(Update 12/9/24: Booking.com was added as a 3% merchant when shopping in Safari at this link. You’ll also get 2% back in Booking.com travel credits.)

At the Apple Event today, they unveiled full details on the release of the impending Apple credit card which we’ve covered before. The card is called Apple Card and will become available this summer. The Apple launch video can be found below.

Apple Card

The new Apple Card is issued by Goldman Sachs and will run on the Mastercard network. The card runs entirely through Apple Pay, and I’m not sure it’s possible to signup for the card if you don’t have an iPhone.

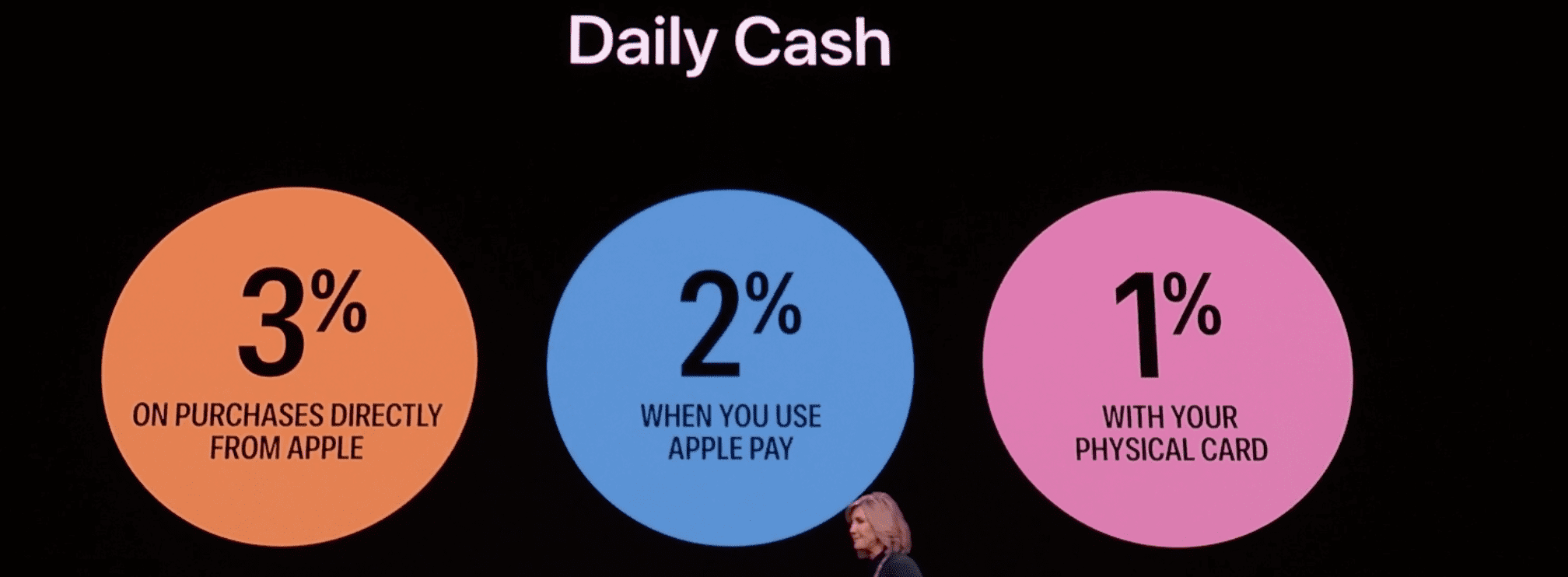

Card will earn the following rewards:

- 3% cash back on Apple purchases and services (including the app store, Apple Music payments, etc.)

- 3% cash back on Ace Hardware, Booking.com (at this link; you’ll also get 2% back in Booking.com travel credit),

Panera Bread, Exxon/Mobil, Walgreen’s, Duane Reade, ChargePoint, Uber, UberEATS, T-Mobile store purchases, and Nike when using Apple Pay - 2% cash back on all Apple Pay purchases

- 1% cash back when using the physical card

There’s no limit to how much rewards you can earn.

