Today is American Express’ investors day, one of the things they have touched on is people gaming credit card rewards. Unfortunately there is no transcript of the event (update we now have a transcript, relevant sections below the slides), but we do have the following slides from their presentation.

In addition Bloomberg have some quotes:

- An increase in incentive bonuses has boosted so-called gaming by credit-card applicants looking for a quick reward, Doug Buckminster, president of global consumer services said

- “opportunity to use our analytics and technology to surgically remove gaming and reinvest in higher-quality, more loyal new customers…”

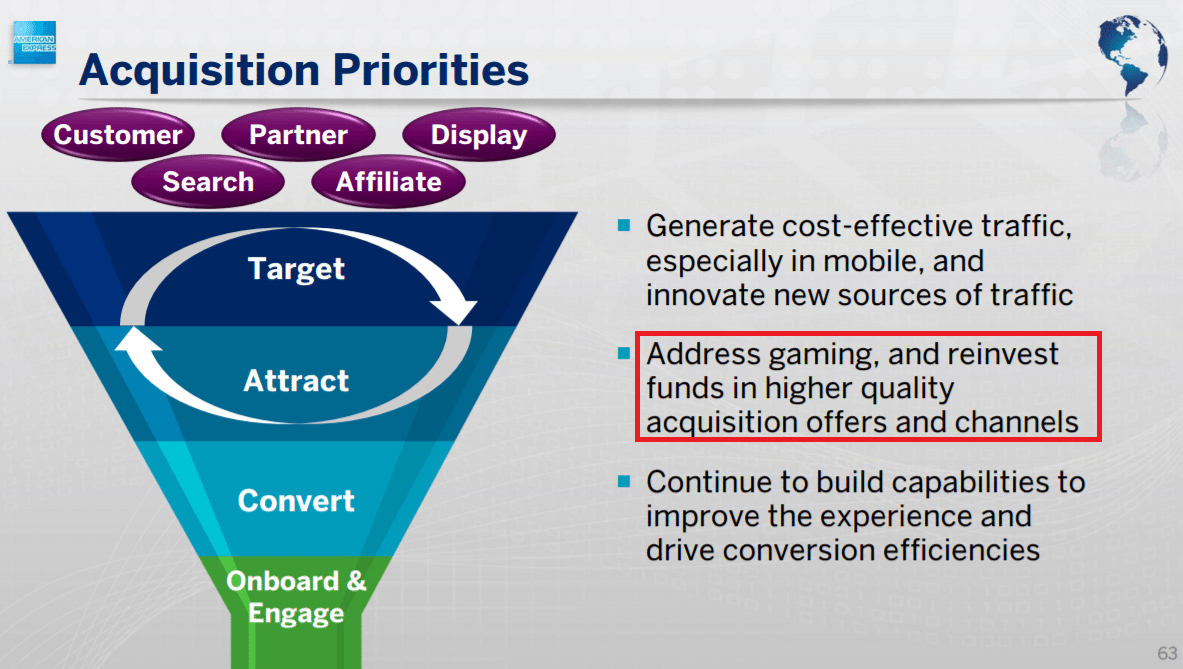

p63 of slides

Transcript

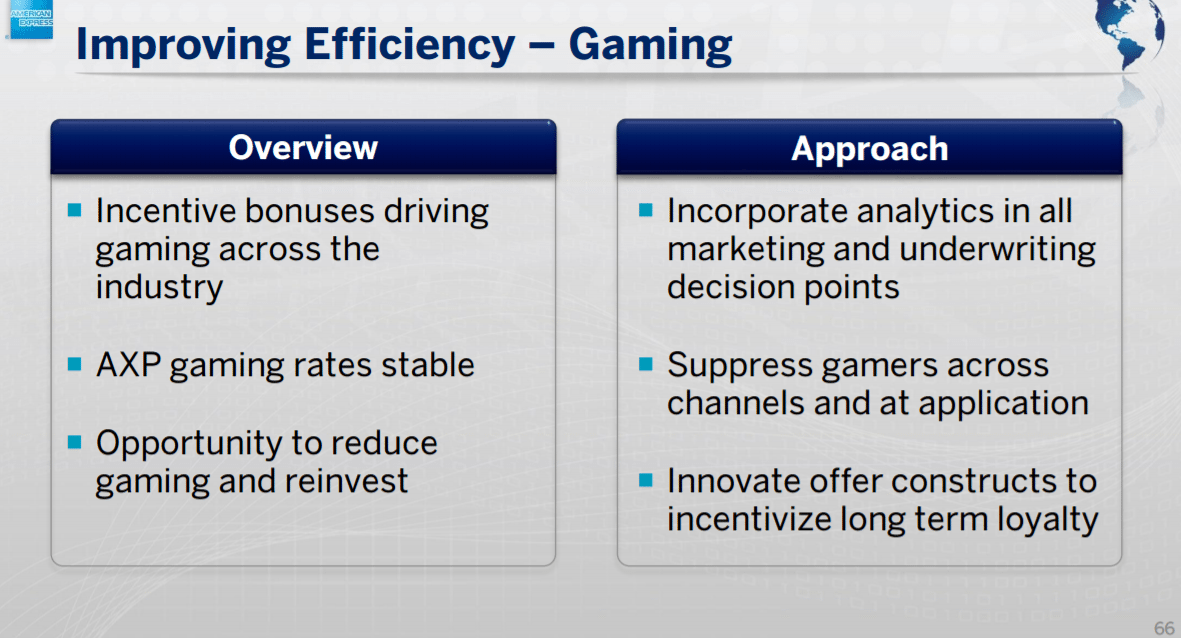

So turn my attention to efficiency and to a topic that has been popular in industry circles these days, and it goes by various names, gaming or churning. And for purposes of this discussion, I’ll define it as a consumer taking out a new credit card account, engaging in the first 3 or 4 months at the level required to earn the acquisition incentive, a cash back incentive or airline points, and then disengaging and moving on. And certainly, the very intense, at times bordering on irrational, competition based on rich sign-up bonuses and a whole social media ecosystem that’s grown up around this particular phenomena has put pressure on gaming and churning trends. Now our more conservative incentive structure and the controls we have in place have largely kept gaming rates constant over the last couple of years, but we still see a substantial opportunity to use our analytics and technology, surgically remove gaming and reinvest in higher-quality, more loyal new customers, achieving an acquisition efficiency gain on a year-on- year basis. And so we’ll leverage technology and analytics at all of our marketing and underwriting touch points. We'll suppress gamers across channels and at the point of application.

Key to enabling all of these use cases from corporate cross-sell to member referral to gaming reduction is our new dynamic application and underwriting technology. And this technology supports custom application flows, it’s device responsive, it allows applications to be interactive with a customer with respect to their data entry. And it allows customer underwriting applications as well. In short, this new suite enables us to maximize conversion rates, while optimizing margins through interactive negotiation with applicants.

In the question & answer section it was briefly mentioned again:

And listen to what Doug said on gaming. My view is you’re going to hear a lot more about gaming in the next 12 to 36 months in the card industry, a lot more about gaming. What we’re focused on is long-term, sustainable, profitable relationships with our customers. Yes? All right, Ken?

What This Means For Us

Honestly I don’t think this means a great deal, American Express already have their once per lifetime restriction and a rewards abuse team. I think there are a few other areas they could target (I won’t tempt fate by mentioning them), but for the most part they have already locked down their rewards for gamers.

The issue credit card issuers have is they want to restrict unprofitable customers (“gamers”) from signing up and receiving bonuses and at the same time ensure that people who are profitable can still sign up. That’s why they have once per lifetime rules, but still send out targeted offers without these restrictions. They also need to balance this with the demands from co-branded partners.

Hat tip to /r/churning