A few days ago Wallaby Financial tagged me in a post on Twitter asking my thoughts on the Petal Card. I’d never heard of the card before so I thought I’d have a look and do a quick review. Petal advertises itself as a no fee credit card that is available to people without a credit score. They claim to look at the money you make and the bills you already pay to qualify you for the card.

Contents

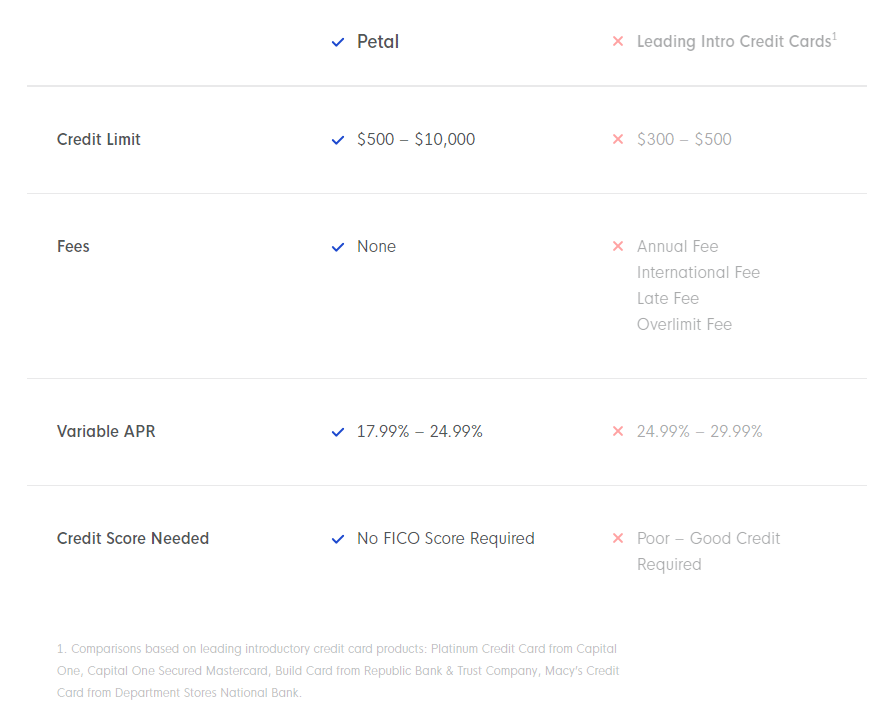

Card Basics

- No annual fee

- No rewards program

- No fees of any kind (e.g no late fees, foreign transaction fees etc)

- Variable APR of 17.99%-24.99%.

- Minimum interest charge of $0.50

- Credit limit of $500-$10,000

Our Verdict

Credit cards targeted towards people with bad credit are notorious for having a lot of fees, it’s something I’ve tried to educate people with bad credit on a lot. I like seeing new cards with no/low fees targeted towards this market segment. I can see some limited use for petal for people with poor/no credit history (but these starter cards might be better). The downside to this card is that there is no rewards program or sign up bonus. I think this is less of an issue for people with poor/no credit history but there are cards that do have a rewards program and no/low fees.

For example the Discover it Secured has a pretty good rewards program, the downside to this card is that it’s a secured card. This means you need to put down a security deposit that matches your credit limit (e.g if you want a credit limit of $1,000 you need to deposit $1,000 as a security). I can definitely see the case for somebody wanting to get the Petal card over the Discover it Secured card for that reason, just keep in mind that the Discover it Secured can unsecure (e.g security deposit no longer required) after a period of only 7 months.

There are other cards in the market trying to offer credit cards without using traditional scoring models as well, SelfScore is another player targeting international students. What are your thoughts on the Petal card? Let us know in the comments below.