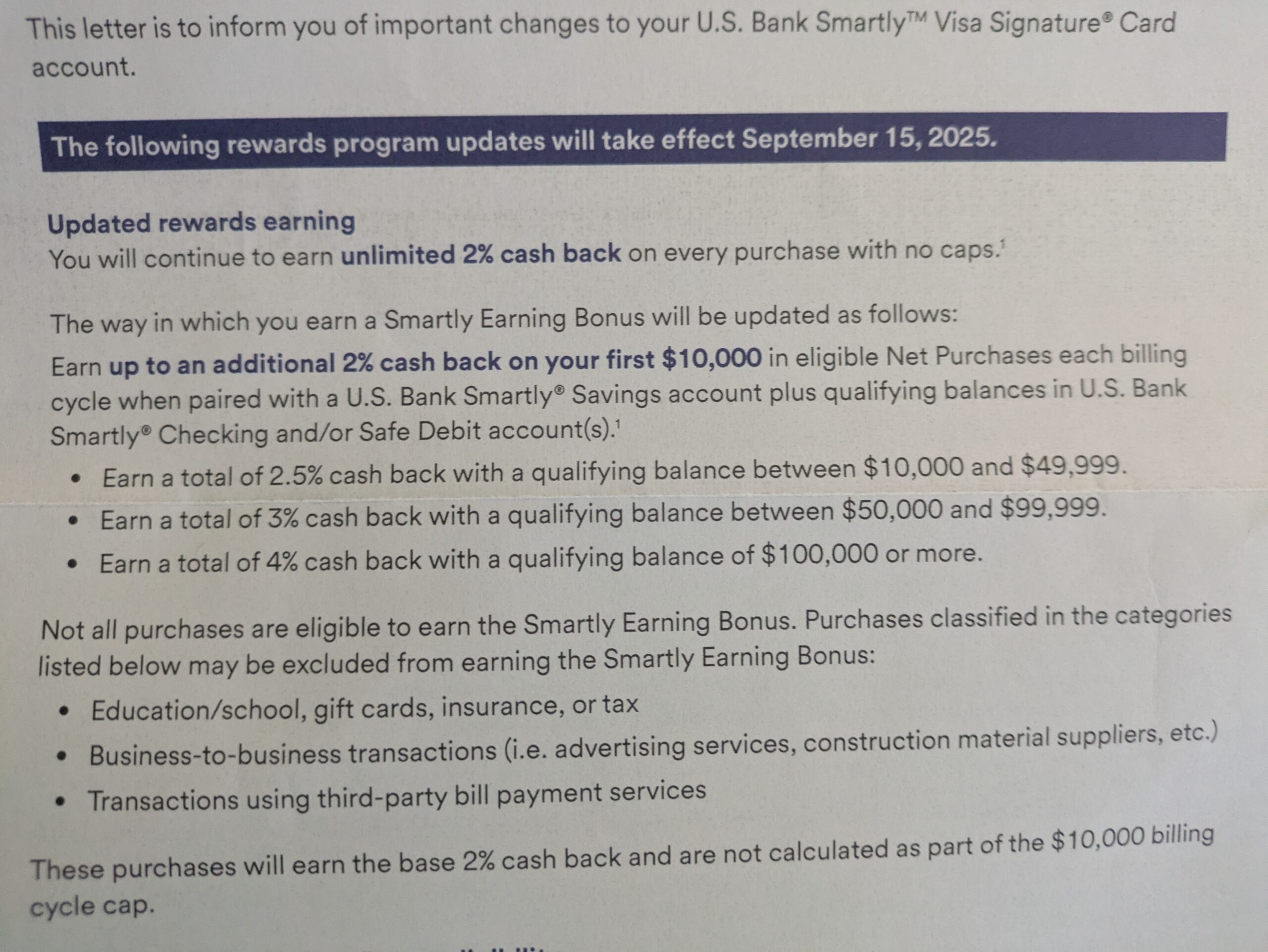

Original post: Earlier this year U.S. Bank made huge changes to the Smartly credit card, but the changes only applied to new applicants and existing cardholders were grand fathered in. Existing cardholders have now received a notice that this is changing, starting on 9/15/25:

- “earn unlimited 2% cash back on every purchase with no caps”

- “earn up to an additional 2% cash back [the “Smartly Earning Bonus”] on your first $10,000 in eligible Net Purchases each billing cycle when paired with a U.S. Bank Smartly Savings account and average daily combined qualifying balances in U.S. Bank deposit, trust or investment accounts” with $100K+ in qualifying balance required for a total of 4% cash back

- exclude* certain categories of purchases “from earning the Smartly Earning Bonus”: (1) “Education/school, gift cards, insurance, or tax”; (2) “Business-to-business transactions (i.e., advertising services, construction material suppliers, etc.)”; and (3) “Transactions using third-party bill payment services.” “These purchases will earn the base 2% cash back and are not calculated as part of the $10,000 billing cycle cap.”

