Update 4: Rapid Travel Chai confirms that as of May, 2015 it’s still possible to product change to the BBR. Just keep trying till you get a CSR that can actually help you.

Update 3: Oren’s Money Saver confirms this is still working. If you get a rep that says they can’t process the downgrade, hang up and call again!

Update 2: Matthew in the comments was able to convert again, so it looks like this is back on. I’d recommend hanging up and calling again if they say it isn’t possible.

Update: It looks like Bank of America has stopped you from converting existing cards to the Better Balance Rewards card, it’s now only possible to sign up for this card directly.

I’ve been putting together a list of the best downgrade options for each card issuer (post coming soon) and then I read this post by Rapid Travel Chai which alerted me to an easy way to make another $100-$120 per useless Bank of America card.

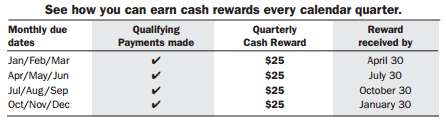

Bank of America has a credit card called BankAmericard Better Balance Rewards which doesn’t come with a sign up bonus and doesn’t earn at a high rate in any categories. It does come with an interesting benefit though, for every quarter where you pay more than the monthly minimum each month you’ll receive a $25 bonus. If you hold a Bank of America checking account, you’ll get an additional $5 per quarter which gives us a total of $120 per year.

Obviously this isn’t a lot and I wouldn’t recommend applying for this card directly, but Bank of America does let you do a downgrade/product change to this card from an existing card. There is no hard pull to do this product change and the card will keep the same opening date which will help increase your average age of accounts and thus your FICO score.

Sometimes the international phone operators will have trouble understanding your request. If this fails, say something along the lines of “I’d like to do a product change on <cardname you want to switch from> to the BankAmericard Better Balance Rewards” card.

To get the most value out of this card, you’re going to want to automate this promotion as much as possible. Here is what I’d recommend doing, find a small monthly charge that you don’t receive a category bonus on. Put this charge on your new BankAmericard Better Balance Rewards and then set it up so this card is automatically paid in full each month. [See also, PSA: Put a $5 Charge on that Better Balance Rewards Card]

You don’t qualify for the bonus if you have a positive balance on your card. Because the bonus posts directly to your credit card, you’ll have a positive balance some months. If you have a checking account with Bank of America, this is easily fixed you can opt in to receive the bonus as a direct deposit instead. This is by far the easiest option and remember you’ll earn an additional $5/quarter for having a checking account with them. If you don’t have a checking account, consider opening one or remember to make additional purchases on your card in months where you receive the cash reward.

If you’re the type of person who likes fine print, you can view all of the program details by clicking here.

Checking Promotions

Once a year BofA seems to offer a $100 bonus for opening a checking account. It might be worth waiting to open an account until one of these promotions comes around. Here is the promotion for earlier in the year (note: this is actually valid again, but not open to everybody). There is no hard pull done when you open the checking account, but they will do a ChexSystems inquiry.

You also get free access to a bunch of museums nationwide when you’re a BofA checking customer.

Negatives

It’s not all roses though. Because you need to have a statement generate each month to earn your $25/$30 the chances are Bank of America will report a balance. When it comes to FICO scores, it’s best to have a reported balance on one or two credit cards and no balance on the remaining cards.

You can try calling Bank of America and asking what date they report your credit utilization to the credit bureaus, then make sure your card has a balance of zero on that date (it should always remain the same).

For example, you call Bank of America and they state they report your balances on the 11th each month. Your statement generates on the 15th of each month. You’d want to set your recurring charge on the 12th-14th, and then you’d need to make sure your statement is paid off by the 10th each month. That way Bank of America would still report a utilization of $0 and you’d still earn your $25/$30 quarterly.

It’s also worth remembering that this plays a small role when it comes to your FICO score, personally I’m not going to go to this much trouble. If I plan to make a large loan (e.g mortgage or auto) I’ll simply not bother with this card for a couple of months to ensure my FICO score is the highest it can be. It’s a lot more important to ensure that your overall credit utilization is under 30% as that’s when you see the most negative impact (anecdotal you want it in between 1-10% depending on your credit profile with one or two cards reporting a balance).

Final Thoughts

If you have any Bank of America credit cards sitting in your sock drawer doing nothing, I’d definitely recommend doing a product change to this card instead. You might as well grab a checking account as well, it’s much easier than remembering to put additional charges on the card in certain months plus you might be able to grab a $100 checking bonus and you also get free access to some museums as well.