[Originally posted on 5/21/15. We’re reposting it now again as it’s available again until the end February.]

Offer at a glance

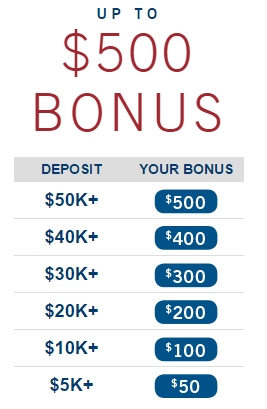

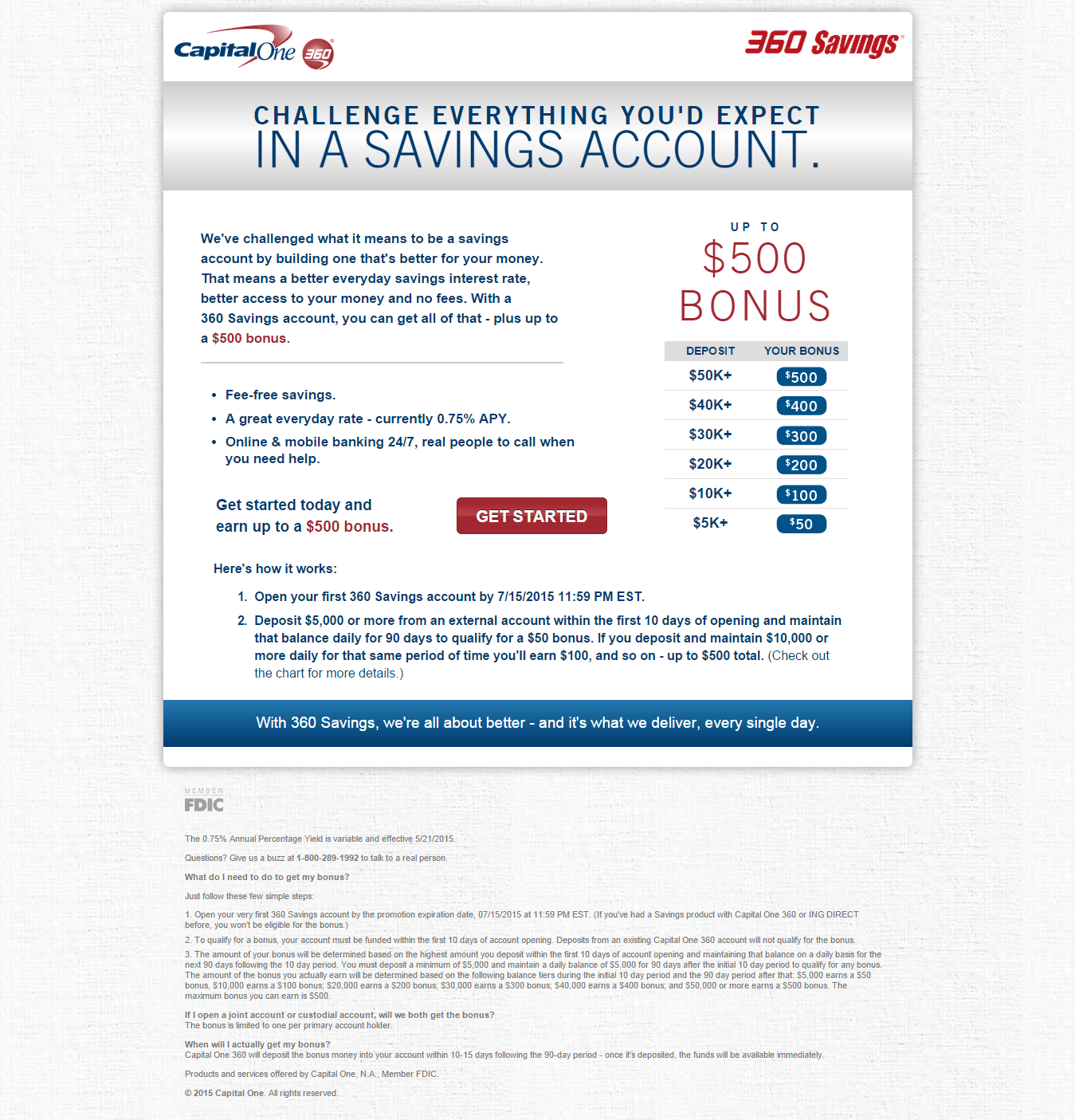

- Maximum bonus amount: $500

- Availability: Nationwide

- Interest rate:

0.76% APY0.75% APY - Deposit requirement: Starting from $5,000

- Deposit length: At least 90 days

- Hard/soft pull: Soft

- Credit card funding: None

- Monthly fees: None

- Early account termination fee: None

- Expiration date:

September 30th, 2015November 30, 2015February 29, 2016March 31, 2016

The Offer

- Receive a bonus of up to $500 when you open a Capital One 360 Savings Account, deposit new funds into that account and maintain those funds for at least 90 days. The bonus you’ll receive will depend on amount you deposit into the account as follows:

The Fine Print

- Deposit must be made within 10 days of account opening

- Funds transferred from existing capital one 360 accounts do not qualify

- The bonus is limited to one per primary account holder

- Bonus will be deposited within 10-15 days after the 90 day period.

- All bank account bonuses are treated as income/interest and as such you have to pay taxes on them

Avoiding Fees

There are no monthly fees for this account and no early account termination fees.

Our Verdict

Before I dive into this bonus, I’d just like to point out that there are affiliate links available for this offer – so tread with a bit of caution (remember we don’t use affiliate links for bank bonuses). The other thing to keep in mind is that twice a year (Black Friday & Independence day) they offer promotions and you can usually get a bonus of $76-$100 on the savings account (with a deposit requirement of ~$500), because of this the $50 and $100 bonuses really aren’t worth considering.

Let’s take a look at how this Capital One 360 bonus compares to other savings accounts, we’re only looking at the first three months because after you’ve earned your bonus you shouldn’t be keeping it in a 0.75% APY account. We’ve included up to 5% APY, because it’s possible to get that with a rewards checking account (consumers credit union) and some prepaid accounts.

| Capital One 360 | 1.00% | 2.00% | 3.00% | 4.00% | 5.00% | |

|---|---|---|---|---|---|---|

| $50,000.00 | $593.00 | $125.00 | $250.00 | $375.00 | $500.00 | $625.00 |

| $40,000.00 | $475.00 | $100.00 | $200.00 | $300.00 | $400.00 | $500.00 |

| $30,000.00 | $356.00 | $75.00 | $150.00 | $225.00 | $300.00 | $375.00 |

| $20,000.00 | $237.00 | $50.00 | $100.00 | $150.00 | $200.00 | $250.00 |

As you can see, you’re better off with this Capital One 360 account until you hit that 5% mark. But what you also need to consider is that instead of opening this account you could open another checking or savings account for a bonus (hell, you could even open this account during black Friday or independence day sale).

If you opened another account for a $100 bonus, suddenly this Capital One 360 deal becomes less attractive. Personally I think most people would be better off going for one of our recommended bonuses instead and putting their money into a high interest checking account or prepaid card.

That being said, for those that don’t want to bother with the requirements of a high interest account and have funds sitting around this is a good opportunity to get a nice bonus/have your funds earning at a higher than normal rate for a few months at least.

{kind=link}