U.S. Bank has just launched a new premium card, this time a co-branded card with Korean Air SKYPASS. Let’s take a look at the new card.

Contents

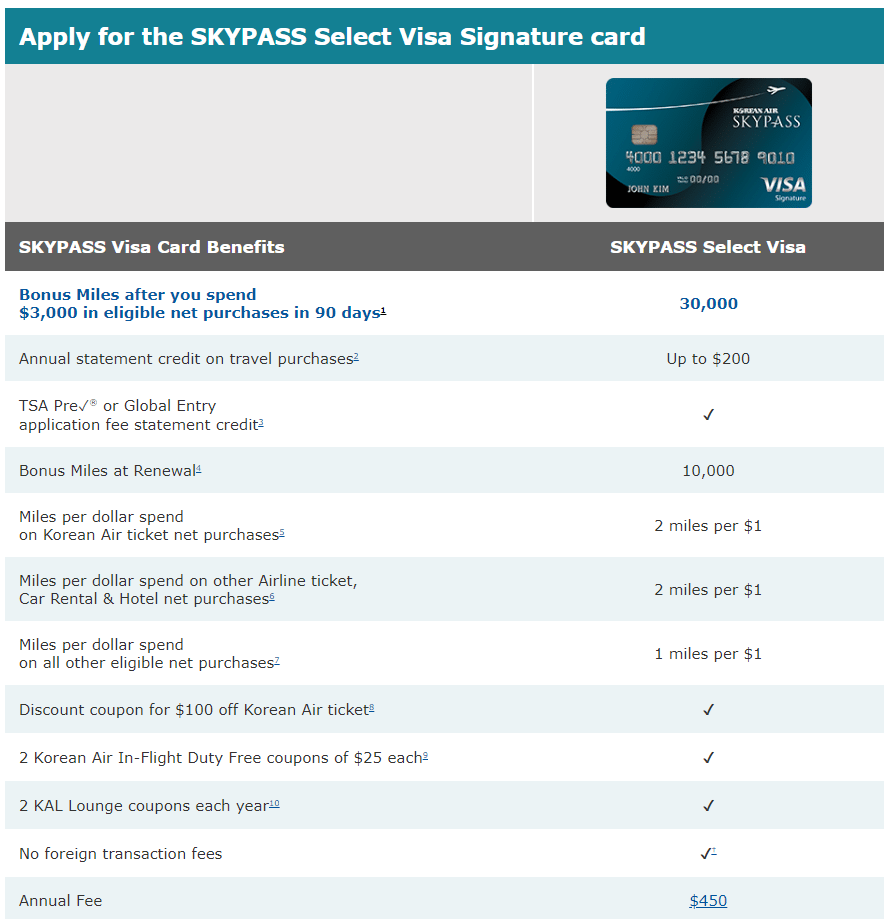

Card Basics

- Annual fee of $450, not waived fist year

- Sign up bonus of 30,000 miles after $3,000 in spend within the first 90 days of card opening

- $200 annual statement credit on travel purchases (this is based on a card member year, not calendar)

- TSA PreCheck/Global Entry Credit of up to $100

- 10,000 bonus miles on card anniversary, must spend $35,000 in the prior year

- Card earns at the following rates;

- 2x miles per $1 spent on Korean air purchases

- 2x miles per $1 spent on Airline ticket, Car Rental & Hotel purchases

- 1x mile per $1 spent on all other purchases

- Discount coupon for $100 off Korean Air ticket

- 2 Korean Air In-Flight Duty Free coupons of $25 each

- 2 KAL Lounge coupons each year

Our Verdict

In July last year they sent out a survey regarding this possible card, so it’s interesting to see it finally launch with a lot of the benefits they surveyed people on. Personally I think this card sucks, you’re paying an annual fee of $450 and the benefits are lackluster. Most people already have TSA PreCheck/Global Entry, the renewal miles required $35,000 in spend to receive, the earning rates suck and one time discounts on airfare and in-flight duty fee don’t make up for the fact that the card has no other redeeming benefits apart from the $200 travel credit that is based on a card member year. Maybe if the bonus was better I could see this being useful for some people but even on the existing U.S. Bank Korean cards we’ve seen better bonuses in the past. It seems like U.S. Bank are hoping to cash in on the success of the Altitude card, but without offering any similar benefits.

Hat tip to Chong786