Reposting this as we wrongly reported that the $500 in spend must be done on a non cash back credit card. Thanks to Freequent Flyer Book for providing the actual letter that proves this is wrong.

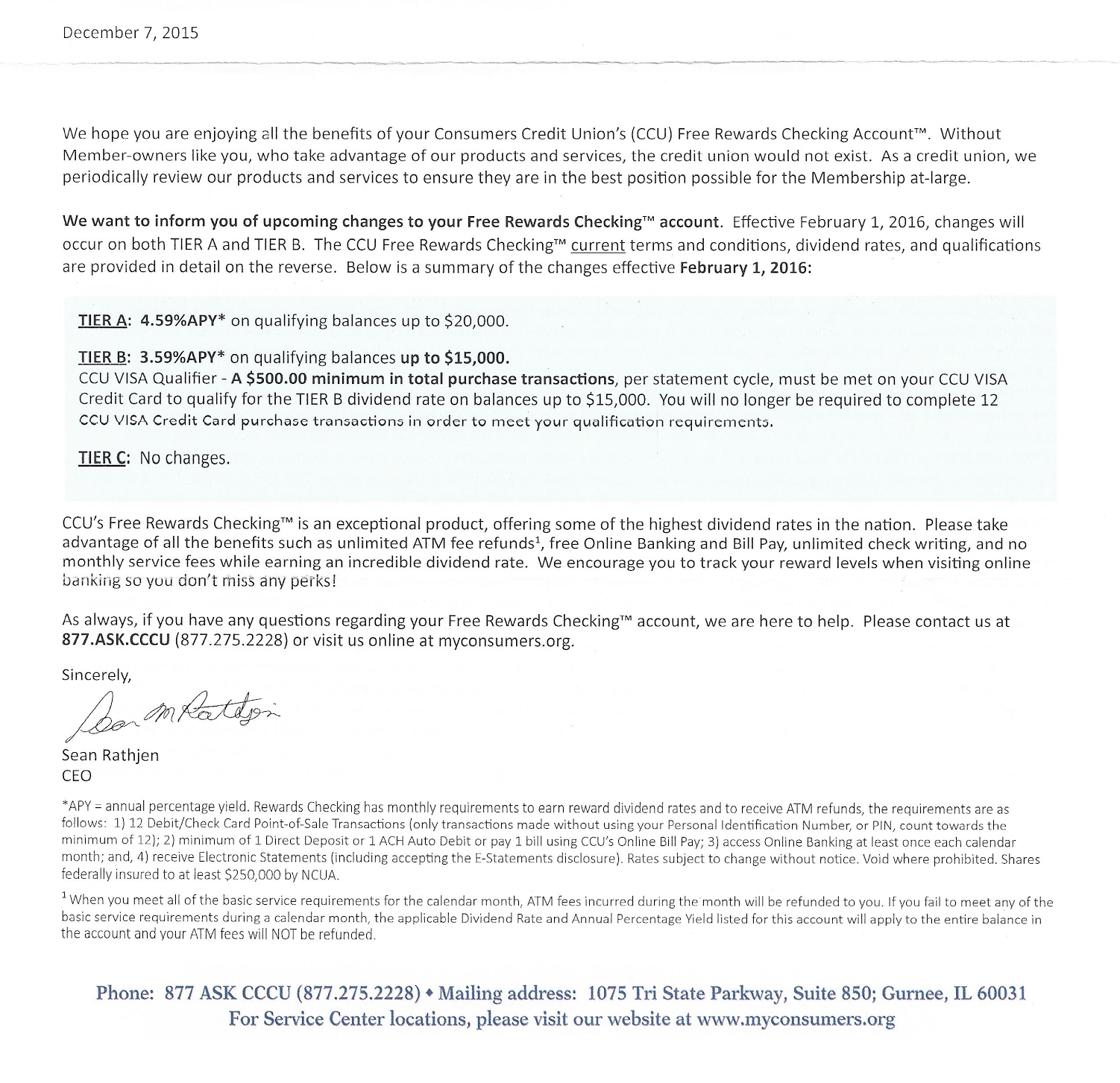

Consumers Credit Union offer one of the best rewards checking accounts, with their highest rate being 5.07% on balances up to $20,000. They have just let existing customers know that this rate will be dropping at the start of February, 2016. Below are the old rates followed by the new rates:

- No change: 3.09% APY on balances up to $10,000 and ATM refunds.

- Complete 12 debit/check card point-of-sale purchases without a PIN

- Complete one of the following every calendar month:

- One direct deposit OR

- One ACH debit OR

- Pay one bill using CCU online bill pay

- Access online banking at least once

- Receive eDocuments (enroll and accept the disclosure)

- Previously 4.09%, will be 3.59% APY on balances up to $20,000 (maximum balance being dropped to $15,000) and ATM refunds

- Complete all of the 3.09% requirements and

- Complete 12 CCU Visa credit card purchases, no minimum purchase requirement (new requirements will mean you need to spend $500 per month as well)

- Previously 5.09%, will be 4.59% APY on balances up to $20,000 and ATM refunds

- Complete all of the 3.09% requirements and

- Spend $1,000 or more in CCU Visa purchase transactions, regardless of the number of transactions (new requirements will mean you don’t need to meet this, but you still need to spend $500 for the 3.59% rate which is a requirement for this rate as well)

Basically the two higher tiers are having their rate dropped by 0.50% and the lowest tier is staying the same. In addition to this there is now a spending requirement of $500 for the second tier and you can only have $15,000 in that account instead of $20,000. Consumers credit union recently also announced that they were nerfing their 3% cash back card (on grocery & convenience stores). Previously you could earn up to $6,000 in cash back per year, starting January 1st this is being limited to $6,000 in spend (maximum cash back of $180).

This makes it much less appealing to go after the highest tier rate (currently 5.09% but will be dropped to 4.59%) as you’d only be able to earn 3% cash back for the first six months and then you’d be stuck earning 1% back (or 2% back on gas).

This might not be an issue though, as people are also saying that the spend requirement will need to be completed on a non-cash back Visa earning card. This would make the deal even worse as you’d be missing out on earning cash back on $6,000 (for the second highest tier) or $12,000 (for the highest tier). Although I’m not 100% sure if this is correct. Update: This is not correct, see the letter sent out above. Thanks to Freequent Flyer Book for providing this.

There are other options out there, although Consumers Credit Union could still be a great option for a lot of people. Most of them have smaller balance maximums (usually $5,000), but the requirements are easier to meet and don’t require any credit card spend. Here are some other options you could consider:

- Guide to 5% Interest Prepaid/Savings Accounts

- Mango 6% account, up to $5,000

- Lake Michigan Credit Union 3% account, up to $15,000

- Great Lakes Credit Union 3% account, up to $10,000

- Northpointe 5% account, up to $5,000

Hat tip to Frito_Pendejo_esq on /r/churning