We’ve known for quite some time not to meet an Amex minimum spend requirement by purchasing gift cards. Beyond the minimum spend, many people have no issues getting points on gift card purchases, though there are select merchants like Simon Mall gift cards which apparently don’t earn points.

At some point, Amex added in the terms on all cards (sample link) to clearly disallow signup bonuses from being earned with gift card purchases.

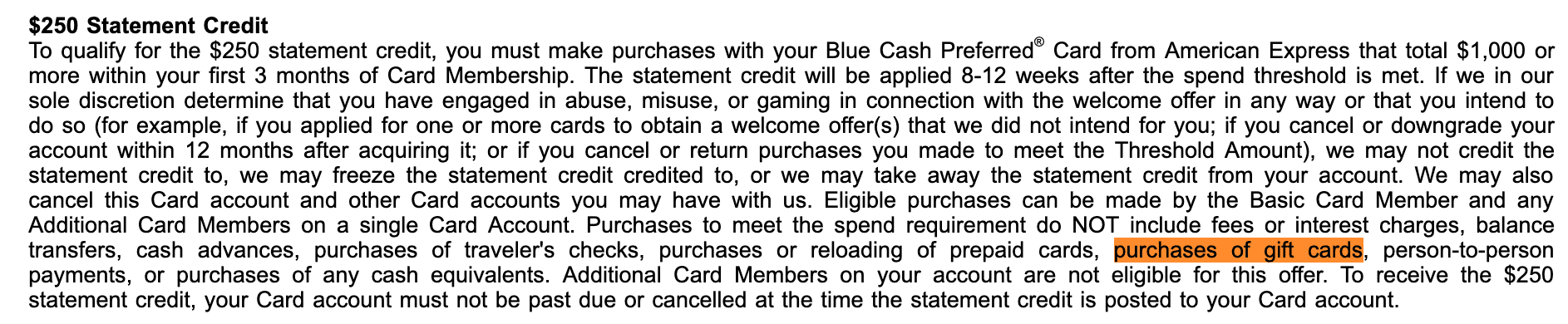

To qualify for the $250 statement credit, you must make purchases with your Blue Cash Preferred® Card from American Express that total $1,000 or more within your first 3 months of Card Membership…Purchases to meet the spend requirement do NOT include fees or interest charges, balance transfers, cash advances, purchases of traveler’s checks, purchases or reloading of prepaid cards, purchases of gift cards, person-to-person payments, or purchases of any cash equivalents. Additional Card Members on your account are not eligible for this offer. To receive the $250 statement credit, your Card account must not be past due or cancelled at the time the statement credit is posted to your Card account.

On various Amex cards, the gift card exclusion shows even for earning ordinary points. It’s not showing on all cards explicitly for ordinary points, but does on some; here are a couple of examples: Blue Business Plus card (link), Gold card (link) Blue Cash Everyday (link). All cards show the gift card exclusion for the bonuses, and many cards show it for ordinary purchases as well.

With your Blue Business® Plus Card from American Express, you earn one Membership Rewards® point for each dollar you spend on your Card for eligible purchases. For the first $50,000 in eligible purchases in each calendar year you also earn one additional point (for a total of 2 points)…Eligible purchases do NOT include fees or interest charges, balance transfers, purchases of travelers checks, purchases or reloading of prepaid cards, purchases of gift cards; person-to-person payments or purchases of other cash equivalents. Additional terms and restrictions apply.

Last we wrote about this was in March 2018 when Amex excluded reloadable prepaid cards and Amex gift cards from earning ordinary points. The pages quoted there still show the same terms with only Amex gift cards being excluded, but on the above-mentioned ‘important information’ pages, many cards show the exclusion for earning points on any sort of gift card, not limited to Amex gift cards.

In all likelihood, places like grocery stores will continue to earn points (unless you get manual reviewed in which case all bets are off), and specific locations like Simon Mall gift cards will continue to be excluded from earning points and rewards. But it’s worth knowing that the terms technically disallow all gift cards from earning points.

The terms would imply that even third party gift cards, such as Amazon gift cards, won’t earn points. Again, I have no doubt that regular, small gift card purchases from Amazon or most retailers will continue to earn points as before. On Prime Day, I bought a few small gift cards on Amazon, and it’s showing as pending rewards in my Membership Rewards account. Larger amounts or easily-detectible amounts, such as $500, do have some risk of Amex not awarding points if they decide to crack down on this, or they can potentially claw back points.

Hat tip to reader R.O.

[Post has been updated to reflect that these terms may have already been around on some cards for a while.]