[Update 6/26/19: They sent out an email with details of the change from 2.20% to 2.10%. Points for transparency.]

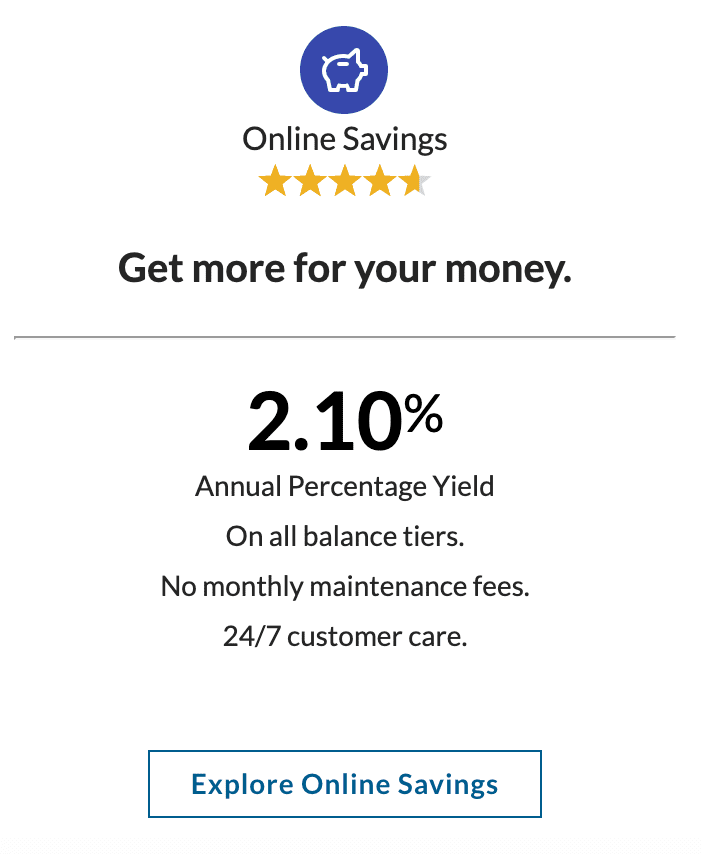

A lot of us use Ally Bank as a high-yield interest account. They just lowered the rate from 2.20% APY to 2.10% APY.

Back in January, they increased the rate from 2.00% to 2.20% as they saw people leaving them after getting their Payback Bonus offer; now, they’ve put it down to 2.10%. It’s getting more compelling to switch over to one of the 2.50% options. Or you can move the funds to the Ally no-penalty CD which remains at 2.30% APY, as before.

Update: a reader notes that existing Ally accountholders are still seeing 2.20% in their account. Unclear if it’s still maintaining that rate for existing users (for the time being) or it just hasn’t been updated yet.

Hat tip to reader Evelio204