Update 11/3/23: Added note below about possible new rule which auto-declines applications if there was a hard pull done on your credit report from any bank in the past 5 days. This also may cause a decline for another 60 days since Citi will just use the old credit pull for up to 60 days. (After 5 days you can call reconsideration and ask them to run your credit report again for approval.)

Original Post:

Citi has strict rules on how many card applications they’ll accept from someone. Many people are confused about this, and we’ll try explaining Citi’s rules as clearly as possible.

Note: This post is not about Citi’s 24-month rules regarding how frequently you can get a signup bonus (we have a separate post on that churning rule). Here we’ll discuss when they’ll process your application at all and when they’ll deny you, often without even pulling your credit.

There are still some question marks here – please contribute your own data points in the comments. We’ll try to keep this post updated with any future rule changes as well.

Contents

Personal Cards (8/65)

There are two rules to be aware of regarding Citi personal cards:

- Must wait 8 days after application before applying for another card. While this rule is well known, there are data points of those who got approved for a second card within 8 days, so this might not be a hard rule (Flyertalk). Based on this, I’d guess that a hard pull will be done for applications within 8 days.

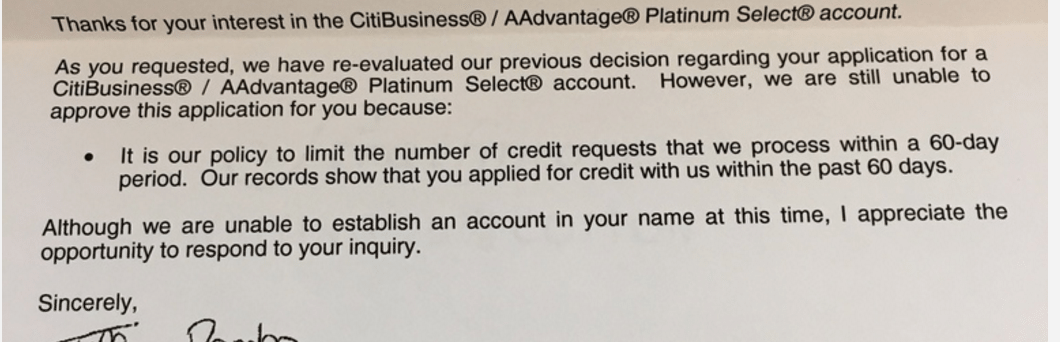

- No more than 2 Citi applications within 65 days. The real rule is 60 days, but it’s become common to wait 65 as a safeguard since Citi has been known to miscount.

These two rules have borne the short-hand ‘Citi’s 8/65 rule’.

That is, after applying for a Citi card (Day #1), wait eight days before applying for another Citi card on Day #9. Then you’ll have to wait until Day #66 to apply for a third card. Then on Day #74 you can apply for the next one. And so on.

Business Cards

Regarding business cards, the rule is as follows:

- Must wait 90 days between business card applications. Again, we’ll wait an extra 5 days to be safe.

For example, if you apply for a business card today Day #1, you can apply for another business card on Day #96.

Personal + Business Combo

It appears that both business cards and personal cards combine toward for the 65-day wait. A friend reports that during a recent business card application, Citi didn’t even do a hard pull due to the fact that he had done two personal two applications within the past 60 days. Other reports (1, 2) confirm this as well.

The 8-day rule is often relaxed when applying for one business and one personal card, meaning that you can apply for a personal and business card on the same day or the same week and don’t have to wait 8 days in between (Frequentmiler and others). This can be the case even when applying for both with your SSN. Being the 8-day rule is a soft rule, it’s difficult to track solid data on this.

You can apply for a business card using an EIN within 8/65 since business applications run separately. Thus, it’s possible to get three cards within 60 days (2 personal and one business) (1, 2, 3). [However, note, there are data points indicating that while EIN applications don’t count your previous SSN applications against you, SSN applications DO count your previous EIN applications against you (1). Hopefully, this makes sense.]

Notes about the Rules

- Even denials count. For example if you were denied for your second card on Day #9, you still have to wait until Day #66 for the third application. And the same is probably true for business cards: if you were denied a business card, you’ll have to wait 95 days to try again.

- If your application did not get processed, e.g. if you violated the 8/65 rule, that application will likely not count against you toward your 8/65 (Reddit).

- The only day that matters is the application date, not the card approval date.

- All calendar days count, even non-business days.

Other Rules

5-Day Credit Pull Rule

Frequentmiler has some reports indicating a possible new rule which auto-declines applications if there was a hard pull done on your credit report from any bank in the past 5 days. This also may cause a decline for another 60 days afterward since Citi will just use the old credit pull for up to 60 days. (After 5 days you can call reconsideration and ask them to run your credit report again for approval.)

New 1/60 Rule?

In the past few months, some people have been told by Citi that only one new card can be approved per 60-days.

Is there a new 1/60 rule? Based on numerous data points, my understanding is that this is not a firm approval rule. There does seem to be a fraud detection in place when you apply for two cards within 60 days which requires manual intervention. I believe this issue is only when you apply for two of the same cards (e.g. two AA cards), but not when you apply for two separate cards.

Max Hard Pull Rule (6/6)?

Many people mention that Citi does not approve applicants who have six hard pulls on their credit report within the past six months.

There’s not a whole lot of information out there on this rule, but it’s probably a generalization, not a firm rule. There will presumably be a hard pull if you apply when you have more 6/6.

Since this rule tracks pulls, not cards, it’s much easier to get around it by spreading your hard pulls around various credit reports. Most people are usually under 6/6 since even if they do have six hard pull, overall, in the past six months, there will be a few pulls with each credit bureau, not six with a single one.

Max Credit

This isn’t a rule, but some people mention having a hard time getting approved for a card after they have a certain number of cards, or, perhaps, a certain amount of overall credit limit with Citi. This is probably true for a lot of card issuers, and it’s something to keep in mind.

If you have too many cards and high credit limits, consider proactively closing some of them before applying. Or try asking the credit analyst to close out another card in order to get the new one approved.

FAQ

1) You say that denials count. What if I mistakenly applied for a third card within 60 days. Does the 8/65 start over or is the dead application rendered non-existent?

Flyertalk suggests that your clock probably resets anyway, as if it were a real application. Some data points confirm this as well. (I did hear one data point about a Citi business card which would seem to suggest otherwise regarding the 90 day business rule.)

2) Is a product change considered an application toward your 8/65?

Logically, it shouldn’t count since it’s not an application.

3) If you have a targeted offer which doesn’t have the 24-month language, will it bypass the 8/65 rule?

No. It’s subject to 8/65 and it counts against future applications as part of 8/65.

4) Any advice if can’t remember the exact date I applied?

You can figure it out from your application number. The date is written year/month/day in the application number. For example, 201412150000 means you applied on December 15, 2014. (Flyertalk)

5) Is there an easy way to count up 8/65 without adding up the days on the calendar?

6) Can I apply for a card I already have to have two of the same card?

You can usually do that with personal cards but not with business cards. That does not mean you’ll get the bonus on the second card. Read more about that here.

Other questions? Drop a comment below.

Other posts worth reading about Citi cards: