[Update 6/19/17: Beginning this month, Amex made a change and now calculates the year as beginning the day after your anniversary date. As such, some of the information in the post (Q1, below) is inaccurate. And I wonder if the mid-month isssue (Q2 and Q3) will change now too.]

American Express offers the ‘Old Blue Cash’ card (OBC) which earns 5% cashback on purchases made in select categories – grocery stores, drugstores, and gas stations – up to $50k per year. All other purchases earn a flat 1% cashback.

There is a caveat, however, that the initial $6500 in annual spend receives a lower cashback rate: category spend earns 1%, and all other spend gets just .5%.

Contents

Questions

Numerous questions arise regarding this initial $6500 requirement:

- Does the reset begin on the exact anniversary date? Or does it begin at the start of the 13th statement? I was told unequivocally by a chat rep that it’s tied to the anniversary date, but my findings indicate otherwise.

- What happens if you cross over the threshold in mid-month? Logically, dollar $6501 and up should earn the higher cashback rates of 5% or 1%. This, indeed, appears to be the case if you put exclusively category spend during that month and don’t mix in any ordinary spend.

- And what if you do mix category and ordinary spend during the month that you cross over the $6500 threshold? Will the ordinary pre-threshold spend earn the .5% rate and allow the post-threshold category spend to earn the 5% rate? Reasonably, that’s what should happen, but whether this is in fact how it plays out is subject to conflicting reports. Some say that Amex arranges the purchases to your detriment, taking the category spend that happened later as if it happened first and giving just 1% on that spend. My experience is consistent with this approach as well.

- If you spend the initial $6,500 on category spend, does that use up part of the $50,000 bandwidth and leave you with just $43,500 to earn 5% or can you still get 5% on the full $50k? This point is a grey area and is not the subject of this post. We wrote previously that it does use up part of the limit, but multiple reports (1. 2) indicate that it does not and the T&C sound that way as well.

- Does loading Serve count toward the $6500 threshold? This, too, is not the subject of this post. One report indicates that it does not count.

My Statement and Purchases

My card anniversary date is September 18th. My statement cycle went from September 14th until October 14th.

