Contents

Big Issuers

American Express

Doesn’t do a hard pull for credit limit increases, in fact it’s quite easy to get large credit limit increases from American Express. Read our in depth guide by clicking here.

Barclays:

Barclays seems to do a hard pull for customer initiated credit limit increases but they also seem to be pretty good at doing automatic increases at the six or twelve month mark.

- Barclays Arrival: Does a hard pull for a credit limit increase: 1, 2, 3

Bank of America:

As of May 2018 Bank of America no longer does a hard pull for credit limit increases.

According to BofA they are required to do a hard pull by federal law for all credit limit increases. Some people have reported that they have received an automatic credit limit increase without a hard pull being performed. For credit limit increases they’ll usually do a hard pull from TransUnion, whereas for new applications it’s usually from Experian.

Recently, they seem to be doing just a soft pull for reallocations when you call in. YMMV. You can also check for deals/offers and they will sometimes offer a credit limit increase with no hard pull.

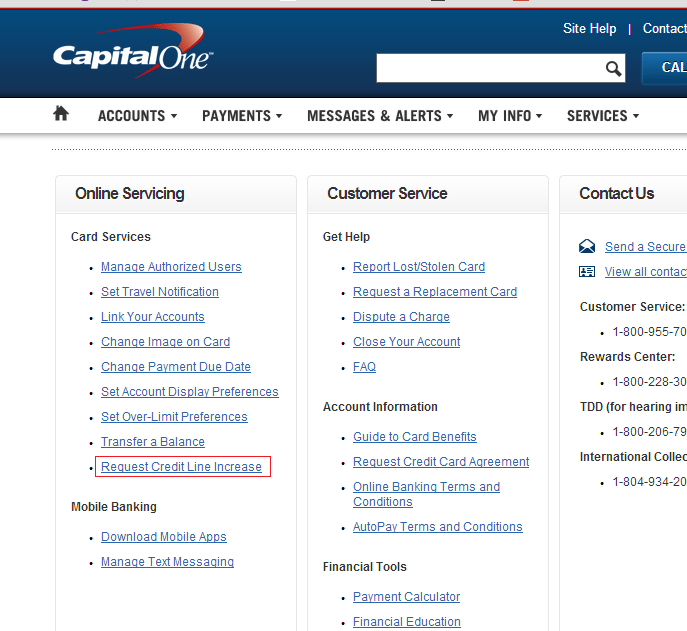

Capital One:

You can request a CLI increase online once every six months with your Capital One card, this results in a soft pull. To request:

- Log into your account

- Click “Request Credit Line Increase” which is found under “Card Services”

Image courtesy of reddit user nmac_mpls

A lot of people will find that they struggle to receive an increase from clicking this button. One person reported that making a complaint with the BBB resulted in them receiving an increase from $500 to $2,000 and had their annual fee removed – but this is an ethical grey area.

Others reported that the only way to get an increase from Capital One is to contact somebody in the executive office of Capital One asking for one. If you do this, we suggest getting in touch with the Capital One CEO Richard Fairbank ([email protected]). You should include why you think you deserve a CLI and what you plan to do if you don’t receive one (e.g cancel your current cards).

Chase:

You can now do a credit limit increase via the app and it’ll be a soft pull if you are pre-approved, more details here. Otherwise if you the card holder initiate a credit limit increase, it will always result in a hard pull with Chase.

If you do multiple credit limit increases in the same day it will be combined into a single inquiry.

Citi

Update: You can also request an increase via their app and you’ll also be told if it’s a hard or soft pull.

Update: Citi will now tell you if it’s going to be a hard or soft pull online. To find out how to tell, read this post.

Citi seems to do both soft and hard pulls, usually if they come back with an instant decision a soft pull has been performed whereas if they require more time a hard pull will be performed. If you call and ask the customer service representative should be able to tell you if it will be a soft or hard pull if you proceed, but this really depends on how knowledgeable the phone representative is and you should always be expecting a hard pull and be happy if a soft pull occurs.

