Update: The application link for this card went down, when it came back the language was removed.

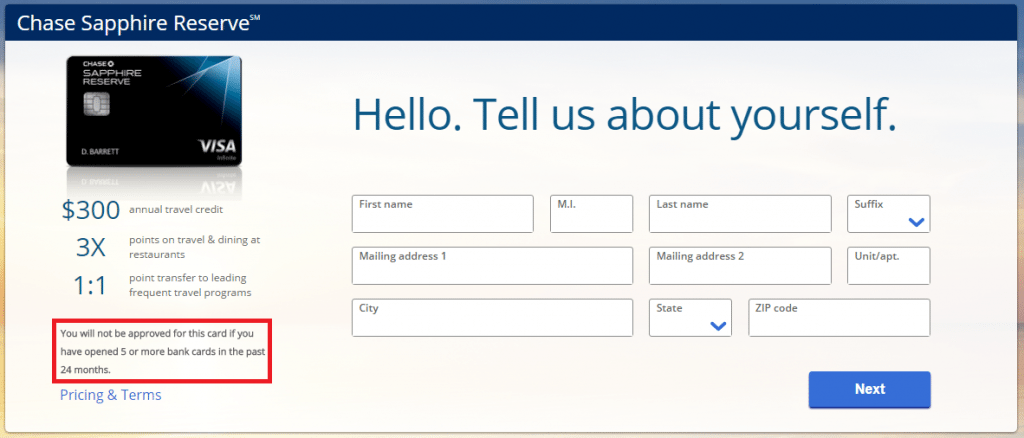

We’ve known about the Chase 5/24 rule for awhile now, but it seems that Chase are now including it in the fine print of at least the Chase Sapphire Reserve card. It states:

You will not be approved for this card if you have opened 5 or more bank cards in the past 24 months.

I’m not currently seeing this on any other cards issued by Chase, but as we know this isn’t the only card affected by this rule and not all cards issued by Chase are affected either. Also keep in mind it is possible to bypass this rule, the most common way is through an in branch pre-approval (I’d strongly recommend reading our F.A.Q about this here).

Interestingly the official rule states that if you have opened 5 or more bank cards in the past 24 months, you’re disqualified. I assume this means that store cards and other loans on your credit report will not be counted (what we previously expected). I’m honestly a bit surprised Chase didn’t have this language on the application pages sooner as it was misleading not having this criteria publicly available.

Hat tip to reader Peter C