Card will be discontinued and replaced with the Barclays View card.

[Update 10/28/19: They’ve made various changes to the card, including lowering dining to 3%, dropping the subscription benefit, increasing Uber earn rate to 5%, and shifting from cash back rewards to Uber credit rewards.]

Uber announced today the details of their anticipated Uber credit card. The card will be issued by Barclaycard and running on the Visa network, and will be available for application on November 2, 2017. Key features include 4% cashback on dining, $100 signup bonus, $600 in cell phone insurance, and a $50 subscriptions (e.g. Netflix or Amazon Prime) benefit.

Card Details

Uber and Barclaycard have partnered to issue a Visa card which will be available for application starting November 2, 2017. Card earns the following rewards:

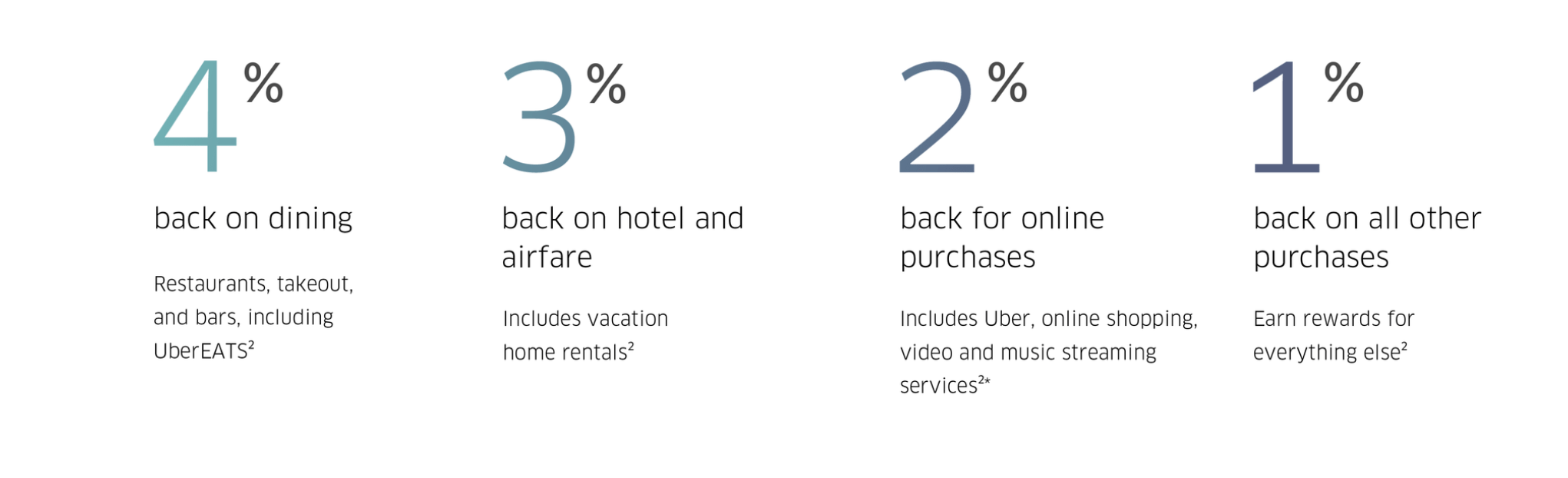

- 4% back on dining which includes restaurants, fast-food restaurants, takeout, and bars, including UberEATS

- 3% back on airfare, hotels, travel agencies, and vacation home rentals including AirBnB

- 2% back on online purchases which includes online shopping, Uber, and streaming services. This includes retailers such as Amazon, Walmart, Best Buy, and Macy’s, as well as Netflix, Pandora, HBO Now, Apple Music, iTunes, and Google Play. And also certain online services like Instacart, Shyp, Angie’s List, Handy, Thumbtack, FlyCleaners, and TaskRabbit. Starting December 5, 2017, it also includes: online purchases paid with third party payment methods including PayPal, Venmo, Apple Pay, Samsung Pay and Android Pay. Does not include: online purchases from merchant category codes that include Utilities, Contracted Services, Government Services, or Professional Services.

- 1% on everything else

Interestingly, the New York Times says to have heard from Uber and Barclays that “point transfers to airlines will be coming in 2018.” That could be pretty interesting, we’ll have to wait to hear more details.

