The Barclaycard Arrival Premier is now live. Keep reading for more information, sadly you’re unlikely to like what you’re about to read.

Card Basics

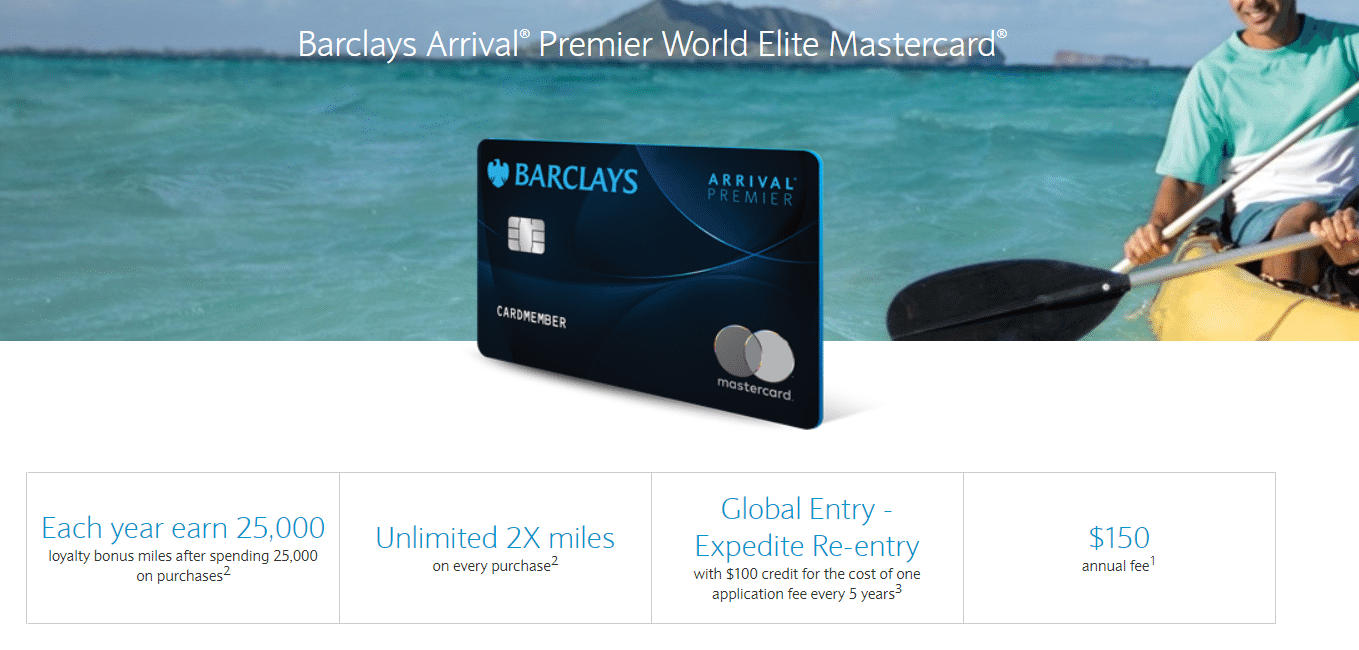

- No sign up bonus

- Card earns 2x miles per $1 spent

- Ability to transfer miles to Barclays travel partners

- $150 annual fee

- Annual spend bonuses:

- Spend $15,000 in a card membership year and get 15,000 bonus miles

- Spend an additional $10,000 and get an additional 10,000 bonus miles (total of $25,000 spend for 25,000 miles)

- Global Entry credit

- No foreign transaction fees

- Lounge Key access (basically just Priority Pass, but you have to pay for lounge access at $27 per entry)

- In early May existing Barclays Arrival/Arrival Plus cardholders will be able to convert to this product. Points earned on the Arrival/Arrival Plus do not carry over to this card

- Not currently available to existing Arrival/Arrival Plus cardholders: Unfortunately Arrival Premier is not available for instant approval at this time if you are an existing Arrival Plus or Arrival cardmember. Please check back in the next 30 days

Travel Partners

One of the most exciting things about this card in the lead up is the possibility to transfer the miles this card earns into other programs. The transfer partners are:

- Aeromexico

- Air France/KLM Flying Blue

- China Eastern

- Etihad

- EVA Air

- Japan Airlines (JAL)

- Jet Airways

- Malaysia Airlines

- Qantas

The transfer rate is 1.4 arrival miles = 1 miles with all of these programs apart from Japan Airlines. Japan Airlines requires 1.7 arrival miles per Japan airlines mile.

Other Redemptions Options

You can still redeem miles for 1¢ per point like you can with the Barclays Arrival/Arrival Plus products. This card does not carry the 5% rebate the Arrival Plus does.

Our Verdict

Overall it’s hard to see this for anything other than a massive disappointment. The nail in the coffin for me is the transfer rates aren’t 1:1. Keep in mind this card doesn’t come with a sign up bonus and also comes with a $150 annual fee.

At best you’re earning 3x miles per $1 and you have to spend exactly $15,000 or $25,000 for this to be the case. Let’s assume you spend $25,000 and earn 75,000 points, that’s either worth $750 or 53,571 miles. You’re basically earning 2.142 miles per $1 spent, best case scenario. You then still have to also pay a $150 annual fee and the annual fee isn’t offset by anything (e.g the card doesn’t really have any useful benefits). Worst case scenario you’re earning 1.42 miles per $1 spent and then paying $150 for the privilege. Actually if you want to transfer to JAL then it’s even worse as you’re earning 1.175 miles per $1 spent.

Keep in mind Chase offers the Chase Freedom Unlimited and this earns 1.5x points per $1 spent with no annual fee, the points are transferable as long as you have the Chase Sapphire Preferred, Reserve or Chase Ink Preferred. Even more damning is the American Express Blue Plus, that card earns 2x points per $1 spent with no annual fee and the points are transferable out of the box. Those cards also usually come with a sign up bonus of $150/$200. All of this is forgetting that the Barclays transfer partners are incredibly weak, they haven’t even partnered with any brands they offer co-branded credit cards with.

From a purely marketing perspective this card is simply to hard to understand for most people. You earn 2x miles per $1 spent, then those miles need to be transferred at uneven rates of 1.4 or 1.7 and then sometimes you get bonus miles for meeting spend requirements. Part of the reason the Chase Sapphire Reserve was so successful was that understanding the value was so easy.

I feel like a parent that has found out their child is doing drugs. I’m not angry Barclays, I’m just so very disappointed in you.

P.S. If you like our unbiased reporting on this and other cards, please considering retweeting this out or sharing it out elsewhere.