[This page does not contain any affiliate links. If you sign up for an account with Credit.com we don’t receive any monetary incentive. We post honest reviews regardless of our financial connection to the companies reviewed. We appreciate you using our links when they are present]

Credit.com was founded by Adam Levin who used to be the Director of the New Jersey Division of Consumer Affairs from 1977 till 1982. It gives consumers free access to their credit scores, based on Experian information. It is similar to other free credit monitoring services such as Quizzle, Credit Karma & Credit Sesame.

Contents

Credit.com Credit Scores

Credit.com providers consumers with access to two different credit scores. They give users access to their Experian National Equivalency Score (same score offered by Credit Sesame) & their Experian VantageScore 3.0 credit score (Equifax VantageSc0re 3.0 is offered by Quizzle and TransUnion VantageScore 3.0 is offered by Credit Karma).

Is It Really Free?

Credit.com doesn’t require any credit card to sign up, you only need to enter some basic information so that they can verify your identity. They make money in a number of ways, the first is by trying to upsell you on other products (such as your credit reports through creditreport.com and identity theft protection through Identity Guard).

They also make money by selling consumers financial products, such as credit cards, home loans, auto loans or refinance loans.

Is The Credit.com Score Accurate?

Lenders don’t really look at your Experian National Equivalency Score (ENES), as such it is accurate but it’s not really that useful. This is because even if you have a perfect ENES score, it’s not going to matter unless a lender actually uses it as part of their lending decision. When we compared our ENES score to our Experian FICO score there was a difference of 12 points (with the ENES score being higher, despite the fact that it has a lower scoring range).

Financial institutions do look at VantageScores, although they are probably only used in less than 5% of all decisions (whereas FICO scores are used in 91% of all decisions). When we compared FICO & VantageScore our VantageScore was 75 points lower than our FICO score.

Our Thoughts

Both of the scores offered are really only for “educational” purposes only, as such they should be used as a general indication of your credit health. It’s OK to look at these scores, it’s just important to remember that they are not the same scores that lenders will be looking at when they either approved you or deny you for new credit.

Credit.com Credit Reports

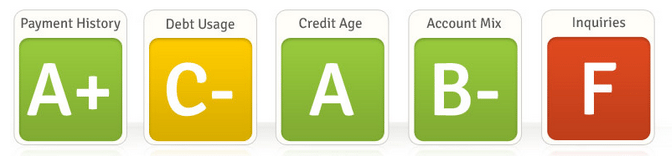

Unlike the other free credit monitoring services on the market, credit.com doesn’t give you access to your credit report. Instead they give you something called a credit report card. This gives you an A-F grade on specific scoring categories, such as:

- Payment History

- Debt Usage

- Credit Age

- Account Mix

- Inquiries

Credit.com Credit Tools

Action Plan

Credit.com gives you a personalized action plan depending on what is found in your credit report. For example, if you have a high credit utilization (they call it debt utilization) they’ll recommend it. They market it as being customized by their experts, this doesn’t mean that an expert actually looks at your credit report. What is actually happening is that all the negative factors are being looked at by a computer algorithm and then generic advice is given.

If you’ve read our in depth article on FICO scores, you probably have a good grip on what you can do to improve your credit score and as such won’t find these custom action plans particularly insightful. If you haven’t read that article, here is a basic summary:

- Lower your credit utilization ratio to 1-10%

- Have a mix of credit types (e.g both revolving and installment loans)

- A longer credit history is better than a shorter one (the average age of your accounts is also important, so don’t close accounts unless you have to pay an annual fee to keep ’em open)

- New inquiries will generally lower your credit score, they stop affecting your score after a period of one year and fall off your credit report after a period of two years.

- Late payments/delinquencies will lower your score

Expert Advice

If your a credit.com user you can ask questions in their online forums, where their panel of “experts” will answer all of your questions and queries. Given the number of other online forums that are out there, this doesn’t really provide a lot of value. Here is a list of some of our favorites and what they are good for:

- Creditboards.com – Credit score questions

- MyFICO.com – FICO score questions/rebuilding credit questions

- FlyerTalk.com – Points & Miles questions

Find Savings

The find savings section of the credit.com is really where they make the bulk of their money. They’ll recommend products that they receive a commission on that’ll also save you money. The problem is that they have an invested interest in promoting options that pay them the most. It’s fine to look at this section for ideas on where you can save money but just make sure you always do your own independent research to ensure that you’re selecting the best option for yourself and not the option that pays them the most.

Credit Monitoring

You’ll also get basic updates on how your credit is changing (e.g is your debt increasing or decreasing over time) as well as alerts for major credit changes.

Our Final Thoughts

Out of the four free credit monitoring sites currently on the market, Credit.com has the most basic suite of tools. They also offer credit scores that aren’t really used by lenders and are already offered by the other sites on the market. As such we don’t see a lot of value in signing up for an account. It is free though, so feel free to sign up for an account to make your own judgement. Just keep in mind the other sites offer better value in our opinion.

- Quizzle: Provides information based on your Equifax credit report

- Credit Sesame: Provides information based on your Experian credit report and provides free identity theft insurance

- Credit Karma: Provides information based on your TransUnion credit report and has the most robust credit tools on the market