Signup Bonus

The card has the following signup bonus:

- Get $100 back after spending $500 within the first 90 days

Your 10,000 bonus points will be awarded at the close of the first billing statement after you spend $500 in purchases on your Uber Visa Card.

You’ll apply for the card in the Uber app or online, and the card will be available for you to use immediately upon approval with a virtual instantly-issued card (a few card issuers do this).

Points Currency

The card earns ‘points’ which can be redeemed for cash back, Uber credit, or gift cards at a rate of 1¢ per point. In other words: it’s a cash back card. Cash back can be received as a statement credit or a transfer to your bank.

- Reward redemptions start at a $5 when redeemed for Uber credit and $25 when redeemed for cash back or gift cards

- No limit to how many points you can earn

- Points don’t expire

Barclaycard has stated they would like to airline transfer partners in 2018 as well.

Fees

- No annual fee

- No foreign transaction fee

- APR: 15.99%, 21.74% or 24.74% depending on credit worthiness

Card Benefits

- Up to $600 in mobile phone insurance for theft or damage if you pay your complete monthly phone bill with the Uber card. There is a $25 deductible. Coverage for stolen and damaged cell phones as well as involuntary and accidental parting of your cell phone is provided. Contact the Benefits Administrator at 866-894-8569 or visit CardBenefitServices.com for additional details. Once all other available insurance has been utilized, Cellular Telephone Protection will provide coverage up to six hundred ($600) dollars per claim after the twenty-five ($25.00) dollar deductible, with a maximum of two (2) claims and twelve-hundred ($1,200.00) dollars per twelve month period. More details here.

- $50 subscription credit after you spend $5,000 on your card per year. Eligible subscription services are: Apple Music, Pandora, Spotify, Amazon Music, Google Music, Audible, Sirius XM, Netflix, Hulu, HBO NOW, DirecTV NOW, the membership fee for Amazon Prime, and Shoprunner. (This credit only begins in year #2 if you spent $5,000 in year #1.)

- No foreign transaction fees

- Exclusive access to events and offers in select U.S. cities

- Complimentary FICO score (like all Barclay cards)

Final Thoughts

I’ve always thought that the various tiered cashback cards are worthless since most purchases fall into the lowest 1% category. This is the first tiered cashback card I’m impressed by:

- The 4% eateries category is awesome for someone who eats out a lot. Sure, a lot of travelers would prefer 3x CSR points on dining since those points can be worth more than 4%, but for a cashback person this is excellent. The dining highest cash back card that comes to mind is 3.5% on Bank of America Premium Rewards, and that’s only for people who have $100k in BofA accounts. [Related: Best Credit Cards For Restaurant Spend]

- The 4/3/2 categories actually cover many/most purchases for a lot of people. Even your typical consumer who will just use one credit card for everything could potentially do well with this card, depending on their spending patterns.

This is the first 1%-base card that I’d actually consider recommending someone who wants a single card, though in practice I may defer to the Double Cash or the Alliant 2.5% card for simplicity (depending on the consumers spending patterns).

In any case, for credit card enthusiasts, it’s not a question of one card or another: someone who finds the card useful can certainly add it to their collection. Maybe it’ll even be available for product change from another Barclay card.

There are a few reasons people might find the card interesting:

- Get 4% cash back on dining, including international dining

- Get 3% cash back on travel

- $600 mobile phone coverage is excellent for a no-fee card; we compared the various credit cards who offer this benefit here

- $50 streaming credit; we don’t usually see perks like that on no-fee cards

- It’s a no-fee card that can be used internationally (there are more-and-more cards coming out with this feature)

The biggest surprise to me is that they created a cashback card, not an Uber rewards system. They did not even offer 4% on Uber rides. In other words, the card doesn’t have much to do with Uber. That’s not a bad thing about the card, just an observation.

Uber mentioned specifically that they are focusing on long-term users who will keep this card as their main credit. For that reason they kept the signup bonus small; they don’t want gamers who will signup and leave. That’s also why they nudge you to put your monthly cellular bill ($600 protection) and monthly subscription services ($50 credit) on the card to keep it as your ongoing-use card.

F.A.Q

Can I product change to this card?

Currently this is not possible. Customer service representatives are stating that it’s not currently possible so it might be possible in the future.