Deal has expired, view more PayPal deals by clicking here.

Update 5/7/19: Deal is back for 2019. Hat tip to MtM

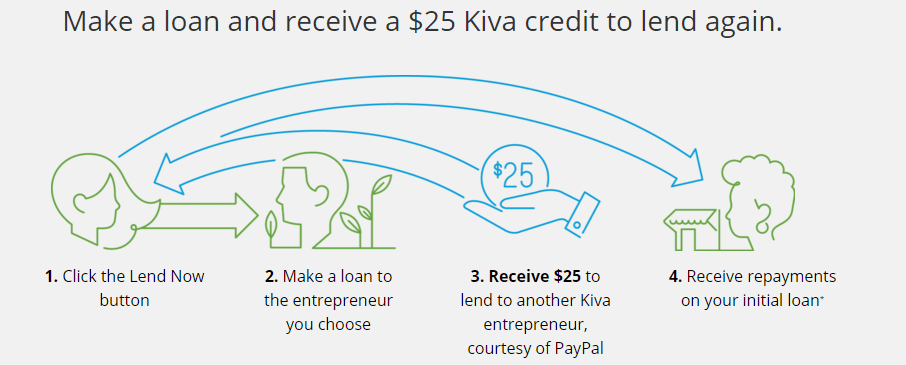

The Offer

- Loan someone $25 or more through the KIVA loan system with Paypal payment and Paypal will give you another $25 to loan out. Keep in mind repayments made on your loan made with the promotional Kiva credit will be returned to the Kiva PayPal Donor Advised Fund to be used in future lending campaigns.

The Fine Print

- “Qualification Period”: Starts at 12:01:00 a.m. Pacific Time (“PT”) on May 1, 2019 and ends the earlier of (2) 11:59:59 p.m. PT on May 11, 2019 or when the total Reward amount reaches five thousand (5,000) loans.

- “Redemption Period”: Starts at 12:01:00 a.m. Pacific Time on May 1, 2019 and ends at 11:59:59 p.m. PT June 15, 2019.

- “Reward”: A Kiva credit in the amount of USD $25.00 to make another loan using the Kiva.org platform during the Redemption Period to a qualified borrower registered with Kiva on Kiva’s platform and located outside the United States. Proceeds from the loan are not payable to Eligible Participants and are instead payable to the Kiva PayPal Donor Advised Fund. Rewards are not tax deductible. There is a limit of one (1) Reward per Eligible Participant.

Our Verdict

Some people like to manufacture credit card spend with Kiva. I have some issues with micro lending in general, but if you’re a fan of the program then this is effectively a way to double your “donation” via Kiva & PayPal.

Hat tip to reader Sergio R