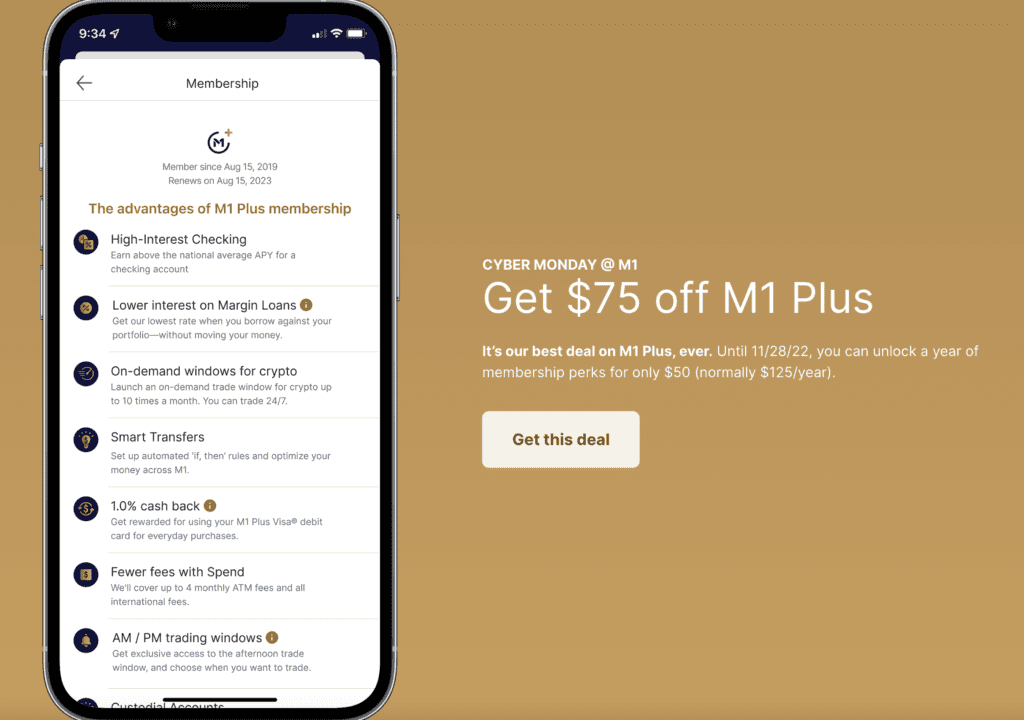

M1 Finance launched a sale today on their M1 Plus membership for just $50 instead of $125. The deal is available through 11/28/22 and works for existing members as well to get their renewal for just $50.

Having M1 Plus gets you access to special cashback rates on their debit card, more details on how that works can be found in this post. They are also slated to be launching in January a 4.50% APY savings account for M1 Plus members, but that’s not live yet.

If you are new to M1, you can get $10 by signing up with a referral link (thread to find a referral here), though honestly it’s not the biggest deal for new members since you can get 3 months of M1 Plus free.

Hat tip to readers Peek and Josef