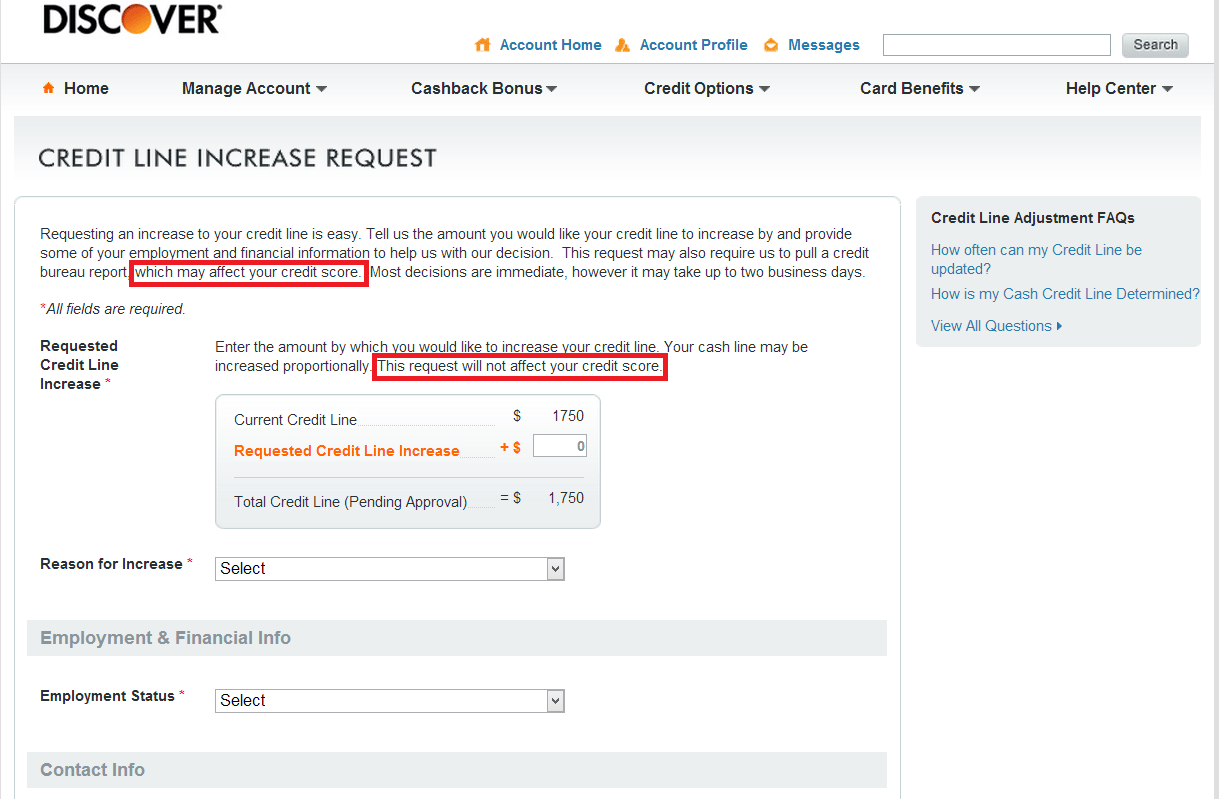

Discover:

Even the Discover site itself reports two different things, at the start of their credit line increase application form it says “…which may affect your credit score”, then further down it says “…this request will not affect your credit score”

Photo courtesy of gx240 from the myFICO forums

In reality it depends on how large of a credit limit increase you want. Small increases can be done without a hard pull, large increases require a hard pull. This is how the process works:

- Enter in the credit limit increase you want and all other relevant information

- Discover will either give you the increase (in which case only a soft pull is done) or they will counter with another offer.

- If you reject their offer it’ll give you the option to request further review, if you click this button a hard pull will be performed.

