Lending Club (LC) is a person to person lending website that connects borrowers and lenders (which LC call ‘investors’) together to try and create a efficient market place for loans without the overheads and vast profits that banks command.

Today we’re going to look at how a borrower can find out their FICO score for free by using Lending Club. You’ll first need to sign up for an account and start the application process to become a borrower (don’t worry, we won’t be borrowing any money in this guide and it won’t affect your FICO/credit scores as we’ll only be doing a soft inquiry which doesn’t show up on a credit report).

When signing up to become a borrower they’ll do a soft inquiry to work out your credit score, this is used to find out what APR (Annual Percentage Rate) they will charge you. We can use this information to work backwards to find out your FICO score.

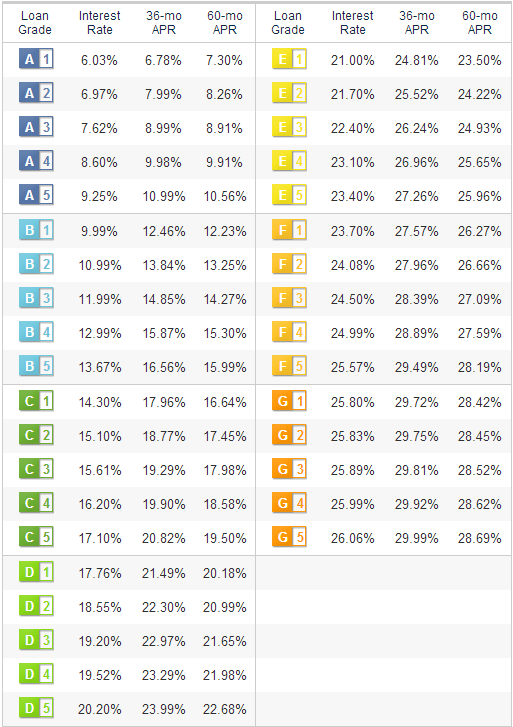

Once you’ve applied, you’ll receive a 36 month APR. Get this and match it up with the table below to find out your loan grade:

APR’s – Loan Grade’s – Lending Club

Once you’ve worked out your loan grade, look at the below table to find out your FICO score range:

FICO Score and Loan Grade : Table Two

The above table has since been removed from the Lending Club website, but we still believe there is a strong correlation between FICO scores and loan grades. You can always have a look at the other methods of getting a free FICO score if you want a more accurate idea.

Examples:

- You receive a 36-mo APR of 13.84% if we match this up in table one we’ll see a loan grade of B2. We can then look at table two and see that a loan grade of B2 will have a FICO score range of 700-706.

- You receive a 36-mo APR of 6.78%, looking at table one will show a loan grade of A1. This indicates a FICO score range of 770+ (or 770-850 as 850 is the maximum)

- You receive a 36-mo APR of 23.99%, table one shows us this is a loan grade of D5. When we look at table two we’ll notice that there is no FICO score range for D5, this means you have a FICO score under 660-663 and will need to increase your FICO score before you’ll be accepted for a loan with lending club (and most other lenders).

Lending Club uses information provided by the credit bureau TransUnion, so you’ll receive a TransUnion FICO score (also known as an Empirica score or TU FICO). We’re currently unsure if this is the TU FICO 98/04 or 08 score, but because it only offers a range it’s unlikely it matters.

If you’ve used Lending Club before, we’d like to hear your experiences – was it cheaper than the rates your bank was offering? Did the above method result in you getting an accurate reading on your FICO score?