Update: Sign up bonus is now 50,000 points.

The Chase Sapphire Reserve is likely to be one of, if not the most popular premium travel credit card. In this in depth review we will be looking at all of the card benefits (from lounge access to the annual travel credit) as well as information about applying for the card itself (e.g average approved credit score, common reasons for denial etc).

Unlike other websites, we do not receive a commission if you sign up for this card from our site. This means we are able to give you unbiased advice.

Before we get started, it’s important to keep in mind that this card comes with an annual fee of $450. The sign up bonus and benefits easily make up for this high annual fee in the first year, but keeping the card in the long term may not make sense for you so keep that in mind and remember when you sign up for the card so you can cancel before having to pay the annual fee a second time if that’s your plan. There is also an annual fee of $75 for each authorized user you have on your account.

Contents

- 1 Application Information

- 2 Card Benefits

- 2.1 $300 Annual Travel Credit

- 2.2 Complimentary Airport Lounge Access

- 2.3 Points Are Worth 50% More In Travel Rewards

- 2.4 Global Entry or TSA Pre✔ Fee Credit

- 2.5 1:1 Point Transfer To Travel Partners

- 2.6 Variety Of Insurance Products

- 2.7 Roadside Assistance

- 2.8 Emergency Medical & Dental Benefit

- 2.9 Access To The Luxury Hotel & Resort Collection

- 2.10 Car Rental Privileges

- 2.11 Elite Hotel Benefits At Relais & Châteaux

- 2.12 Exclusive Events & Experiences

- 2.13 No Foreign Transaction Fees

- 3 Rewards Program

- 4 Our Verdict

- 5 F.A.Q’s & Tips

Application Information

As this is a brand new card, the information in this section is likely to be sparse. We will add to it over time.

Does The Chase 5/24 Rule Apply To This Card?

If you are unfamiliar with this rule, I’d strongly recommend reading this post. Unfortunately this rule does apply.

What Credit Score Is Required

We do not have this information currently.

Common Reasons For Denial:

- Too many cards in the past 30 days (this is common between all Chase cards, you’re limited to 2/3 per 30 month)

- Too much credit currently extended to them (you’re able to bypass this by calling Chase reconsideration and offering to reallocate your credit limits from existing cards)

Sometimes calling reconsideration can help you turn your denial into an approval. Read our tips for calling reconsideration.

What Credit Bureau Does Chase Pull For The Chase Sapphire Reserve?

This depends on the state that you live in, for more information please read this post.

What Credit Limit Will I Receive?

This is based on 69 data points.

| Minimum Credit Limit | Highest Reported Credit Limit | Average Credit Limit |

|---|---|---|

| $5,000 (only one DP, everybody else has $10,000 minimum) | $34,000.00 | $11,769.00 |

Card Benefits

Being a premium travel credit card, this card comes with a lot of different benefits. Some of these benefits are quite substantial and detailed and because of this we’ve given a round down on those in more detail on separate pages. We will provide an overview of all the benefits, as well as links to any additional relevant information.

$300 Annual Travel Credit

Every year (based on calendar year statement cycles) you will automatically receive up to $300 in statement credits as reimbursements for travel-related purchases. What they consider travel is quite broad, we’ve written more on this benefit here. Beginning in May 2017, the statement credit goes based on the cardmember year, not calendar year.

Complimentary Airport Lounge Access

You and your authorized users get a free Priority Pass Select membership. This gives you free access to 900+ lounges in the priority pass network. It’s unclear if you’re allowed to bring in any guests or not. We will have more about this benefit shortly.

Points Are Worth 50% More In Travel Rewards

It’s possible to redeem your points for 1¢ each towards statement credit. With this card points are worth an additional 50% (1.5¢ per point) when you redeem them for travel (airfare, hotels, car rentals or cruises) through Chase Ultimate Rewards.

Global Entry or TSA Pre✔ Fee Credit

You can receive a statement credit of up to $100 when you use your card for the application fee on Global Entry or TSA PreCheck. You’re able to receive this statement credit once every 4 years.

