Hilton HHonors Diamond Card

American Express are considering a new card to their Hilton line up, called the Hilton HHonors Diamond Card. The idea is to better compete with the Ritz-Carlton offering from Chase. Here is what the details of the card would be:

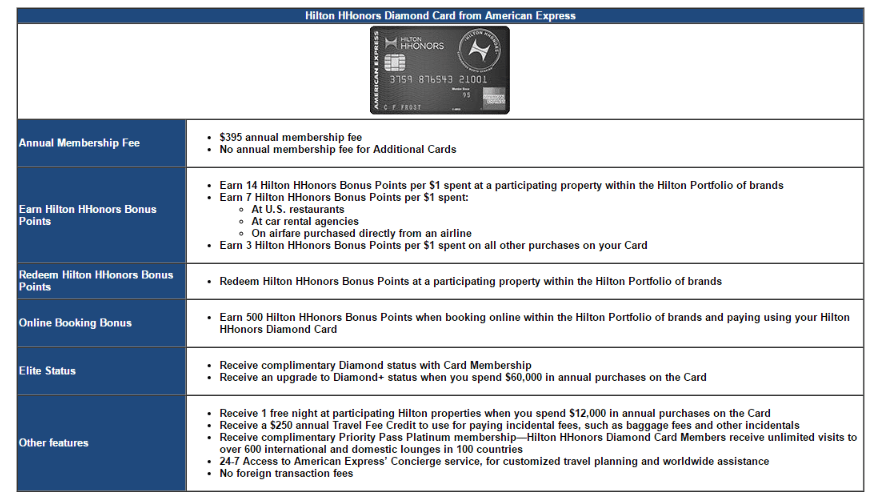

It’s also interesting that it says this card would come with Diamond status and the ability to earn Diamond+ status (something that currently doesn’t exist as far as I know?).

No Annual Fee Card

They are also considering some changes to this card:

- 5x points on all purchases at U.S restaurants, supermarkets and gas stations (increased to 7x)

- $25 Hilton gift card with every $2,500 spent

- 50% certificate for meeting specific spend thresholds ($10,000 or $12,000)

Surpass Card

- Add priority pass basic membership

- Add priority pass basic membership + 10 free visits

- Add a travel credit of $75 or $100

- Change earning categories to higher levels

- Other random changes

Our Verdict

This information comes from a survey a reader took, obviously there is no guarantee that any of these changes will come to fruition but it’s somewhat strange they were presented with a fully thought out card in the Hilton Diamond card. It’s also weird to see mention of Diamond+ status. Obviously not all of the changes would be made to the Surpass and no annual fee card.

Hopefully American Express does launch a new Hilton card, as that means everybody would be eligible to get the card again as American Express limit you to one bonus per lifetime. What sort of sign up bonus would this card need to entice you? Would you consider keeping it long term? Let us know in the comments.

Thanks to reader Jordan C for sending through this information