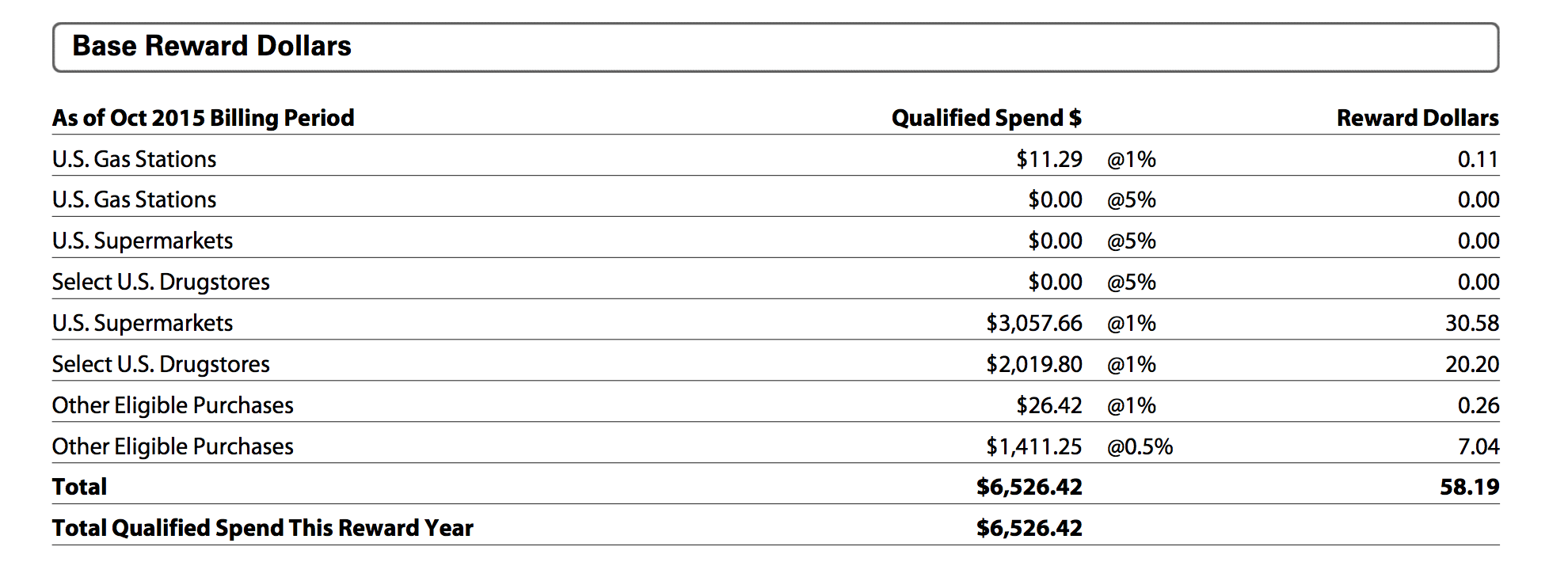

Here are the rewards calculations for my Sept.-Oct. billing cycle, showing on the Oct.-Nov. statement (the rewards from Sept.-Oct. show on the Oct.-Nov. statement):

Here is the order of my purchases:

- 9/13 $14.07 – grocery (apparently, this purchase didn’t clear on the 13th and was thus pushed onto the Sept-Oct statement)

- 9/17 $7.89 – grocery

- 9/18 $3035.70 – grocery

- 9/21 $675 – everyday spend

- 9/21 $2019.80 – drugstore

- 10/9 $762.67 – everyday spend

- 10/13 $11.29 – gas

13th Statement Reset

On the statement shown above, the grocery spend is recorded as $3057 ($3035+$7+$14). Although I fell a few thousand dollars short of hitting the $50k threshold in the 2014-2015 year (I know…unforgivable), the September 13th purchase of $14 earned just 1% back. It’s considered part of the 2015-2016 year and thus only got 1% as part of the initial $6500.

It thus appears that the 13th statement begins the reset, regardless of whether you passed the anniversary date yet. My anniversary date is September 18, and yet a charge made on the 13th is considered part of the new year since it is part of the 13th billing cycle.

Non-Chronological Calculations

On the statement shown above it’s evident that I spent $6526 during the Sept.-Oct. billing, slightly more than the $6500 threshold.

Based on a chronological calculation, the $11 gas purchase made on October 13 should earn 5%, as that occurred after the $6500 requirement was met. But on the statement it shows the purchase getting just 1%. Evidently, OBC advances all category spend toward the $6500 and only afterwards does it calculate the non-category spend.

To be clear, you can earn the higher reward amounts within the first billing statement; for example, if you spend $7k exclusively on gas in one billing cycle, you’ll get 1% on $6500 and 5% on the last $500. Even crossing over the $6500 line in mid-purchase will get you the higher cashback amount on whatever is above the threshold. The only thing that isn’t scored correctly is the chronological order of the purchases.

How to Maximize

To wrap up, there are three methods of optimizing the initial $6500 in spend:

- Spend only in bonus categories and then you don’t need to worry about when you meet the initial spend requirement. Whether you cross over the threshold during the first month, the second month, or any other time will be okay. [Note: You may be hogging part of up your $50k bandwidth by using this method, as noted above.]

- Spend exactly $6500 anywhere in the reset month, even mixing category and non-category spend if you choose.

- Spend $3k or $4k or whatever amount you wish during the first month, but leave it under $6500. Then, in the second month, spend only in bonus categories and cross over the $6500.

Also, as noted, the annual reset seems to be based on the 13th billing, i.e. billing cycle #13 from signup, then billing cycle #25 from signup, and so on. It would be curious to know what happens if someone plays around with their billing cycles and ends up with some shorter billing cycles; possibly, you can speed up the $50k reset that way.

