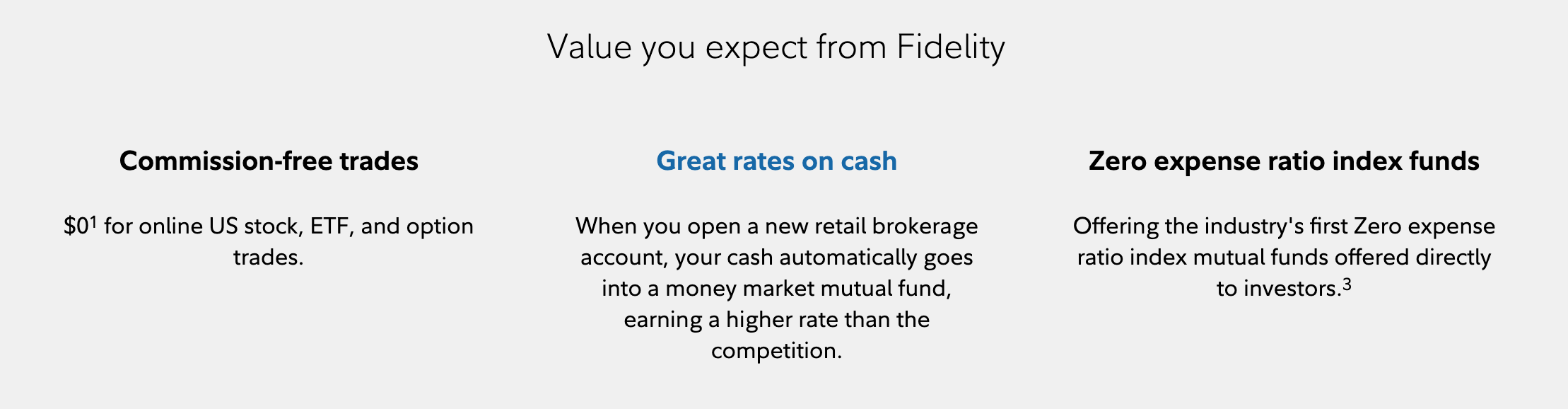

Fidelity brokerage has announced that it will be removing commission on all online US listed Stocks, ETFs & Options. Options contracts will still be charged at $0.65 per contract (which is similar to what most other brokerage charge). This announcement follows on the heels of similar moves made by Charles Schwab, TD Ameritrade, E*Trade, and Ally Bank.

Fidelity also recently added an option to automatically sweep any cash funds in your brokerage account into a competitively yielding money market fund. That makes them almost as good as the new Robinhood option which sweeps funds into an FDIC high yield savings account. I’m considering switching from Merrill Edge to either Robinhood or Fidelity for this sweep advantage.