Chase will soon apply their famed 5/24 rule to co-branded credit cards as well. The rule says that those with five new credit cards within the past 24-months will not be approved for a new credit card application.

Currently, only Chase’s own line of cards has the 5/24 rule, including the Freedom card, Sapphire card, and Slate card. We previously reported that sources say the 5/24 rule will soon apply to Chase business cards as well.

- Chase Credit Card Churning – Living with the New Reality (5/24 Rule)

- Chase Credit Card Limits (5/24) Soon to Apply on Business Card Applications

This trusted source now tells us that in a separate move, Chase will apply the 5/24 rule to co-branded cards as well, including cards like Southwest, United, Hyatt, and the rest of Chase’s co-branded card line-up. This will apply both to personal co-branded cards and to business co-brands.

The new rule is likely to start in April. We can expect a timeline which will look something like this:

- Currently, once past 5/24, you can not get Freedom, Sapphire, or Slate. You can get all other cards.

- At some point in March, the INK cards will be restricted as well. We can still get personal and business co-branded cards.

- At some point in April, all Chase credit cards will be included in the rule, and those past 5/24 won’t be approved for anything.

This timeline reflects the upcoming change as it’s being said now. There is a possibility that it will take slightly longer for the rules to come into practice.

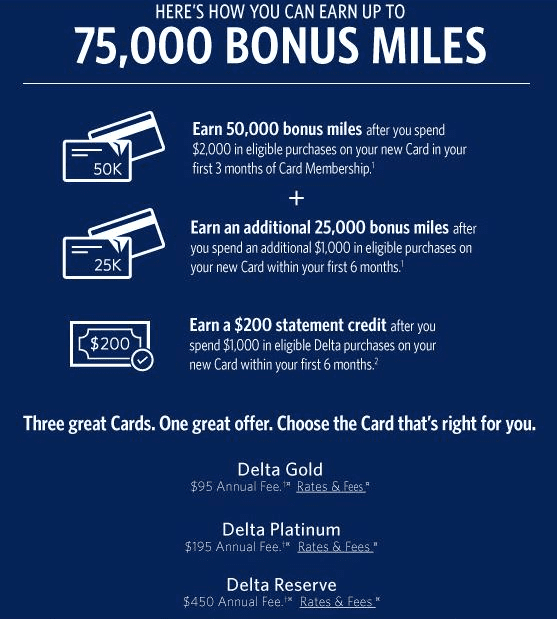

The era of churning Chase credit cards will soon come to an end. Get whatever you can now.