1:1 Point Transfer To Travel Partners

This card lets you transfer all your Chase Ultimate rewards points to their travel partners (including points earned on cards that don’t have this functionality). Chase’s travel partners are as follows:

| Chase Travel Partners (All Transfer 1:1) | ||

|---|---|---|

| Airlines | ||

| British Airways Executive Club | Singapore Airlines KrisFlyer | Virgin Atlantic Flying Club |

| Flying Blue AIR FRANCE KLM | Southwest Airlines Rapid Rewards | Aer Lingus |

| United MileagePlus | Iberia Plus | Emirates |

| Air Canada Aeroplan | ||

| Hotels | ||

| Hyatt Gold Passport | Marriott Rewards | |

| IHG Rewards Club |

Variety Of Insurance Products

This card comes with the following insurance products, when you use your card to book:

- Auto Rental Collision Damage Waiver/Primary Rental Insurance (coverage up to $75,000 when you decline the rental company’s collision insurance and charge the entire rental to your card). Unlike the Chase Sapphire Preferred, there is no restriction on exotic cards. But this card does come with a $75,000 limit.

- Trip Cancellation/Trip Interruption Insurance (reimbursement of up to $10,000 per trip when it’s cancelled or cut short by sickness, severe weather and other situations)

- Baggage Delay Insurance (reimbursement for essential purchases when your baggage is delayed for more than 6 hours, up to $100 per day for 5 days).

- Travel Accident Insurance (coverage up to $1,000,000)

- Trip Delay Reimbursement (if your common carrier is delayed more than 6 hours or requires an overnight stay then you and your family are covered for unreimbursed expenses up to $500 per ticket) CSP requires it to be delayed for more than 12 hours.

- Emergency Evacuation & Transportation (if you or a member of your immediate family are injured or become sick during a trip far from your home and it results in an emergency evacuation then you’re covered for medical services and transportation up to $100,00)

- Travel and Emergency Assistance (can call the benefit administrator for legal and medical referrals, you are still responsible for any costs)

Roadside Assistance

You’re allowed to call for a tow, jumpstart, tire change, locksmith or gas up to 4 times per calendar year and you’ll receive a reimbursement up to $50 per incident

Emergency Medical & Dental Benefit

If you’re 100 miles or more from home on a trip, you can be reimbursed up to $2,500 for medical expenses if you or your immediate family member become sick or injured

Access To The Luxury Hotel & Resort Collection

This gives you the following benefits at some hotels:

- Best available rate guarantee

- Automatic room upgrade upon arrival, when available

- Complimentary in-room Wi-Fi, when available

- Complimentary continental breakfast

- $25 USD food or beverage credit

- VIP Guest status

- 3PM check-out upon request, when available

This benefit is actually provided by Visa. You can find full details about this benefit be found here (we hope to do a detailed post on this in the future).

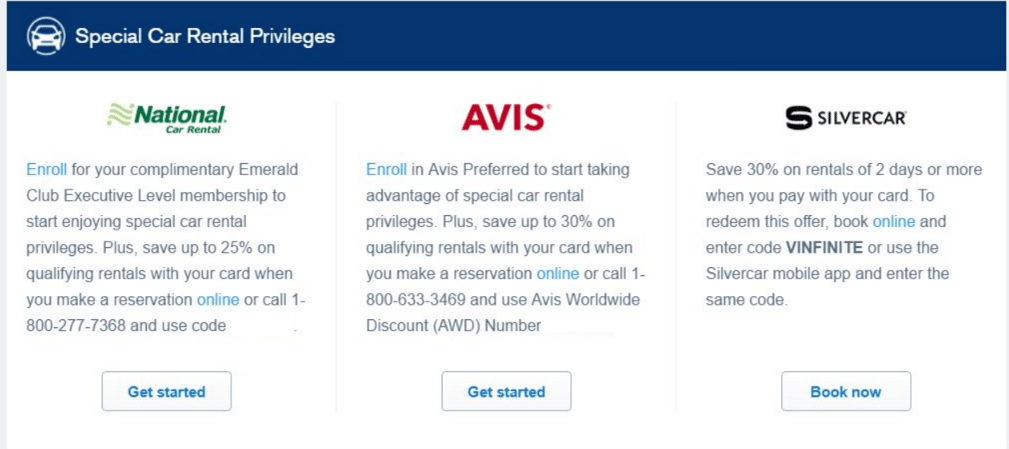

Car Rental Privileges

You can receive enhanced benefits from the following car rental agencies, when you book using your card:

