Note: This is an old post from back in November of 2013, I decided to republish as a lot of people have been asking about meeting minimum spend requirements recently.

Almost all credit cards with large sign on bonuses now require you to spend a minimum amount before these bonuses are unlocked. For example Chase Sapphire Preferred card requires a spend of $4,000 in three months, this may not seem like a lot but for credit card churners that have multiple cards at once it can become difficult to reach the minimum spending requirements. This post contains tips that are not manufactured spend related (e.g buying cash equivalents with a credit card). If you want to get more into manufactured spending, I’d recommend reading these resources.

They do not start when you receive or activate the card, unless otherwise stated so make sure you plan accordingly.

We’ve put together our favorite ways to boost your credit card spend without making frivolous purchases.

Contents

1. Existing Purchases

Whenever you pay for something by cash, debit card, wire transfer or check you should ask yourself (and the person you’re paying) “can I pay for that by credit card?” Here are some ideas to get you started.

-

Put Small Purchases On Your Credit Card

Most big retailers (Walmart, CVS, etc) don’t have a minimum amount that can be charged to credit cards, so even if it’s just a $1 purchase put in on your card.

-

Put Regular Monthly Expenses On Your Credit Card

For example: Utility bills (electricity, gas and water), telecommunications (landline, mobile and internet) and cable can usually be paid for by credit card. It doesn’t hurt to ask your landlord if you can pay by credit card, almost all landlords will say no but asking doesn’t cost a dime.

If your providers don’t allow you to pay by card, see what competing providers say and if there is no price difference, switch!

2. Leverage Your Social Network

-

Pay For The Restaurant Bill

If you go to a restaurant with friends, family or colleagues offer to pay the full bill on your credit card and have the others transfer their share or pay you in cash. This obviously will only work if you get the full amount from everybody.

-

Ask Friends & Family If You Can Put Their Big Ticket Purchases On Your Card

If a friend or family member is planning a big trip overseas or a large purchase such as a television and they don’t make use of rewards cards ask if you can put it on your card and have them pay you back by cash or check.

Some airlines require the cardholder to be one of the passengers otherwise the payment will not be processed.

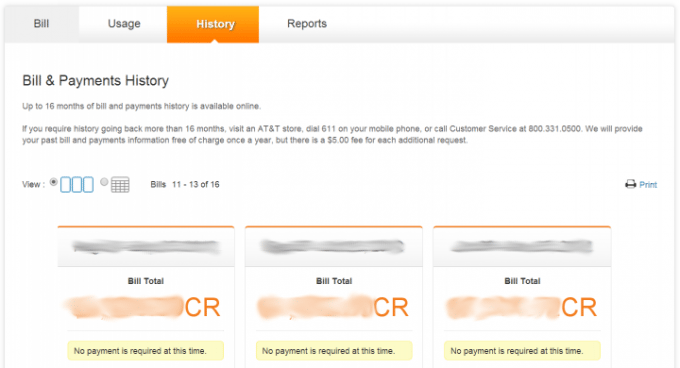

3. Prepay Your Bills

A lot of companies we mentioned above allow you to prepay your bills and carry a positive balance with them. For example AT&T as shown below. A lot of companies will also provide you with a discount they have a fixed monthly fee and you pay for a year in advance (e.g Netflix).

Still struggling? Whenever you pay for something in cash or by check, ask to see if you can pay by credit card in the future.

4. Fund Checking/Savings Accounts

Some checking and savings accounts let you fund the initial deposit with a credit card up to a limit of usually $1,000. This can be a great way of hitting minimum spend requirements and these accounts usually come with a sign up bonus as well.

5. Purchase “Free After Rebate” Products

Occasionally there are products that are free once you complete a rebate form. This allows you to purchase the product on credit card and then receive a rebate from the manufacturer to get your money back. Not only does this increase your credit card spend, you also get a product for free.

Often these free after rebate products are small items only costing a few dollars, but occasionally bigger items are available that can add another $50 or $100 onto your credit card spend. Occasionally you’ll even get rebates so good that you can make a profit (e.g item costs $25 and the rebate is for $50, leaving you with a profit of $25), although these are rare and often cancelled early due to abuse.

Here are a number of websites that list free after rebate products:

- Freebie Depot

- Boarding Area, Frequent Miler free after rebate – not updated often

- Dealigg – hit ctrl+f to and then enter “after rebate” to show items with rebates.

Final Thoughts

I’m sure I’m missing lots of different tactics and some of you may even consider some of the above manufactured spending, feel free to let me know what methods you use to meet minimum spend requirements (without MS) in the comments below.