Card has now been officially launched, you can read our full review here.

Bank of America will soon release a new premium version of their Travel Rewards card. We’ve written about it before, here’s an update with key details that were confirmed in this WSJ report. [If you don’t have a WSJ subscription, you can see it on Fox Business, though there is a graphic in the original article – pictured below – not shown on Fox. Use Facebook or Twitter to bypass paywall.]

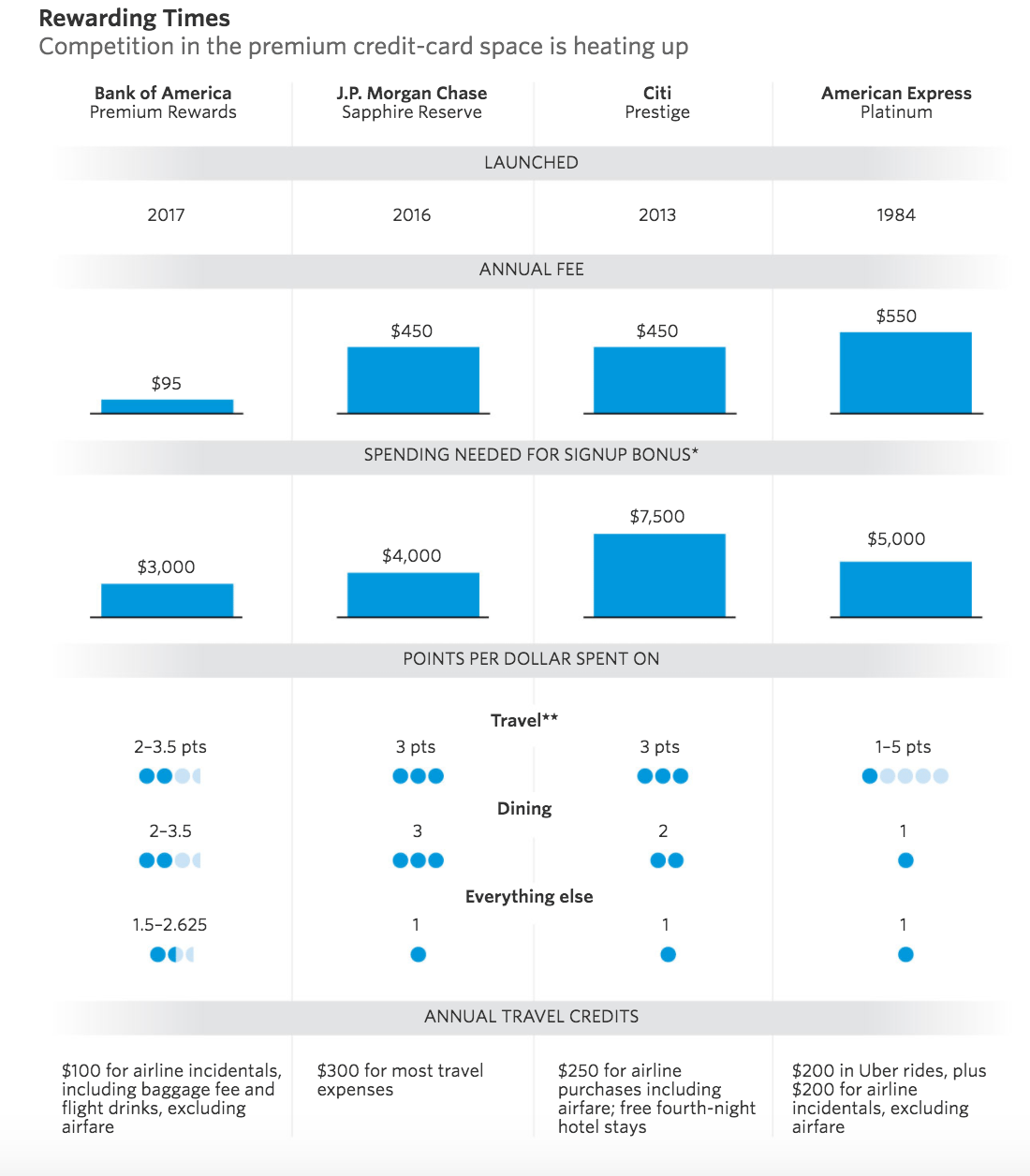

- $100 airline incidentals credit, including baggage fee and flight drinks (does not include airfare)

- 50,000 points signup bonus will have $3,000 spend threshold

- The annual fee will be $95

- 1.5x everywhere and 2x on travel/dining; Preferred Rewards customers will get up to 2.6 everywhere and 3.5 on travel/dining

- It will roll out in September

- It will be a Visa card

- BofA has told Business Insider that there will also be $100 Global Entry/TSA PreCheck credit

We reposted most of this info in a post earlier today, but I missed the $100 airline incidental point which shows in the graphic on WSJ. This credit is a critical component in deciding whether it’s worthwhile to get the card for the bonus. It remains to be seen exactly what will count for the airline incidental credit (gc, MPX, etc).

There’s no mention of a Global Entry credit, and for now I’m assuming it won’t have one.

Analysis

At this point, it seems we have most of the card details confirmed. My feeling is that Bank of America isn’t looking to compete with the other premium cards, they are more looking toward Preferred Rewards customers who keep other money with them. They don’t want existing clients with assets going elsewhere for their credit cards, and they are hoping to attract more clients with assets under the BofA umbrella since 2.6x everywhere and 3.5x on travel/dining are both nice rates, especially for a $95 annual fee card with no foreign transaction fees.

As far as keeping this card long term, it mostly makes sense for Preferred Rewards clients. Without any status, you’ll probably be better off with other cards. For those with top-tier Preferred Rewards card, it’s basically an improved version of the Travel Rewards card which earns an excellent 2.6x everywhere. The improvement here is the 3.5x on travel and dining.

If you value the travel incidental credit at somewhere close to it’s value, there isn’t much question that it’s worth keeping this card instead of using the no-fee Travel Rewards card. If you won’t use the incidental credit, you’re paying $95 for the extra .9x on travel and dining – you’ll have to crunch the numbers to see if that’s worthwhile for you. Bear in mind, travel and dining are heavily bonused categories with other banks, and 3.5x isn’t necessarily better than 3x Ultimate Rewards points on CSR, for example. So for a lot of people the fee won’t be worth it if you don’t value the airline incidental credit.

As far as getting this for the signup bonus, it’s basically worth $405 after discounting the $95 fee – there’s no mention of the fee being waived the first year. [The signup bonus on Travel Rewards does not get compounded the way it does on Cash Rewards cards.]

Depending how you value the $100 incidental credit and how strict they’ll be, you might be able to get an extra $100 value there or close to it. Without the extra $100, I view it as an okay bonus but not amazing. I like getting $500+ value from a new card. Many other people are happy signing up for a card which gives them $200+, and this will be well-worth it.