Surprised they didn’t make these changes earlier in the year to be honest, this card was never sustainable.

Smartly Savings account rates just got cut, for those using that option like me for balances. 2% for $5,000. 2.5% for $50,000. 3.0% for $100,000. If you have another HYSA option over 4% and a flat 2% cash back credit card, you would now have to spend $4,000-$5,000 on the Smartly card per month just to break even due to the monthly interest loss.

CROSS-POSTING HERE AND ON “My Plan Going Forward With U.S. Smartly 4% Card”

Don’t give up hope just yet – cardholders from before April 14, 2025 may be getting grandfathered in to the terms they signed up with.

I received the bad latter. I called in to customer service to see if the letter I got was in fact accurate. Rep said it was. It was a short conversation. I got a survey, filled it out and just got a phone call back. Per the rep that just called me – nothing should be changing on my card, investment account will still count towards qualifying balance, no monthly limit of $10k, etc – basically I was sent the letter in error and nothing is changing on my card.

I guess we’ll wait to see what happens on September 16th. Perhaps this rep is mistaken, but she seemed to know her stuff and seemed pretty confident.

Plus, if it was a mistake, that is a huge amount of letters & emails that went out as a mistake.

If I was forced to gamble, and I do not gamble, I would bet the info you were given by that rep will turn out to be the mistake. I am also considering how much info I have received from phone reps that turned out to be inaccurate.

I hope I am wrong, and that the info you received turns out to be accurate.

Got the bad nerf letter. Had about $175k in spend on this card so far this year (tons of legit spend but also plenty of spend in their made up bad categories as I was putting any spend I could for my business on this card). Can’t say I’m surprised to be nerfed (beyond a general sense of surprise that they are actually somewhat good at filtering out people like me) but sure will be sad to see this one go.

Bad nerf = close up shop I guess huh? Don’t see a point in keeping anything open with them if there’s no reasonable way to keep getting 4% cash back.

Scoobs, thanks for sharing your experience. For sure, and as you expressed, it would not be recommend for someone to keep $100K in a nearly zero-interest checking account when we can make thousands of dollars in interest annually with that money elsewhere. We know for sure the Fed will lower the rate next month, but hopefully not too much.

Hopefully you have at a minimum a 2% unlimited spend cc, with no exclusions. And then make whatever you can via CD or savings account, etc., elsewhere on the $100K that would have earned only 0.005% in a US Bank checking account.

Yep makes sense. Back to the BofA card I suppose

can you share the good nerf letter as well?

https://rewards.usbank.com/benefits/card/SmartlyBenefits/program-rules#rewards-summary doesn’t seem to match the letters (no 10k cap or tax/edu/etc exclusions)

Now that US Bank Smartly is going to be nerfed for rent payments processed through third-party billers starting 9/15/25 for the 4% rate grandfathered people, I just opened up a third Bank of America Customized Cash Rewards Visa card. My third BofA CCR card will be 8.25% cash back rate in chosen category $2,500 max spend per quarter for one year, because of Platinum Rewards bump, and then be regular 5.25% rate after. It is currently 5.25% for my first two CCRs I opened in the past. From a rep on BofA phone call and from what I have seen posted elsewhere, if Travel category is selected, rent is covered as eligible for the higher cash back percentage if MCC Code is 6513. At least for now.

Also, if $1,000 minimum is charged on the card within 90 days of opening, a $200 cash back bonus will be issued.

Can anyone confirm if certificate of deposit is considered an investment account? Have 5 mo $100k CD.

Yes. I’m using the CD as well to park the cash. Here’s the line from their fine print:

Have “Combined Qualifying Balances” with U.S. Bank in open consumer checking account(s), money market savings account(s), savings account(s), CDs and/or IRAs, U.S. Bancorp Investments and personal trust account(s) (business accounts, commercial accounts, and the Trustee only (IFI) client relationship and other trust relationships do not qualify).

I would rather get 2% rollover match on $100k investment balance than getting additional 2% cashback for rollover $100k investment balance and spend $100k.

What’s the best way to dissolve the investment account assuming it’s mostly sgov? Transfer assets and pay a fee to close or liquadate, transfer cash out, and then close?

ACATS transfer to Robinhood. They are offering a 0.5% match and will reimburse your outgoing transfer fee.

This is the way. ACATS full transfer.

Let the new brokerage and your feet do all the talking.

So have we determined why some got the bad letter? Maybe not related to USB specifically but to credit report?

Seems like a coin flip to me. I didnt even get to max out 4% this year since my investment dipped in march from the sell off. So my rate was 2%-3% for quite a bit. Ive barely used the card on the excluded items, mainly for every day use.