A similar course should be followed if you call up, but this is not always the case which is why it’s best to use the online form.

JCB

You can request a CLI from JCB by calling them. They’ll often ask you for employment and address verification in addition to the hard pull that they do.

- Hard pull: 1

USAA

You can request a credit limit increase online, this will result in a hard pull on Equifax.

- Hard pull: 1

U.S Bank

Update 2: They changed the wording on the online request form or by calling. They will usually do a soft pull when using that, but not always.

Update: U.S. Bank now does a soft pull for credit limit increases if you use their online request form or if you call them on 1-866-659-6801. The fact they do a soft pull is also clearly stated on the online page.

You can request a CLI from U.S Bank by clicking here. Your account needs to be open for a minimum of six months before they will consider increasing your credit limit. It seems that requests for a credit limit increase of anything lower than $1,499 results in a soft pull and requests above $1,500 will result in a hard pull – but there have been exceptions to this.

Wells Fargo

Wells Fargo seems to be mostly soft pulls, with a few reports of hard pulls. Again, you’re best off calling their customer service department and asking if it’ll be a soft or hard pull, some representatives will be able to tell you – but be willing to cop a hard pull at the end of the day as they might give you incorrect information.

Smaller Issuers

Alliant

Update: According to our contact at Alliant, all credit limit increases are now soft pulls. Update: This is only for those who are part of their credit limit increase campaigns. If you call in then it will be a hard pull.

Comenity

Comenity is in charge of a lot of store issued credit cards that usually come with low limits. It seems they regularly do automatic credit limit increases if you are putting spend on their cards, this typically happens 6-9 months after the card has been opened.

It’s also possible to ask for a credit limit increase, although there doesn’t seem to be much success unless you wait until you’ve had the card for at least 9 months. When you request this they will ask for your income and some other information as well. They now give you the option to select a check box saying you agree to a credit pull, you can still get increases without checking this box. More information here.

- Soft pull: 1, 2

- Hard pull (if you call in), 2 (online)

DSNB (Macy’s, Bloomingdale’s)

Department Stores National Bank (DSNB) is the private label arm of Citi Bank, they have a confusing policy when it comes to CLI’s. It seems if you are eligible under their criteria (not sure what they consider under this) a soft pull will be performed, otherwise a hard pull will be performed. It’s best to just assume a hard pull will be done and then be pleasantly surprised if a soft pull happens. You can only request a CLI once every six months.

Some people have reported that if you call they can see if your are eligible based on their criteria, if not you can ask them to stop and no pull will be done. This is obviously a your milage may vary situation though.

Fifth Third

Can only request an increase via phone. Maximum increase is $3,000.

- Hard pull: 1

FNBO:

Normally smaller increases will result in a soft pull with larger increases resulting in a hard pull.

GEMB (Walmart, Chevron, JC Pennys)

GEMB issued cards will usually be a soft pull, there are a couple of examples of them being hard pulls but this is few and far between. They also do automatic credit limit increases, this usually happens after your third statement cuts if you’ve been paying on time.

HSBC

Requires a hard pull to do a credit limit increase: 1,

They usually do a soft pull for requests that are less than $25,000 (total) and hard inquiries for credit limits that exceed $25,000. But we suggest reading our full guide here for more information.

SDFCU

- Hard pull: 1,

Synchrony

Update: Newer datapoint says it’s a soft pull unless the account has been opened for less than 60 days.

It can either be a soft or hard pull and there is no way of knowing ahead of time. From one of their representatives:

It is impossible for us to determine if the request for a credit limit increase will result in a hard or soft inquiry as it is completely decided by the system. However, to be on the safe side we assume that it will be a hard check

TD Bank

According to this they do a hard pull.

USAA:

You are only eligible for a credit limit once every six months with USAA, it will always result in a hard pull.

Big thanks to the myFICO forums for providing almost all of the data points for this post.