- National Car Rental

- Emerald Club Executive Level membership

- Save up to 25%

- Avis

- Save up to 30%

- Silvercar

- Save 30% on rentals of 2 days or more

Image via @VM4827

Elite Hotel Benefits At Relais & Châteaux

If you book through the Visa Infite concierge and stay two nights at qualifying Relais & Châteaux properties you’ll receive Club 5C status. Normally you need to stay an average of 18 nights annually to receive this status. It gives you the following benefits:

- Access to a special reservations line

- Welcome gifts & amenities

- Unique experiences/extras (e.g picnic lunch served by Little Nell at the top of Colorado’s Aspen Mountain)

An example of what you receive can be found on the website for the Wedgewood Hotel.

Exclusive Events & Experiences

Chase hasn’t provided information on this, we will add to this post when they do. It’s entirely possible this benefit is talking about stuff like access to the Chase lounge at the U.S. open that is open to all Chase cardholders.

No Foreign Transaction Fees

This card doesn’t charge you any fees if you make a purchase in a foreign transaction. You’ll receive the rate that Visa uses, you can read more about how this rate is determined by going here.

Rewards Program

This card earns Chase Ultimate Rewards points. These are the same points that are earned on the following cards: Chase Freedom, Chase Freedom Unlimited, Chase Sapphire, Chase Sapphire Preferred, Chase Ink Cash & Chase Ink Plus.

Earning Rewards

Standard Earning

This card earns at the following rates per $1 spent:

- 3x points on travel & restaurants

- 1x points on all other purchases

Chase provides their definition for travel & dining on this page. It should include most of the things you should expect.

Sign Up Bonus

Current Sign Up Bonus

- 100,000 points after $4,000 in spend within the first three months

Sign Up Bonus History

- This card has always offered the same sign up bonus

Redeeming Your Rewards

Chase has a very flexible point program. At minimum you can redeem your points for 1¢ in statement credit, this card also lets you redeem them for 1.5¢ towards travel using the Chase Ultimate Rewards portal. You can also transfer your points to points in any of the following travel loyalty programs (1:1):

| Chase Travel Partners (All Transfer 1:1) | ||

|---|---|---|

| Airlines | ||

| British Airways Executive Club | Singapore Airlines KrisFlyer | Virgin Atlantic Flying Club |

| Flying Blue AIR FRANCE KLM | Southwest Airlines Rapid Rewards | Aer Lingus |

| United MileagePlus | Iberia Plus | Emirates |

| Air Canada Aeroplan | ||

| Hotels | ||

| Hyatt Gold Passport | Marriott Rewards | |

| IHG Rewards Club |

Our Verdict

This card is pretty amazing in the first year. At minimum you should get the following value out of this card:

- $600 in travel credit (remember this is on a calendar year, so you could get $300 in credit in October and then again in January)

- 100,000 points (worth anywhere from $1,000-$1,500+)

- Lounge access (not the best, but something for people without any lounge access currently)

There is the annual fee of $450, but that is easily outweighed by the above. The question becomes more difficult to answer after your first year, personally I don’t think it’s worth keeping. In your second year you’re basically paying $450 and getting the $300 travel credit once (and you’re actually getting this in your third calendar year of holding the card), 3x on travel & dining (only 1x more than the Chase Sapphire Preferred with a $95 annual fee) and some middling to poor lounge access plus a bunch of other fringe benefits.

Personally I don’t see great value there, but I can see why people would want to keep it year two onwards as well. If you do apply for this card, remember that Chase combines multiple inquiries into a single hard pull – so it might make sense to apply for another card.

We Recommend This Card For:

- People that want a high sign up bonus

- People that can make use of the annual travel credit of $300

- People with a lot of spend in the travel & dining categories

We Don’t Recommend This Card For:

- People that are unable to meet the minimum spend requirement

F.A.Q’s & Tips

Feel free to ask questions in the comments and we will add to this section over time.