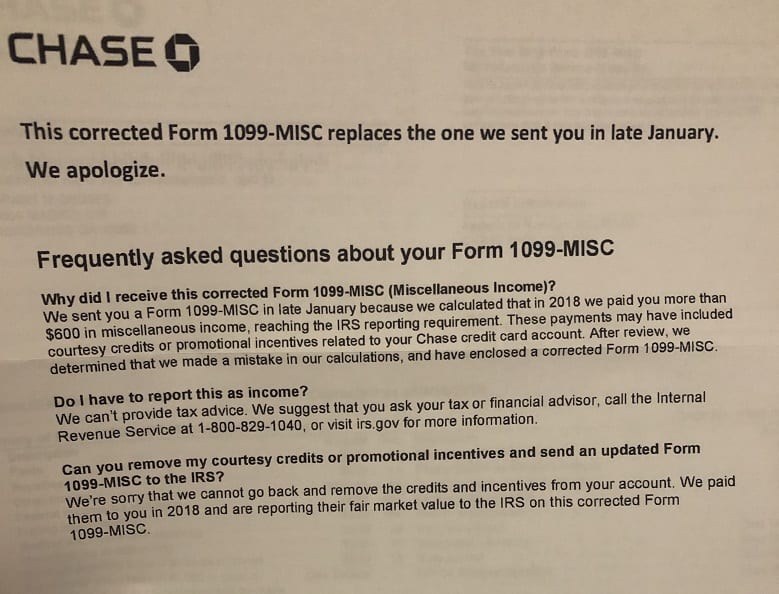

Chase has sent out corrected 1099 forms to people who received an incorrect form in January. The updated form also comes with a short apology (“we apologize”) and F.A.Q’s. It looks as follows:

Chase had to send out this correct as some things were incorrectly valued, for example a paperless statement bonus of 500 points was valued at $500 when it should have been valued at $5. It’s unclear if other things such as upgraded bonuses have been ‘corrected’ as normally we’d expect them to be treated the same way as a traditional sign up bonus is. We did contact Chase to get clarity regarding that point and we have not received any response despite repeated attempts.

It’s also not clear what will happen to people who receive a form only because the incorrect $500 value put them over the $600 threshold, although even if you’re under than threshold you’re still required to pay tax on that income but Chase isn’t required to send out a form. It would have been nice to see Chase extended a courtesy credit given the hassle involved, or at least an apology that was more than two words.

Hat tip to reader Grant G