Update 3/27/26: Card now has a $200 signup bonus after spending $1,000. (Previously there was no signup bonus.) Hat tip to reader Dan

Update: Changes to card:

- 5% cash back on gas & base purchase are no longer combined together as one category. Now Gas has it’s own $3K cap, & military base purchases has a $5K cap, per cal. yr.

- 2% cash back on groceries is now 3%, per cal. yr, keeping the same $3K cap.

- Foreign transaction fees now 0%

- Rewards paid monthly rather than yearly

Original post 12/17/14: This guest post was submitted by Toby Cobb who is a frugal traveler that used to be in the USMC. He tries to use points and miles to spend less money and more time with family. If you’d like to submit a guest post then please read our guidelines first, if your post is accepted then you’ll receive $50 as our way of saying thanks.

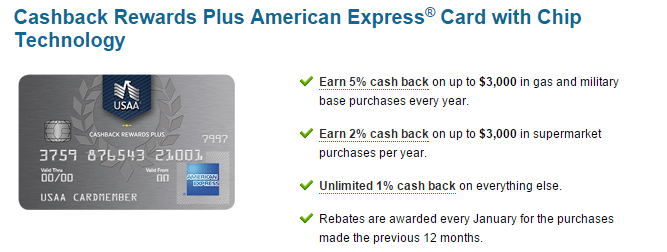

USAA has recently launched a new range of credit cards, the most interesting is the Cashback Rewards Plus American Express. The biggest selling point of this card is 5% cash back on gas and military base purchases and the lack of an annual fee. Note, however, that applications are limited to USAA members.

Contents

Pros & Cons

Card Positives:

- 5% cash back on gas and military commissaries, exchanges and shoppettes¹ up to $3,000 on gas purchases annually

- 2% cash back on groceries up to $3,000 on grocery purchases annually

- 1% cash back on other purchases with no limit

- No annual fee

- 0% introductory APR on balance transfers for 18 months

- EMV chip

- Cash Advance fees are waived when transferring funds electronically into a USAA deposit account.

- No penalty APR

Card Negatives:

- 5% limited to $3,000 in purchases each year.

- 3% balance transfer fee (up to $200)

- 1% Foreign Transaction Fee

Other points of interest:

Whenever we talk about USAA, I have to mention their incredible customer service. They’ve always been great for me, regardless of the product.

Additionally, there are special SCRA (Servicemembers Civil Relief Act) benefits, but they’re actually pretty crummy. A 4% APR when you’re deployed may sound good but Barclay and Amex completely waive all fees and give you a 0% APR the entire time you’re on Active Duty.

[Read: Credit Card Annual Fee Waivers & Other Benefits For Those On Active Duty]

USAA Membership:

You’re eligible if you fit in these categories.

- Active, retired and honorably separated officers and enlisted personnel of the U.S. military.

- Officer candidates in commissioning programs (Academy, ROTC, OCS/OTS).

- Adult children whose eligible parents have or had a USAA auto or property insurance product.

- Widows and widowers of USAA members who have or had a USAA auto or property insurance policy.

You can find more information here.

Recommendation:

I would recommend this card to someone that spends $3,000 each year at military exchanges. Military exchanges are unbonused spend for other credit cards, so the most you’d reliably be able to is 2.2% with the Arrival Plus card or maybe 3% with the JCB Muraki .

[Read: Best credit cards for unbonused spend]

I would not recommend this card to those that can get much higher value out of credit card signups and don’t shop on military bases. The 5% cash back on gas is easily beaten by the Fort Knox Credit Union 5% gas card, as it has no limit. Or check our best gas card page for other options.

My Verdict

USAA sent me a pre-selected email offer a few weeks back and I tried to product change my old USAA Platinum Mastercard to the Cashback Rewards Plus. I was unsuccessful. I could get more value out of the 5% gas rewards, but you can’t switch Mastercard to Amex. And since USAA won’t let you get around the hard pull even for a credit line increase, it looks like my oldest card will almost be the one with the lowest credit limit.

USAA also launched the Preferred Cash Rewards World MasterCard® with Chip Technology which offers 1.5% cash back on all purchases. Given that there are multiple cards that earn 2% or more, this isn’t a particularly interesting offering.

Thanks again to Toby for this guest post. If you have any military related credit questions then please feel free to ask him in the comments. If you’re interested in submitting a guest post then I’d recommend reading through this first.