[Originally posted in February 2017. Reposting in May 2017 since the bonus increased a bit. Reposting 7/9/17 due to new offer with 1.3% APY.]

Offer at a glance

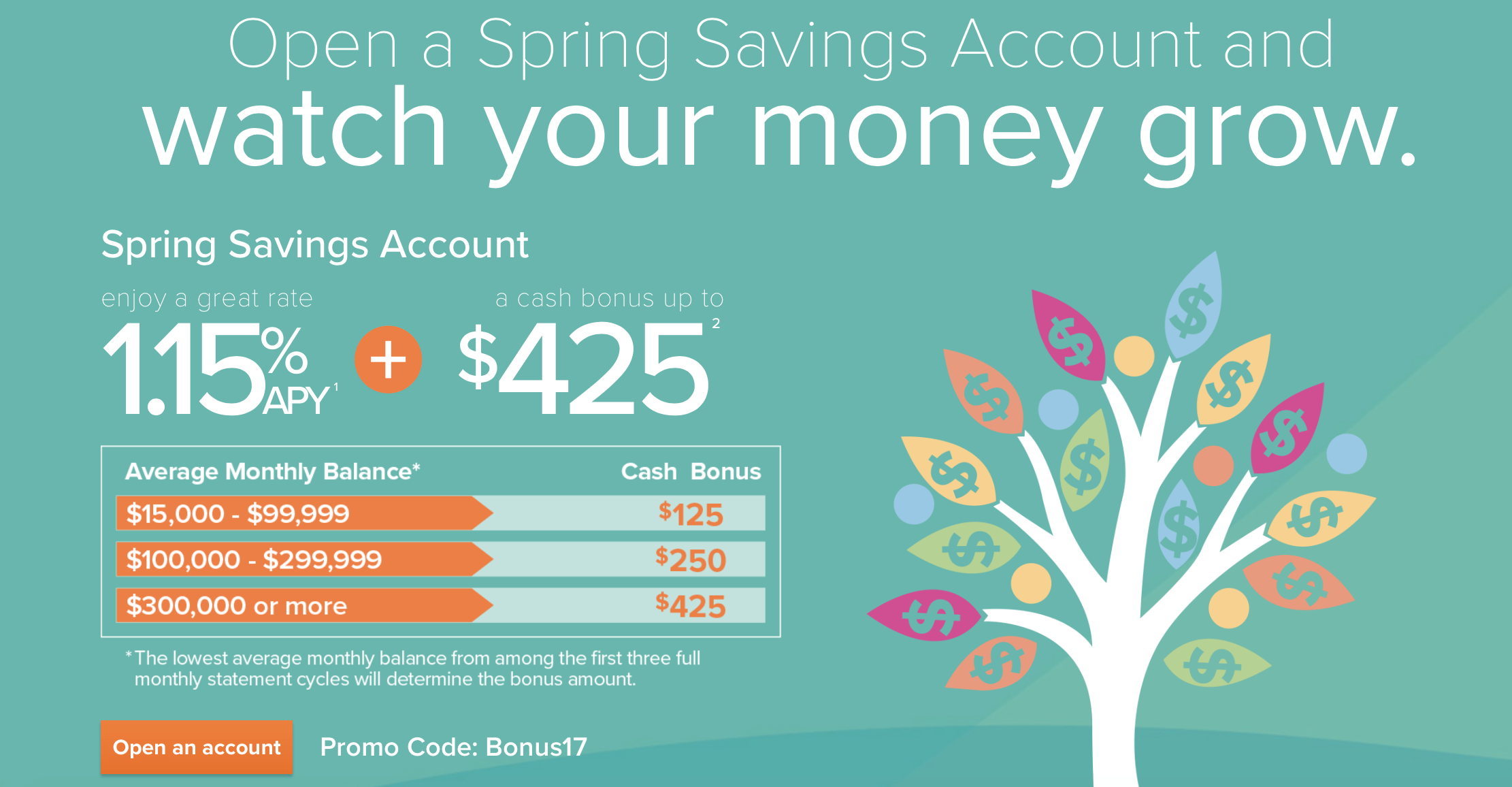

- Maximum bonus amount: $425

- Availability: Nationwide

- Deposit Required: See below

- Deposit Length: 3 statement cycles

- APY: 1.15%

- Hard/soft pull: Soft

- ChexSystems: Unknown

- Credit card funding: None

- Monthly fees: None

- Early account termination fee: None

- Expiration date:

