Update January 7th, 2018: This card is now no longer accepting new applications. All pages on USAA now error out apart from the terms page. It’s unclear what will happen to existing customers.

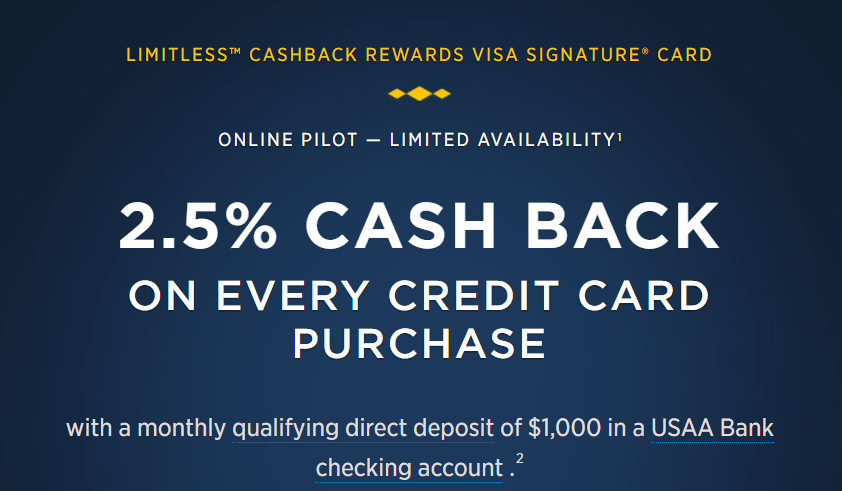

Original post November 17th, 2017: USAA offers the Limtless Cashback Rewards card that offers 2.5% cash back on all purchases when you have a monthly qualifying direct deposit of $1,000 in an USAA Bank checking account. The card has been in an online pilot since it was launched and only available in limited states. They were slowly adding more states until October 30th, 2017 when they removed some previously eligible states. They have now removed even more states and it’s only currently available in Louisiana. It seems like the rumors of it going nationwide have been squashed unless they are rolling back before a nationwide launch (and to me that doesn’t make much sense).

Some people have been warned about manufactured spending, so it’s possible they are trying to get a handle on that currently. Hopefully anybody that in a previously eligible state that wanted to sign up has already done so. You can read our full review of the card here. You can read our full review of this card here.

Hat tip to reader Connor