Final Caution: Amex is known to scrutinize new accounts more than old accounts, and it may not be wise to spend $6500 in the first month of a brand new Old Blue account. I can’t promise that it’s safe on an old account either, but if you were in the habit of doing $4k per month, then $6500 isn’t that much more and should hopefully go over fine.

Related: How to Calculate your $50k Annual Spend on INK and OBC

I received my “old blue card” in early Feb. 2018. Does the $6500 spend have to be in the categories, or just the items after the $6500 to get the 5%.

How did you get an “old blue card”? I heard that it might be possible to PC to it, but the link I had to some info died with fatwallet. 🙁

I believe “initial $6500 in annual spend receives a lower cashback rate: category spend earns 1%, and all other spend gets just 0.5%” Then the 5% kicks in after that for the next $50k in grocery category while non bonus category is 1%

Second time this has happened to me. I went cognito, used the link posted here in this thread and Amex shipped me a different Blue card product with different terms. Might be worth a warning to those using the link.

Seriously? I was just about to apply! I really want this card. You used the link Chuck published?

I had an OBC, or rather, a VERY old green card that had the same T&C as OBC. (It was opened in 2002.) It earned 5% at supermarkets and a few other places, after making a spend of $6.5 k each year. It suddenly was replaced with an Everyday card, with no notice or explanation. I simply signed into to my Amex account one day and saw a picture of an Everyday card where the picture of my green Amex card had been.

I had not been using this card much in the past year.

Also here:

https://www.reddit.com/r/churning/comments/4tiyvv/forced_product_change_from_amex_blue_card_to_amex/

I think they sent letters only to people who weren’t using the card a lot.

That thread seems to be about the plain Blue card (which earns MREs) rather than OBC and it certainly makes sense to convert that to the Everyday card.

Similarly the Flyertalk thread letters seem to have gone to those with a previous version of the OBC “We are writing to let you know that the Cash Rebate Card “

Looks like some have received letters – starts around post # 211-213

http://www.flyertalk.com/forum/manufactured-spending/1742033-old-amex-blue-2016-onwards-15.html

There are reports on FT that Amex is converting these accounts to Everyday Blue.

Has anyone gotten this notice?

Also, I am going to assume that if we buy VGCs to meet the $6.5K spend, Amex can detect those as cash equivalents and they won’t count toward the $6.5K threshold?

I haven’t heard anything. Link?

Ok, that might explain my situation. Somehow, even though I applied using the link, they sent me the Blue Cash Card – it does not contain these terms. It only pays 1% for the the G, G and D categories. Looks like I’ll end up cancelling it and re-applying and making sure -before I use the next card – that it’s the card I was hoping to get.

Word to the wise – make sure the card they send you is the card you thought you applied for!

Have you spend the $6,500 threshold? The card is 1% on GGD until then. Any other Blue Cash card is going to give you at least 3% on groceries and 2% on gas, so I doubt you have the wrong card.

Can anyone please clarify – this card (the one earning up 5% up to $50K) is no longer available?

I checked the American Express site and do not see it listed.

Is that correct? If so, maybe delete this thread & article to avoid confusion.

Thanks!

Look in private browsing mode, and it should show up under cashback. Sometimes there is a link under the Blue Cash Everyday references an earlier version of the card, which also points to this

Use this link incognito https://www.americanexpress.com/us/credit-cards/blue-cash/25330

Datapoint – just finished a year; spending 6500 in category did not use up any of the $50k.

Thanks, Steve

Just as a note to others. This past year they actually had my account reset on the calendar year instead of the card member year. My cardmember year ends in November and every year previously that was when it reset, but this past year it reset Jan 1st. Part of the system seemed to still think it started on card member year (showing both 1% and 5% on statements which normally only happens during crossover but with all zeros in one “type”) but figuring out which transactions were counted where showed it started my $6500 tally on Jan 1st. So make sure you pay attention to your statements around the crossover so you can report (or not if in your favor) any errors.

Mine did not get reset with the calendar year.