Update 9/4/22: They’ve increased the interest rate from 2.09/3.09/4.09% to 3/4/5%, updated below (ht Eric)

Update 1/9/22: MyPoints has a signup offer on this account for 6,000 points (around $39). Hat tip to reader Kory

Update 5/6/20: This page has been fully refreshed and should now provide accurate information.

Offer at a glance

- Interest Rate: up to 5.00%

- Minimum Balance: None

- Maximum Balance: up to $10,000

- Availability: Anybody can join, even if they don’t live in Illinois but you’ll need to pay $5 to join Consumers Cooperative Association. More information here.

- Direct deposit required: Optional

- Additional requirements: Yes, see below

- Hard/soft pull: Hard pull (Equifax)

- Credit card funding: Yes, up to $200

- Monthly fees: None

- Early Account Termination Fee: None

- Insured: NCUA (68588)

Contents

The Offer

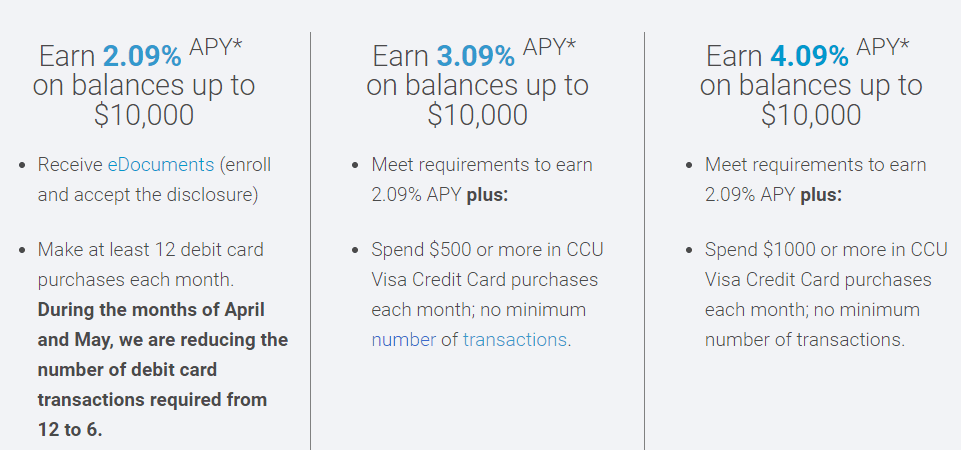

- Receive an APY of up to 5.00% on balances up to $10,000 with consumers credit union. This is a rewards checking account, as such you need to complete certain requirements to get the increased interest rate. Below are the requirements you need to meet and what APY you’ll receive if you meet them. All of these requirements are based on a calendar month.

- 3.00% APY on balances up to $10,000 and ATM refunds.

- Complete 12 debit/check card point-of-sale purchases without a PIN

- Receive $500 or more in direct deposits, mobile check deposits or ACH credits

- Receive eDocuments (enroll and accept the disclosure)

- 4.00% APY on balances up to $10,000 and ATM refunds

- Complete all of the 2.09% requirements and

- Spend a minimum of $500 on CCU Visa credit card purchases

- 5.00% APY on balances up to $10,000 and ATM refunds

- Complete all of the 3.09% requirements and

- Spend a minimum of $1,000 on CCU Visa credit card purchases

- 3.00% APY on balances up to $10,000 and ATM refunds.

If you don’t meet these requirements then you will only receive an APY of 0.01%. None of these rates have a guaranteed rate, so they can change at any time. Check out the rate history to get an idea of what they’ve been in the past.

The Fine Print

- Credit card transactions that post by the 2nd day prior to end of calendar month will count towards the total.

- All transactions received after end of month cut-off will be counted towards the following months qualifications.

Sign Up Bonus/Referral

Update: The referral bonus expired on September 30th, 2015 if you’re able to get it again please let me know and I’ll update the post.

Unlike other rewards checking accounts, consumers credit union also offers a referral program. For every person you refer you’ll receive a $50 bonus and so will they when they meet the rewards checking requirements at any level for the first two full months.