No mention of a signup bonus, but we’ll have to wait until launch to see if they offer a little something (they’ve already said previously that there was no plans on a big bonus).

Card Details

- No annual fee

- No foreign transaction fee

- No cash advance fees

- No late payment fees (late or missed payments will result in additional interest accumulating toward your balance)

- No over-the-limit fees, no balance transfer fees, no expedited card delivery fee

- Variable interest rates (as of March 2019: APRs range from 13.24% to 24.24% based on creditworthiness). No penalty interest rates, even if you miss a payment.

- Card instantly available upon signup for use with Apple Pay; physical card will come later, but most stores accept Apple Pay making it another one in the list of cards instantly available upon approval.

- Physical card is made from titanium laser etched with your name. There will be no card number, no expiration date, and no signature on the card.

- Cash back is issued daily to your Apple Cash card and can be used immediately to buy something, pay your bill, send to a friend via iMessage, or transfer to your bank.

- Customer service via text from your iPhone

- Organization tools to clearly show your spending totals and more

- No word on whether there’ll be any sort of protections, like purchases protection, return protection, car rental insurance, etc.

- For apps and website use, there’s a virtual card number in the Wallet app. It autofills for you when you’re using Safari. It’s not clear in the presentation or on the apple site whether transactions made with this card number are like Apple Pay transactions which earn 2% or like physical card transactions which earn 1%.

Update History

- Update 4/20/21: Apple now added a feature called ‘Apple Card Family’ which allows users to share their Apple card with someone else 13-years or older. Basically the equivalent of an authorized user card, though it does come with additional controls on spending; pretty cool. They’ve also introduced joint cardholders where two people (e.g. spouses) can share the responsibility on a card together and build credit as well. Existing Apple Card customers can also merge their Apple Card accounts, giving the flexibility of a higher shared credit limit.

- Update 7/21/20: Apple Card Now Reporting Card History To Both Experian and TransUnion Credit Bureaus

- 7/2/20, a few updates:

- Apple Card now offers an online login where you can see transactions, make payments, etc. Sign in with your Apple ID.

- You can also apply for a new card online in a web browser. It’s now possible to be an Apple Cardholder without owning an iPhone/iPad.

- Apple has also launched a Path to Apple Card program for those denied the card to eventually become eligible.

- They also added a $50 signup bonus for July 2020.

- Update 8/20/19: Apple Card is now publicly live for anyone with an update iPhone (requires iPhone 6 or later).

- Update 8/7/19: Readers are reporting no hard pull is done if you’ve been invited to apply for the card. Update #2: Many readers are now saying that a hard pull is, in fact, done (Transunion), and a frozen credit report will impede the application.

Our Verdict

It’s basically another 2% card, but only for Apple Pay transactions (and possibly for purchases with the keyed-in number from the app, see above). Most stores accept Apple Pay; depending where you shop, the 2% earn rate may apply for most of your purchases.

Going through the fine details, it does come out at the top of the pack due to the lack of foreign transaction fees, lack of cash advance fees (makes it safe for bank funding and the like), and the fact that the cash back is instantly available.

And of course, you’re dealing with the Apple brand – I have to admit that Apple does a good job at introducing it like a revolutionary thing. In reality, it’s numerous tweaks to a regular 2% card (privacy, transaction clarity, text customer service, no card number etc). Seems pretty cool overall, to be honest, and especially useful for international purchases.

The biggest limiter of the card is that it’s only for iPhone users. And some people prefer to just swipe a physical card – that will only get you 1% rewards. There may be some stores or websites where Apple Pay doesn’t work, and in these cases you are limited to 1% rewards.

For someone, who anyway uses Apple Pay for most transactions, and who anyway uses a 2% card, I’d say this card is a go. Otherwise, it’s still another 2% card added to the market, and one with no annual fee and no foreign transaction fees. Check out this follow-up post for Five Better Alternatives To The New Apple Credit Card.

Here’s an image of the card:

#AppleCard pic.twitter.com/eRt9aUAyRp

— Ben Geskin (@BenGeskin) May 11, 2019