I’m in the market for a new credit card (aren’t we always?), and I was looking into different cards with a high category-bonus, such as supermarket, gas, drugstore … the kind of stores we frequent. Another criterion is that the rewards should be in the form of cash-back, so that I can, you know, pay the grocery bill.

5% Time

I encountered three options to consider:

- TD Easy Rewards This card offers 5% cash-back on dining, groceries and gas. Additionally, payments of cable, phone and utility bills get 5% back. The 5% bonus is only for the first 6 months; 1% thereafter. It also has a signup bonus of $100. Previously, the signup bonus was $200, but that offer is no longer available. The current offer is available until Nov. 1, 2014.

- Wells Fargo Rewards This card offers 5% cash-back on gas, grocery and drugstore purchases for the first 6 months. No signup bonus.

- Old Amex Blue This is different from Amex Blue Cash Everyday & Amex Blue Cash Preferred. This one offers 5% cash-back at supermarkets and drugstores, on purchases in excess of $6500. The first $6500 will earn either 1% or .5%, depending what you purchase. No signup bonus. More details below.

One other option would be BBT Spectrum Rewards, but that card gives just 4.05% and only for three months, among other limitations. So that leaves me with these three options.

Let’s take a look at these cards, and then see if we can decide which one to go for.

TD Easy Rewards

TD has the most extensive 5% options; besides for groceries and gas, they also throw in cable, phone and utility bill payments, plus dining. On the other hand it does not offer 5% at drugstores – one of our favorite place to buy gift cards.

This card has a geographic limitation – it’s only available in the following states: Connecticut, Delaware, Florida, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Vermont, Virginia, Washington, D.C. (location search).

Another limitation is that it’s only available to TD customers, so you’d have to open an account with them to apply. You may be able to apply in-branch without opening any other account.

I wasn’t interested in another checking account, so I opened a CD and put $250 in it. In the application process it’s clear that any CD/savings account with them is enough. I haven’t yet applied for the credit card, but now I got that hurdle out of the way.

Old Amex Blue

This card is not publicly available anymore, but it still has a hidden signup link. For the link to work you need to open it incognito (link). This card offers 5% at supermarkets and the all-important drugstore category.

Note that the drugstore category only includes: CVS Pharmacy, DUANEreade, Rite Aid and Walgreens.

It also gives 5% on gas, but only on the first $400 of the gas purchase. This makes it a little less profitable to use at a gas station, if you want to purchase $500 gift cards. For me this isn’t significant, since I don’t know of any place to buy gift cards which is coded by Amex as a gas station (see this post), but this may matter for others.

The major advantage of Old Blue versus the other two options is that this isn’t limited to 6 months; it’s forever. Of course, “forever” just means until Amex decides to pull the card completely. I really don’t know what the standard is for phasing out old cards, so I’m not going to hazard a guess as to how long current cardholders will maintain the 5% benifit.

But I will guess that the hidden link we mentioned won’t be around for too long. This is another factor which is pushing me toward the Old Blue, since the other two options should be around for a while.

Wells Fargo Rewards

For someone who wants to rack up spend, this card is the best in terms of categories. It has supermarkets, drugstores and gas stations. There’s no $400 limit on gas stations, and it will work at all drugstores. Slightly better than Old Blue. Additionally, the gas category is on Visa’s terms, which is broader than Amex’s terms (think: 7-Eleven) – a very important distinction to me.

On the other hand, Old Blue has the “forever” factor, and TD has the $100 signup bonus advantage.

The Caution Threshold

In order to figure out which option is best, we first need to clarify how much spend we can put on these cards.

Of course, the most basic question is what kind of credit limit the card will come with. I have no data on which of these banks offer higher/lower credit limits.

But just as important is completely separate issue – the Caution Threshold. How cautious are you? Are you willing to rack up many thousands in category (“abusive”) spend? Are you willing to recycle your credit limit a few times?