April 28, 2017 June 30th, 2017July 14, 2017

The Offer

CIT two different signup offers

Direct link to offer (other link without promo code for comparison)

- Open a High Yield Savings Account with CIT Bank (1.15% APY) and receive a bonus of up to $425 with promo code: BONUS17

The bonus you receive depends on how much you deposit. You’re required to keep that average minimum daily balance for the first three full statement cycles. The tiers are as follows:

- $15,000-$99,999: $125 bonus

- $100,000-$299,999: $250 bonus

- $300,000 and up: $425 bonus

The Fine Print

- Account must be opened and funded by July 17, 2017.

- One bonus per customer.

- Daily ACH withdrawal limit of $25,000

- If multiple accounts are opened by a customer, only one account will be eligible for the bonus.

-

Offer valid on High Yield Savings accounts opened between March 31, 2017-June 30, 2017, provided that the following requirements are met:

- The account is opened with a minimum deposit of $100. All funds used to qualify for bonus eligibility must be new funds. Funds on deposit with CIT Bank, N.A. or its OneWest Bank division at any time during the 90 days preceding account opening, are ineligible.

- The account is funded within 30 calendar days from the account opening date.

- An average monthly balance of at least $15,000 is maintained for the first three full statement cycles. A full statement cycle is defined as beginning the first day of a month and ending the last day of that same month, e.g., 5/1/17 to 5/31/17. The average monthly balance for each full statement cycle is calculated as follows: at the end of each day, the High Yield Savings Account balance is recorded. When the statement cycle ends, these end-of-day balances are added together and then divided by the number of days in the statement cycle to determine the average monthly balance.

-

The account will be deemed ineligible for a bonus payment if the account is not funded within 30 days of the account opening date or is closed prior to the end of the third full statement cycle or if the average monthly balance from any of the first three full statement cycles is less than $15,000.

-

Any bonus for which the customer qualifies will be deposited to the account within 45 days of the end of the third full monthly statement cycle.

-

Bonus payments are reported as interest earned on IRS form 1099-INT for the calendar year in which it was paid. Recipient is responsible for any applicable taxes.

Avoiding Fees

There are no monthly fees and no early account termination fee.

Our Verdict

Bonus is now $25 better with promo code on the $15k threshold and on the $300k threshold than had been the case in the past.

The nice thing about things account is that it offers a 1.15% APY (close to the top available basic savings account rate). If you have lots of cash on hand, it could make sense to use CIT Bank and get the bonus + good interest rate.

Check out our post on Best Savings Accounts and do the math to compare best rates. For example, if you have exactly $100,000 in funds which will be in a savings account for a year, you’ll do better putting those funds in a Memory Bank account and getting 1.5% APY for the first year (that would earn you $1,500 compared to $1,425 with this account and bonus). In many other scenarios, you’ll do better with the CIT Bank rate + bonus.

Assuming you have $15,000 in cash sitting an account earning around the 1.15% interest rate, you’ll net $125 by opening this account and moving your money over. Not bad for a soft pull bonus with no requirements. I imagine many people have $15,000 in cash reserves or emergency funds so this bonus might be interesting for many people. We will be adding this to our best savings bonuses.

Hat tip to reader John

Useful posts regarding bank bonuses:

- A Beginners Guide To Bank Account Bonuses

- PSA: Don’t Call The Bank

- Introduction To ChexSystems

- Banks & Credit Unions That Are ChexSystems Inquiry Sensitive

- What Banks & Credit Unions Do/Don’t Pull ChexSystems?

- How To Use Our Direct Deposit Page For Bank Bonuses Page

- Common Bank Bonus Misconceptions + Why You Should Give Them A Go

- How Many Bank Accounts Can I Safely Open Within A Year For Bank Bonus Purposes?

- Affiliate Links & Bank Bonuses – We Won’t Be Using Them

- Complete List Of Ways To Close Bank Accounts At Each Bank