Update 08/23/18: Bonus has been increased to $150 (from $100) after $500 in spend. Still not very attractive. Hat tip to reader Steve

As I predicted yesterday, Ally Bank has released its first credit card called simply ‘CashBack’. The card is issued by T.D Bank and apparently Ally are using this to gauge interest before possibly releasing cards issued by themselves in the future. Let’s take a quick look at the features and benefits of this card:

- No annual fee

- Sign up bonus of $150 after $500 in spend within the first three billing cycles

- Card earns at the following rates:

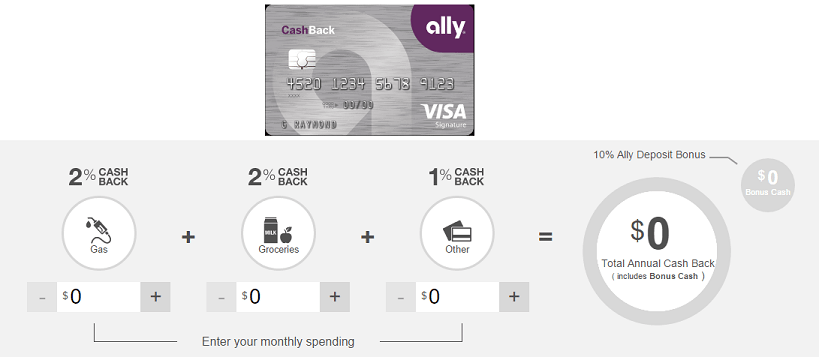

- 2% cash back at gas stations and grocery stores

- 1% cash back on all other purchase

- Get a 10% Ally Deposit Bonus when you deposit your cash rewards into an eligible Ally Bank account

- No cap on the amount of rewards you can earn

- 0% Introductory APR for first twelve billing cycles

Our Verdict

This card is pretty useless, let’s see why:

- You can earn up to 2% cash back on all purchases (this card offers a maximum of 1.1%)

- You can earn up to 5% cash back on gas (this card offers a maximum of 2.2%)

- You can earn up to 3% cash back on groceries with no cap, or up to 5-6% with a cap (this card offers a maximum of 2.2%)

- There are a lot of cards with a higher sign up bonus than $100 in cash.

It’s good to see Ally getting into the credit card space as they are a pretty good bank, but this offer just isn’t of interest to me at all, fingers crossed they come up with something better.