You need to fill out a paper form and then send it/fax it in, so this might be too much of a hassle for some folks, 847-566-7005 should be the correct fax number. You should also be able to e-mail it in, which is probably preferable as they will acknowledge when they have received it. This form is filled out after you sign up.

Referring friends & family members at the same address is not an issue. If you have any experience with this referral program then please let us know in the comments section below. You can find more information about this referral/sign up bonus here. The reports from this FatWallet thread are mostly positive for the referral program.

Avoiding Fees

There is no monthly fee, even if you do not complete the requirements to earn the higher interest rates (although if this is the case you’d only earn 0.01% interest). I couldn’t find any mention of early account termination fee in their fee schedule either.

Consumers Credit Union Credit Cards

Because there is a requirement to spend $1,000 per month to get the top rate of 4.59%, I thought I’d be a good idea to have a quick look at the credit cards CCU offers.

- Platinum card. No annual fee or rewards program, card doubles the manufacturers warranty on all purchases.

- Platinum rewards card. No annual fee and earn 1 point per dollar spent

- Student Visa. No annual fee or rewards program. Available for applicants aged 13 to 21.

Visa Signature Rewards Card, 3% Cash Back On Grocery Store Purchases

- Card earns at the following rate:

- 3% cash rebate for “Grocery/Convenience Store” purchases

- 2% cash rebate for “gas” purchases

- 1% cash rebate on all other purchases

- Cash rebate is automatically credit to account each month

- Maximum of $6,000 spend ($180 cash back annually, previously this was $6,000)

- No annual fee

- No fee on balance transfers

- 0% introductory APR for six months on all purchases and balance transfers

Our Verdict

I personally think this account only makes sense if you plan to go after the 4.09% rate and even then it only really makes sense if you’re making a lot of grocery store purchases every month and even then only if you put $6,000 on this card and then move the other $6,000 into non bonused spend and even then you’d need to be maxing out the other cards that earn at a higher rate on grocery store purchases.. For people that don’t fall into those categories, I think you’d most likely be better off with one of the other banks that offers a high interest account, although those are getting rarer. It’s also worth remember that CCU often changes what the requirements are to get the highest rate, so there is nothing stopping them making it much more difficult in the future.

As always, you can view more rewards checking accounts here or read our introduction to them here.

Post history/rate history:

- Update 4/15/20: Rates are being decreased by 1% for each tier starting May 1st, 2020. They have also removed the $100 monthly spend required for tier C (lowest rate) and mobile check (remote) deposits now count towards the minimum $500 monthly deposit requirement for tier C. I’ll give this page a full refresh on May 1st to make all of the requirements and tiers clearer.

- This account also has some new requirements, more information here.

- Update 4/8/20: This account is also showing on Swagbucks currently with a $50 bonus. Hat tip to reader Kyle

- Update 1/4/2020: Inactivity fee now added: $5/month after 2 years of inactivity.

- Update 12/10/19: There’s also a $37.50 signup bonus if you go through Swagbucks to signup for this account and meet a debit card requirement. (ht chasingurpoints)

- Update 11/20/19: Top rate is back to 5.09%. Hat tip to Dayn_Perrys_Vape

- Updated info here: Consumers Credit Union Rewards Checking Account Changes (Maximum Balance Decreased, APY Increased)

- August, 2007 – ??: 6.01% on up to $25,000

- Pre October 30th: 3.09%

- October 30th, 2010 – July 1st, 2012: 4.09% APY (maximum of $10,000 balance at this rate)

- July 1st, 2012: Rate dropped to 3.09% APY

- February, 2016: Top rate dropped to 4.59% from 5.09%

Dang even with the bump to 5%, the $1000 spend/mo requirement is way too high, when various credit cards can get you much more cashback. ETFCU’s 3.3% on balances up to $20k requiring only 15 debit card purchases/month ($0.15 per month with a PayPal subscription to yourself or with venmo/PayPal transactions) is still the better deal imo

To me, the CCU checking account at 3% is still worth it on its own, forget the CC.