These questions each person has to ask themselves in order to properly calculate how much they’ll be able to profit from these cards. Here’s my calculations for myself.

In terms of credit limits, my recent cards have yielded between $5000-$7500 credit lines. I’m going to figure the lower end, $5000, since I have a feeling that %5 cards will specifically start you with low credit lines so that you can’t do precisely what we’re trying to do here. On the other hand, the Old Blue isn’t a limited (6 month) offer, so I’m going to guess a $6600 credit line – what I got on my last Amex card.

Conversely, with regard to my Caution Factor, it’s precisely the opposite; I’d be extremely cautious with the Amex card, and not nearly as much with the TD or WF.

Why?

Simple. I have no relationship with TD or WF, but I do have other credit cards with Amex. Since I’m cautious by nature, I wouldn’t risk being shut-down by Amex in order to get all I could out of this card. But with TD and WF there’s much less at stake for me should I get on their bad side, so I’d be willing to use the card more “abusively”.

If it were literally free money, I’d probably be willing to risk much more with Amex. But 5% cash-back takes a reasonable amount of time and effort to cash-out, so I wouldn’t take the risks of recycling my credit lines or even maxing out my credit lines on gift cards.

To put out a number, I’m going to say that on TD or WF I’d spend $5k per month, and on Old Blue I’d spend $3000 per month (6 gift cards, in our language).

The Target Factor

[Update (11/10/14): it appears that TD codes Target not to earn 5%, despite the fact that it comes up in your TD login as “supermarkets”.]

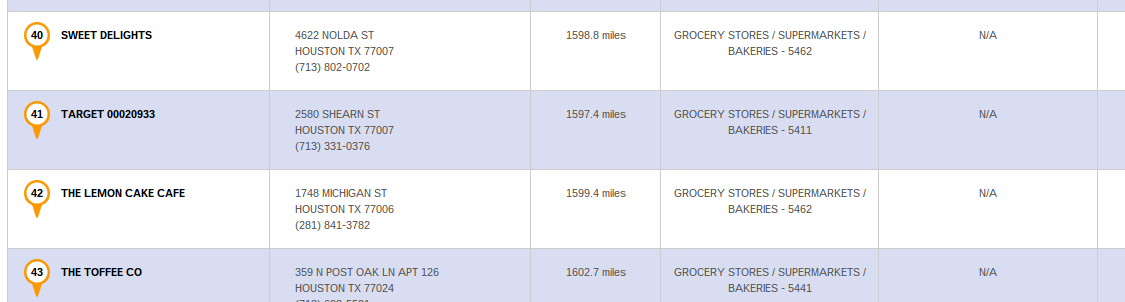

Another factor to consider is perhaps less-known: the Target Factor. Many Target stores are coded by Visa as supermarkets, and thus would earn 5% with the TD of WF cards – both are Visa branded cards. You can check your local Target using the Visa Supplier Locator.

Here’s a random Target store in Texas listed by Visa as a grocery store

Some Walmart’s are also coded as supermarkets, but the reason we’re interested in Target is because we like to load our Amex for Target (AFT) cards there. That’s an easy way of racking up $5000 in spend per month!

Different people experience different levels of difficulty with buying gift cards with a credit card and with unloading those gift cards, but for me Amex for Target is extremely easy to load and unload; I never experience any lines at Target or at the ATM, I have a surcharge-free ATM nearby, and both Target and the ATM are along my regular driving route.

Since my TD/WF spend threshold which I mentioned earlier was $5000, I could actually max out my $5000 spend by just using it at Target.

On the other hand, Amex does not consider Target to be a supermaket, so this trick wouldn’t work.

From my online Amex account. Target is called a “discount store” and “wholesale store”, not supermarket.

Now let’s approach the question of TD vs. WF.

TD Rewards Vs. Wells Fargo Rewards

Both cards have the same 5% for 6 months.

- TD has the edge of giving a $100 signup bonus.

