Update 8/18/25: Numerous reports indicate Chase is now being pretty strict with approvals even beyond 48 months. Possibly limiting customers to one lifetime bonus on Sapphire Preferred or Reserved combined. It’s still possible the ‘lifetime’ restriction will go away after a certain number of years and it’s possible that some people will still get approved in less than 48 months. Again, it never hurts to apply and you’ll see a pop-up if you are not eligible for the bonus. You can then decide to apply for the card without a bonus, if you’d like. But I wouldn’t necessarily downgrade after 48 months with intent to apply again since it’s far from certain you’ll get the bonus offer anyway. Note, you are eligible to get the bonus on the Sapphire Reserve for Business card, even if you’ve previously gotten the signup bonus on any other personal or business Chase card as it’s a different product line.

Update 6/23/25: I just want to reiterate that the new rules are not only negative, but might also have a positive outcome of being able to get another Sapphire bonus in less than 48 months. Reader Ashly reports getting approved in under 24 months from her prior Sapphire bonus without any popup issues. (After this update posted, many others in the comments also concurred with data points of receiving the Sapphire bonus in less than 48 months.)

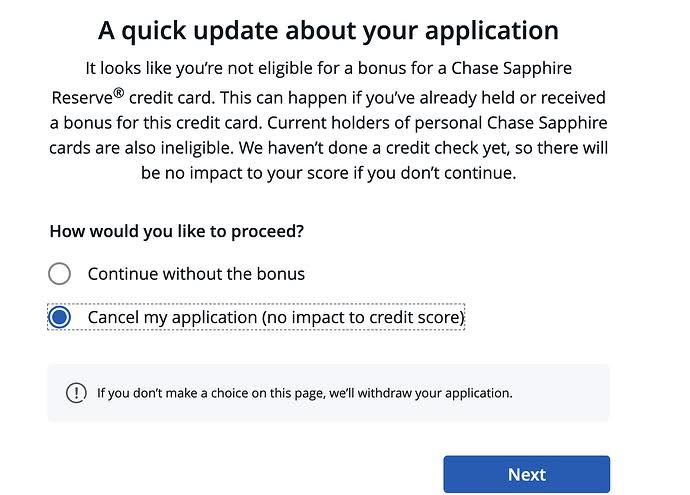

Update 6/23/25: This is what the pop up looks like.

Original Post 6/17/25:

Chase has said to various media outlets that the are doing away with the 48 month signup bonus eligibility restriction in favor of a proprietary determination by the bank of signup bonus eligibility.

Theoretically someone might be deemed by Chase to be eligible in less than 48 months. Practically Chase seems to be getting stricter and might deem someone ineligible even beyond 48 months. It will all depend on how profitable Chase deems you or whatever other factors they consider.

Chase will introduce a notice during the application flow which will let you know if you are not eligible for the bonus and give you the choice to continue or cancel the application. This makes sense: since the bonus determination is variable based on your customer history, they’ll let you know during the application if you are eligible for the bonus.

We are transitioning away from the family of cards every 48 month eligibility to a same product premium eligibility. The timeframe will be longer than 48 months but we aren’t able to share additional details.

American Express has long had this system whereby they’ll let you know during the application flow if you are eligible for a bonus. It’s often referred to as ‘AmEx pop up jail’ whereby someone attempts to apply for a card and gets a ‘pop up’ notice from Amex informing them they are eligible for the bonus.

I’m not sure exactly how the notice will display with Chase, but we might as well call this new Chase bonus denial, ‘Chase pop up jail’.

These changes will go in effect on June 23, 2025.

For now I’m only seeing this new change for the Sapphire Reserve and Preferred cards. It’s possible that all other cards, for the time being, will not have this new notification system and will run with all of the rules that we’ve seen until now.

New account bonus offer eligibility for either card will be based on factors including previously earned bonus offers and the number of cards opened and closed, among others.

Consumers applying through most channels will be notified during the application process if they are not eligible for a bonus offer and given the choice to continue the application or cancel the application with no impact to their credit score.

Over time, it’s possible that this pop-up method will eventually replace the whole 5/24 rule, as Chase will decide with each application whether to allow a bonus or not. For now, we haven’t heard any mention of changes to 5/24.