On the other hand the CCU CC is one of the very few CC’s I kinda regret getting; it was sort of a waste of a slot.

But as long as I have it, at 3% CB for grocery, including Walmart, it’s still my card-of-last-resort for those (though less so for grocery since I PC’d an old TY card to the Citi Custom Cash).

And they do run deals several times a year for an extra $25 statement credit for spending $500 on this or that (holiday spending, online purchases, etc.) or extra $ for setting up recurring payments (phone, cable, etc.). Those deals are good enough on their own to exploit, and In those cases, it’s kinda nice to be able to also goose the checking interest rate as a side effect, as long as I’m already doing the spending.

So I make the best of it, but I wouldn’t really recommend getting the CC.

The checking account, however, is a winner.

Chris.

you can buy 2 VGC in grocery stores for the 1K spend and get 30.00 back (3%) But only for 6 months as the 3% is limited to 6k. I closed this acct a few years ago. then only 10.00 back for the next 6 months at 1%. This will cover the VGC fees but you need a way to liquidate these cards. Might still be worth the hassle for 10k Arielle Bianchimano%

Arielle Bianchimano%

This account is 3%/4%/5% now.

I haven’t used this account for several months. I just looked at the qualification email that I received for June. It shows that I qualified for the 2.09% rate even though I only met 1 of the requirements. Are any of you in the same boat as me? I’m just wondering if this is a glitch or if they are still waiving the requirements.

You qualified for the 2.09%APY* (Annual Percentage Yield) and ATM fee refunds on your free Rewards Checking Account last month.

We look forward to rewarding you again the next cycle you qualify. Remember, if you don’t qualify, you still earn the base dividend rate.

Below is a summary of the monthly qualifications and your actual results:

Monthly Qualifications

Actual Results

12 or more debit card transactions

Not Met

Direct Deposit/Mobile/ACH Credit of $500 or more

Not Met

Enrolled in eDocuments

Met

Required to receive 3.09% APY*: Complete at least $500 in CCU Visa credit card purchases.**

Not Met

Required to receive 4.09% APY*: Complete at least $1,000 in CCU Visa credit card purchases.**

Not Met

Several posts refer to a $500 DD requirement. Maybe there used to be a DD requirement, but as of 1/26/2022, the requirements to earn 2.09% APY are

(1) Receive eDocuments (enroll and accept the disclosure)

(2) Make at least 12 debit card purchases each month.

(3) Direct deposits OR Mobile Check Deposits OR ACH Credits totaling $500 or more monthly.

As you can see, DDs are OPTIONAL !!!

Furthermore, the requirements to earn 3.09% APY and 4.09% APY do not include receiving DDs.

Here’s the link: https://www.myconsumers.org/bank/accounts/free-rewards-checking

I’m considering this, but not sure if I’m going to go for it. In case this helps others out, here’s how I figured I could potentially qualify for the 4% interest:

Debit card

Eating out 4-8x/month

Gas 4x/month

Small shopping trips (or doing separate transactions as needed) 2-4/month

Credit card for regular household bills and groceries

$800+ for groceries (family of 4)

Cell ($52), internet ($50), electric ($60), gas ($30), insurance ($55)

Still not sure if it’s a wash with missing out on cashback from my other cards. If you’re single and on a tight budget, I can see how this wouldn’t work, but for families you might be able to swing it.

Em….”$800+ for groceries (family of 4)

Cell ($52), internet ($50), electric ($60), gas ($30), insurance ($55)”cando much better with the usbank cash+

Has anyone who is an existing member tried to open a checking account for the MP or SB bonus? If so, what reports got pulled? I am assuming they would do a Chex pull but no hard pull (this being required only for membership), but I am reluctant to give it a try without a DP.

I misplaced my dictionary of abbreviations and acronyms. What are the “MP” and “SB” bonuses? Member of parliament? Santa Barbara?

I miss the good ‘ol days. You could get 5.09% with 3% cashback on groceries and making an extra 1% from paying your bill with PPDG.