- WF has the edge of allowing the all-important drugstore category.

WF has the drugstore category which helps in two ways: it gives a more diverse base to purchase gift cards, and you can often save a dollar or two by purchasing gift cards in the drugstore versus the supermarket. That may not seem like a lot, but consider the fact that my plan here is to buy 10 $500 per month for 6 months. If we’ll figure a conservative $10 savings per month by having the additional option of purchasing at drugstores, we’ll end up with a $60 savings over the 6 months. Now the edge to TD is just by $40 ($100-$60=$40). The added ease of having the drugstore option available may make it worthwhile.

But once we have the Target Factor mentioned above, this point becomes moot. If I’ll do most/all of my $5000 monthly spend at Target, I won’t need the drugstore option. Full $100 edge to TD.

Verdict: TD over Wells Fargo.

TD Vs. Old Blue

Okay, that was the easy part. Now… TD or Old Blue?

Let’s try to put a dollar-value on each card. How do we do that?

Well, with TD we’ve pretty much figured everything out already. If I spend $5k for 6 months, that’s $30k total spend, for a total cash-back of $1500. Since I have access to a surcharge-free ATM to unload AFT, my total cost is around 1% (Target load fees + AFT ATM fees), which means I lose 1/5 of the $1500. That leaves $1200. Add $100 signup bonus for a grand total of $1300.

But how do we evaluate the Old Blue? How many months do we count?

I’d like to calculate the value assuming two years of usage.

Why? Why not calculate ten or twenty years?

Firstly, we don’t know if Amex will stop this card completely. I’m sure they’ll stop the hidden signup link, but the question is how long they’ll allow current cardholders to continue with the card. Will they eventually transfer everyone over to their “new and improved product” Blue Cash Everyday? I simply have no data on what credit card issuers usually do and how long it takes them to do it, but I feel two years is a fair number to put out.

Additionally, I need to consider other factors: even if the card is still offering 5%, will I still be using it? What if sometime down the line I get busy with a job/project and have no time to rack up credit card spend (possible)? What if I move out of the USA (unlikely)? What if Tim Cook retires and they hire me as CEO of Apple (very unlikely).

The point is that it may not be around forever and I may not be using it forever. Thus, I think two years is a fair amount of time to give this card.

Now… the math.

The Math

Given the number mentioned above of $3,000 per month, we’d end up with $72k in spend over the next two years (3000 x 24 = 72,000). At 5% that would be $3600. But wait! We need to remember that the first $6500 per year only earn 1%. Without boring you with the math, the total cash-back over the two years ends up at $3080.

Now we need to deduct the costs associated with purchasing the gift cards. Earlier, for TD, I calculated 1%, based on what it costs me to use AFT. For Amex, I’m going to calculate a slightly higher expense-rate of 1.2%. Thus, my profit will be 3.8% of $59,000 and -.2% of $13,000.

Bottom line: $2216 profit.

[Note: the first $6500 could technically be spent anywhere. If you decide to do that, be careful for post #3382 on this Flyertalk thread. For simplicity’s sake, I made the calculations assuming that all spend is done in the bonus category, including the first $6500.]

So now we need to make a decision: TD with a profit of $1300 or Old Blue with a profit of $2216? The Old Blue includes considerably more effort, and I won’t see that money for longer. But it’s almost $1000 more. Which to do?

The Verdict

Ultimately, I’d have to hand it to Old Blue over TD, particularly because it’s a fleeting opportunity. TD may lose its $100 signup bonus come November 1, but the basic offer should still be around even after that.

But as I’m writing this post I realized that there’s no reason I can’t go for both: my main opposition to that is that I’m not sure I have the time/effort to spend and maximize two 5% cards concurrently. But once we hit on the Target Factor mentioned above, I consider the TD to be extremely simple for me, barely going out of my way. So why not apply for both?

I think I’ll apply for Old Blue one of these days, and then a little before November 1, I’ll go for the TD.

