Offer at a glance

- Maximum bonus amount: $100

- Availability: Nationwide

- Deposit Required: $15,000

- Deposit Length: 3 statement cycles

- APY: 1.35%

- Hard/soft pull: Soft

- ChexSystems: Unknown

- Credit card funding: None

- Monthly fees: None

- Early account termination fee: None

- Expiration date: September 8, 2017

The Offer

- Open a High Yield Savings Account with CIT Bank using the direct link above to get $100 bonus and a

1.3%1.35% APY rate. - Must enter promo code: PREMIER at the time of account opening.

- Must deposit $15,000 and maintain that balance for 3 months.

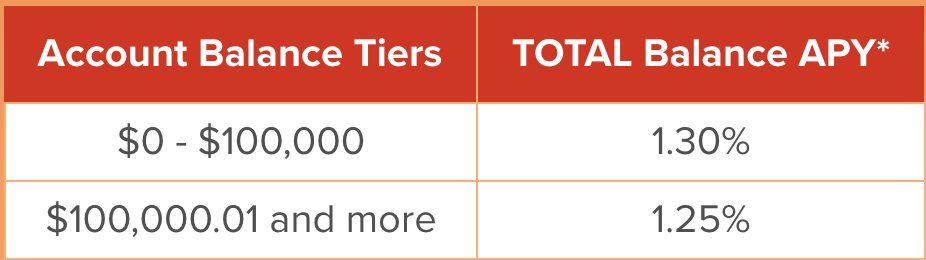

One thing to be aware of is that the 1.35% APY rate is only on balances up to $100k. Balances over $100k will earn 1.3% APY on the entire balance. The $100 signup bonus applies, regardless, to any amount of $15k+.

The Fine Print

- Account must be opened and funded by September 8, 2017.

- Customers who received a CIT Bank bonus payment or enrolled in another CIT Bank bonus offer between January 1, 2017 and July 14, 2017 (regardless of whether the bonus has yet been paid) are not eligible for this Premier High Yield Savings account bonus offer.

- Minimum opening deposit is $100.

- Interest rates for the Premier High Yield Savings account are variable and may change at any time without prior notice.

- One bonus per customer. If multiple accounts are opened by a customer, only one account will be eligible for the bonus.

- Funding must be done with new funds. Funds on deposit with CIT Bank, N.A. or its OneWest Bank division at any time during the 90 days preceding account opening, are ineligible.

- The account must be funded within 30 calendar days from the account opening date.

- An average monthly balance of at least $15,000 is maintained for the first three full statement cycles. A full statement cycle is defined as beginning the first day of a month and ending the last day of that same month, e.g., 5/1/17 to 5/31/17.

- A $100 bonus will be deposited to the Premier High Yield Savings account of the qualified customer within 45 days of the end of the third full statement cycle following account opening. For example, a customer who qualified for the bonus on a Premier High Yield Savings account opened on July 10, 2017, would receive a statement credit of $100 no later than December 15, 2017.

- Bonus payments are reported as interest earned on IRS form 1099-INT for the calendar year in which it was paid. Recipient is responsible for any applicable taxes.

Avoiding Fees

There are no monthly fees and no early account termination fee.

Our Verdict

It’s uncommon to have an account which offers a solid rate (nearly the best available) and comes with $100 signup bonus to boot. Might not be worth the hassle just for the bonus, but if you’re looking for a high-interest account it’s a great option.

Sample scenario for opening this account would look like this:

- Open account on July 15, 2017

- Have account fully set up and funded witht $15k before end of July

- Wait 3 months until end of October to fulfill 3 month requirement

- Wait 45 days until December 15, 2017 for bonus to post (during this time, you are no longer required to maintain the $15k balance)

Two things to keep in mind before jumping on this offer:

- CIT holds you at the lower rate as rates go up. Interest rates have been on the rise lately, and readers tell us that the rates on CIT accounts remain at what you signed up for. (In other words, they don’t have a single uniform APY rate on their savings accounts; they keep various signups at various rates.) A lot of people might be considering this account as a long-term solution (instead of Ally or Discover or whatnot), and it’s not necessarily going to be the best rate forever. If you’re willing to move your money around in another year or two, it’ll probably still be competitive for that amount of time. If you want to find a single high-yield option and park funds there for the next 5+ years, it might be smarter to use something like Ally which will move up the rates as rates go up.

- There’s currently another CIT offer expiring soon. Until July 14, there’s a different CIT bonus available which offers a bonus of up to $425 and a lower 1.15% APY rate.If you put around $15k (the minimum for the bonus), you might do better with the $125 bonus and lower interest rate. It’ll depend how long you’re planning on leaving the money in the bank. Run the numbers and decide.If you’re depositing $100k+, you might do better with the $250 bonus, and if you’re depositing $300k+ you might do better with the $425 bonus. It’ll depend on how long you’re planning on leaving the money there. Again, run the numbers to see which option is better. Remember, $100k+ accounts only earn 1.25%, not 1.3%.

We’ve added this rate to our list of Best Savings Account Rates.

Hat tip to readers Mike and A.

Useful posts regarding bank bonuses:

- A Beginners Guide To Bank Account Bonuses

- PSA: Don’t Call The Bank

- Introduction To ChexSystems

- Banks & Credit Unions That Are ChexSystems Inquiry Sensitive

- What Banks & Credit Unions Do/Don’t Pull ChexSystems?

- How To Use Our Direct Deposit Page For Bank Bonuses Page

- Common Bank Bonus Misconceptions + Why You Should Give Them A Go

- How Many Bank Accounts Can I Safely Open Within A Year For Bank Bonus Purposes?

- Affiliate Links & Bank Bonuses – We Won’t Be Using Them

- Complete List Of Ways To Close Bank Accounts At Each Bank