Without discussing age I remember back in 1978 you could get 5.5% on just your checking account and 11% on a CD-without doing anything but watching the money roll in.

To get 4.09% APY, you need to have their credit card and spend $1000 ore more each month. Too much.

Why can’t they make it simple. I’m getting 2% from 1st community credit union. Only have to do 25 debits/mo(25 swipes at a gas station at 3-4 cents each) and 1 automatic ACH($1). Maximum for the 2% is 25,000. Not sure if they’ll take out of footprint.

Trying to do some math here:

Max Annual Earn: 409+30 (3% earn on buying 2x$500VGC at S&S for 6 month) +10 (1% earn for the next 6 months)

Losses

1) $6VGC fee for 12 months x2 = -72

2) Loss of 3% in grocery points for the 2nd 6 months of the year = -30

3) 1% interest earned at other CU = -100

4) Time to deposit a check every month and do the 12 Amazon reloads.

Total loss: $202

Net Gain: 449 – 202 = $247 annual profit as compared to putting the money elsewhere.

Excludes time spent described in 4 above and the signup SB.

Funny thing, I just sat down on calculated to see if it is worth the extra $500 MS spend a month to get the 3.09% interest from 2.09% interest for each month (I opted for this, as the 3% cash back at supermarket is limited to 6K a year, so that’s $500 a month, alternatively you can do $1k/month for 6 months). I can qualify the 2.09% interest easily (which require DD and the debit spends only), so I don’t factor that in.

1) the 1% increase , would gain $100 in interest a year on the 10K if I charge $500/month. So divide that by 12 to keep things simple, that is roughly $8.33 additional interest a month

2) Buying a $494 VGC+$6 Fee would yield (3% of 500 spend is $15 cash back minus the $6 fee) , yields $9 profit

3) I have a 2.5% Cash back card that is my daily driver unless there are categories that is higher that I would set aside and spend the VGC card, so that is a loss of $12.38 ($494*2.5%) in cash back.

So the work on qualifying for the 2nd tier rewards would yield $4.95 profit each month (+8.39 in bank interest, +$15 Cash back on $500 spend, -$6 in VGC fee, -$12.38 in cash back opportunity on my regular card).

it’s an extra 5-10 mins to do a separate transaction as I’m already at the supermarket already, so that would be worth the $4.95 monthly profit ($59.40 a year). I wouldn’t go out of my way to do it. However, Q1 5% category on Chase Freedom cards is supermarket and I have 5 Freedoms, so I will prob focus on that first.

what card gives 2.5% on everyday spend? Thanks in advance.

I also left out the loss point of a hard pull which may be the main reason I would skip getting this CC.

USAA Limitless, no longer available

Qualifying for the 2.09% APY does not require a DD. According to CCU’s advertised requirements, the $500 monthly deposit requirement can be satisfied by direct deposits OR mobile check deposits OR ACH credits.

Here’s the link to CCU’s advertised requirements to earn top rates for Rewards Checking: https://www.myconsumers.org/bank/accounts/free-rewards-checking

CCU’s Visa Signature Rewards credit card and Visa Signature Cash Rebate credit card have no annual fee and pay 3% rewards on grocery purchases up to $6000/yr.

You don’t have to deposit any checks or make any direct deposits. According to the ADVERTISED requirements to earn 2.09& APY, you can satisfy the $500 monthly deposit requirement with ACH credits. Here’s the CCU link to CCU’s ADVERTISED requirements to earn the top yields with Rewards Checking:

https://www.myconsumers.org/bank/accounts/free-rewards-checking

You don’t have to do do any Amazon gift card reloads. Instead, link your CCU debit card and any one of your bank accounts to a CashApp account. Using CashApp, you can easily do 12 point-of-sale purchases (of any amount) with your CCU debit card; the purchases are debited from your CCU checking account as point-of-sale purchases. The debited amounts go into your CashApp balance, which you can easily transfer to your linked bank account. You don’t actually spend any money. You merely move money from your CCU checking account to your CashApp balance to your linked bank account.