Wish me luck on getting two easy approvals!

Do the drugstore accept Amex cards for VGC purchase? I thought they only accept Visa, MC and Discover. So how can you use old amex card ? Even Walmart and Target won’t accept Amex to purchase VGC. The only option left is amex for Target. Is this correct?

Amex for Target doesn’t work anymore. Drugstores typically do accept Amex credit cards for Visa gift card purchases, but not always.

Regarding the target factor, you’re saying the TD card doesn’t code Target as a supermarket, even though the VISA site says that particular target store does? That’s a bummer if that’s the case…

How about the WF card? I can’t find any datapoints on how WF treats Targets that VISA considers grocery stores. Would love to get 5k spend at 5% with Redbird

Any datapoints on the Citizens bank cards?

I am referring to a Target store that Visa codes as a grocery. Additionally, in my TD login itself, the system calls it a grocery store. Yet they still coded it not to earn 5%.

I just recently saw somewhere (maybe it was on Reddit somewhere) that both Citizens and WF do get 5% for Target’s which are coded as grocery stores.

I’ve had Old Blue for years and have hit it pretty hard. My CL is $25K (recently bumped) and I have no problem cycling through that or more. Though I can back up my income and I do have work-paid expenses to fall back on, should I need it for FR.

I do use this card for regular spend, too. Groceries, gas, etc.

Wow, you cycle more than 25k per month?

And how long have you been doing big volumes?

Great datapoint. Do you have any idea of your ratio of ms spend to non-ms spend? Thanks.

Have Old Blue for more than 6 months, been doing GC for 8-12k a month mixed with 2-3 small amount of gas or grocery transactions with no issue.

Okay, I’m really getting convinced that there’s no issue with hitting this hard!

I would still like to hear from more people who have been doing this for a few years.

I would definitely go for the TD and Blue, and then WF after the TD runs out. It actually will save you a lot of time. It’s very hard to do back to back GC purchases, or even multiple large purchases in a day without getting fraud calls. So by having at least two if you have a grocery store next to a drugstore you can hit up both without a fraud alert.Also WF likes to hold up your credit line up to a week after receiving a normal ACH payment. You can get around that by making in branch cash payments, which is the perfect way to recycle AFT cash, or transferring from a WF checking account.

Interesting points. Thanks Arielle.

Look back at the T&C. It’s only after you spend $6500 every reward year, not only the first year, that you get 5/1% back indefinitely. Changes your math.

I thought I calculated that in. No?

I calculated $13,000 for two years.

I’m the AU on the Old Blue since my boyfriend is too lazy/busy to MS. The Old Blue has a low-ish credit line compared to his other Amex cards, and I cycle through it 5-7 times in a month. As an AU. In the beginning this got annoying fraud warnings that required me to call in, but those have largely stopped and instead, it’s our favorite money maker. As far as I can tell, the worst Amex does is verify income rather than the full shutdowns you fret about, which are more of Chase’s MO.

Thanks for the data point. How long have you had it?

~9 months now as an AU, although this is the first Amex he’s ever had so he’s had it for something closer to 8 or 9 years.

Thanks.

Regarding how much caution to exercise: We got the Old Blue half a year ago and have gone pretty hard at it. Amex very kindly issued the card with a $25,000 credit line, and we’ve come close to that amount a couple of times. Every swipe has been approved, whether for $505.95 or for 10 times that amount. Never a call or a concern. We use the card 95% for gift cards, plus a bit of gas and groceries mixed in… everything in the 5% categories. Lest you think that might raise a flag, the opposite seems to be true In fact, last week the mailman brought a nice letter from our friends at Amex. Because you’re such a good customer, we’ve increased your credit line to $30,000. Go Blue!

Thanks for the precise data-point. If I get approved, I’ll definitely hit it harder based on your experience.

I’d love to hear more data-points on this point. Can anyone else tell us their experience with hitting Old Blue hard?